Key Stats

- Current Price: ~$276

- Q1 2026 Revenue: $11.6B (+29% YoY)

- Q1 2026 Adjusted EPS: $1.86 (+25% YoY)

- Q1 2026 Free Cash Flow: $1.7B (+14% YoY)

- Full-Year Revenue Guidance: Low double-digit growth (trending toward high end)

- Full-Year EPS Guidance: $7.10–$7.40

- Full-Year Operating Profit Guidance: $9.85B–$10.25B

- Full-Year FCF Guidance: $8.0B–$8.4B

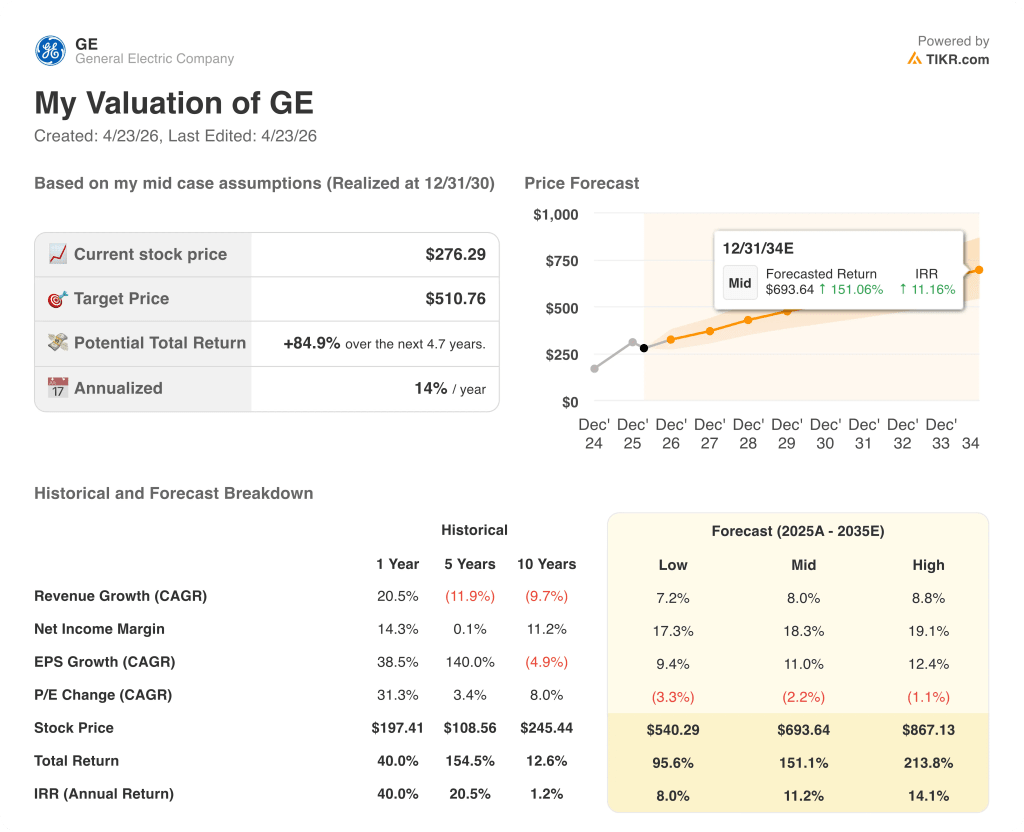

- TIKR Model Price Target: ~$511

- Implied Upside: ~85%

GE Aerospace Q1 2026 Earnings: Revenue Jumps 29%, But the Second Half Is the Real Question

GE Aerospace stock (GE) opened Q1 2026 with revenue of $11.6B, up 29% year-over-year, and adjusted EPS of $1.86, up 25%, as commercial engine deliveries and services demand both accelerated well ahead of plan.

The Commercial Engines and Services segment drove the headline, with revenue up 34% as internal shop visit revenue grew 35% and spare parts sales climbed over 25% from improved material availability.

Commercial services revenue rose 39% overall, with LEAP internal shop visits up over 50%.

Engine deliveries surged 43% company-wide, including LEAP deliveries up 63% and wide-body deliveries up over 25%, led by GEnx.

Defense and Propulsion Technologies contributed 19% revenue growth, with defense and systems units up 14% as F-110 and rotorcraft engine volumes increased, and Propulsion and Additive Technologies grew 29%.

Orders were up 87% in the quarter, with CES orders up 93% and DPT orders up 67%, including record defense orders for the decade and a book-to-bill above 2 for DPT for the second consecutive quarter.

“Had it not been for current events, we’d be talking about an increase in the guide this morning,” said CFO Rahul Ghai on the Q1 2026 earnings call, noting that Q1 came in roughly $300 million above internal expectations.

Despite the quarter’s strength, management held full-year guidance at EPS of $7.10–$7.40 and operating profit of $9.85B–$10.25B, citing Middle East conflict uncertainty and its potential lag effect on commercial services demand in the second half.

Management did signal the company is trending toward the high end of every guided range, with Q2 services growth expected at high teens, supported by 95% of spare parts revenue already secured in backlog and all required shop visits already off wing.

Full-year services revenue growth guidance was raised to approximately $4.0B year-over-year, up from roughly $3.5B expected previously.

GE Aerospace stock also saw commercial services backlog reach over $170B, up nearly $30B since year-end 2024, providing multi-year demand visibility across the installed fleet.

The company announced plans to invest $1B in U.S. manufacturing sites and supply chain for the second consecutive year, with an additional $100M directed to external suppliers for tooling and capacity expansion.

GE Aerospace Stock Financials

The Q1 2026 income statement shows a business generating strong operating leverage on accelerating revenue, with operating income above $2.5B even as margin pressure from installed engine mix continues.

Gross margin came in at 31% in Q1 2026, consistent with the 30% posted in Q4 2025 and reflecting the ongoing mix effect of faster growth in lower-margin installed engine shipments versus services.

Operating income was $2.50B in Q1 2026, up ~15% year-over-year from the $2.18B posted in Q1 2025.

Operating margin was 20.2% in Q1 2026, compared to 22% in Q1 2025, a compression of roughly 180 basis points driven by installed engine growth, GE9X shipments, and continued investment spending.

The margin trajectory over the past several quarters reflects the deliberate trade-off GE Aerospace stock is running: CES operating margin came in at 26.4% in Q1 2026, down 230 basis points year-over-year as LEAP installed engine volume and 9X shipments weigh on near-term profitability while building long-term aftermarket entitlement.

Management guided to roughly flat CES margins for the full year, with LEAP aftermarket margins expected to approach overall CES service margin levels by approximately 2028 as repair capability scales and external shop visit penetration grows.

Is GE Aerospace Stock Worth Buying After Q1 2026?

The TIKR model prices GE Aerospace stock at ~$511, implying roughly 85% upside from the current price of ~$276, based on mid-case assumptions of 8.0% revenue CAGR and an 18.3% net income margin through 2030.

The model’s high-case scenario, assuming 8.8% revenue CAGR and a 19.1% net income margin, puts GE Aerospace stock at ~$867, representing total return potential of over 200%.

Q1’s results reinforce the mid-case assumptions rather than stretching them: services growth is running ahead of plan, but management’s conservatism on the second half reflects genuine uncertainty that the model must accommodate.

The investment case for GE Aerospace stock is incrementally stronger after Q1, not because guidance was raised, but because execution and backlog visibility now make the multi-year earnings ramp look more credible, even with a softer macro backdrop.

GE Aerospace stock delivered one of its strongest quarters in recent history, but management refused to raise full-year guidance, and the question is whether second-half caution is prudent conservatism or a preview of real services deceleration.

What Has to Go Right

- Commercial services backlog exceeds $170B with 95% of Q2 spare parts revenue already secured, providing near-term earnings visibility that de-risks the next two quarters materially

- Spare parts delinquency is up ~70% since year-end 2024, meaning pent-up demand exists that would convert to revenue as supply catches up, regardless of short-term departure softness

- LEAP aftermarket margins are on track to reach overall CES service margin levels by approximately 2028, with the number of repairs developed this year expected to double relative to last year

- Defense book-to-bill held above 2 for the second consecutive quarter, including a $1.4B T408 contract for the CH-53K, diversifying earnings against any commercial air traffic disruption

What Could Still Go Wrong

- Management explicitly referenced a Global Financial Crisis-style lag dynamic, where services revenue typically follows departure declines by several quarters, making second-half 2026 and 2027 more exposed than current backlog visibility suggests

- Spare parts delinquency increasing ~70% since year-end 2024 signals supply chain constraints that could prevent the company from fully capturing services demand even if demand holds

- GE9X losses are not expected to peak until 2028, and a mid-seal durability issue identified in January 2026 introduces execution risk on the Boeing 777X program even as management holds certification timeline expectations

- Full-year departure growth guidance was cut from mid-single-digit to flat-to-low-single-digit, with low double-digit Middle East decline assumed through summer, and any escalation beyond that scenario is not reflected in the current guide

Should You Invest in GE Aerospace?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE Aerospace alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GE stock on TIKR for Free →