Key Stats for Navitas Semiconductor Stock:

- 52-Week Range: $1.80 to $19.79

- Current Price: $18.30

- Street Mean Target: $8.15

- Market Cap: $4.22 billion

- LTM Gross Margin: 31.0%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Power Chip Company Betting on GaN and SiC

Navitas Semiconductor (NVTS) designs power chips built on gallium nitride and silicon carbide, two materials that handle electricity more efficiently than traditional silicon transistors, which have powered electronics for decades. The company’s GaN and SiC semiconductors target applications where heat, speed, and energy density matter most, including fast chargers, electric vehicles, solar inverters, and increasingly, AI data center infrastructure.

The core technology argument is straightforward. GaN chips switch on and off far faster than traditional silicon chips, which means less energy is lost as heat, and power systems can be made smaller without sacrificing performance. For data center operators trying to reduce cooling costs and consumer electronics manufacturers shrinking charger sizes, those efficiency gains translate directly into product differentiation and real operating savings.

Customer relationships in power semiconductors are stickier than they appear. Integrating a new power chip into a product requires validation cycles, thermal testing, and regulatory certification that can take over a year. Once a manufacturer qualifies Navitas components for a fast charger, an EV onboard charger, or a data center power supply, switching means restarting the entire process. That friction creates a durable barrier to displacement once design wins are secured.

See analysts’ growth forecasts and price targets for NVTS (It’s free) >>>

Navitas Semiconductor Stock Financials

Revenue grew from roughly $24 million in 2021 to a peak of $83 million in 2024, then pulled back to $46 million in 2025 as inventory corrections in consumer electronics weighed on volumes. Gross margins have fluctuated between 31% and 45% over that period, settling at 31% on a trailing basis.

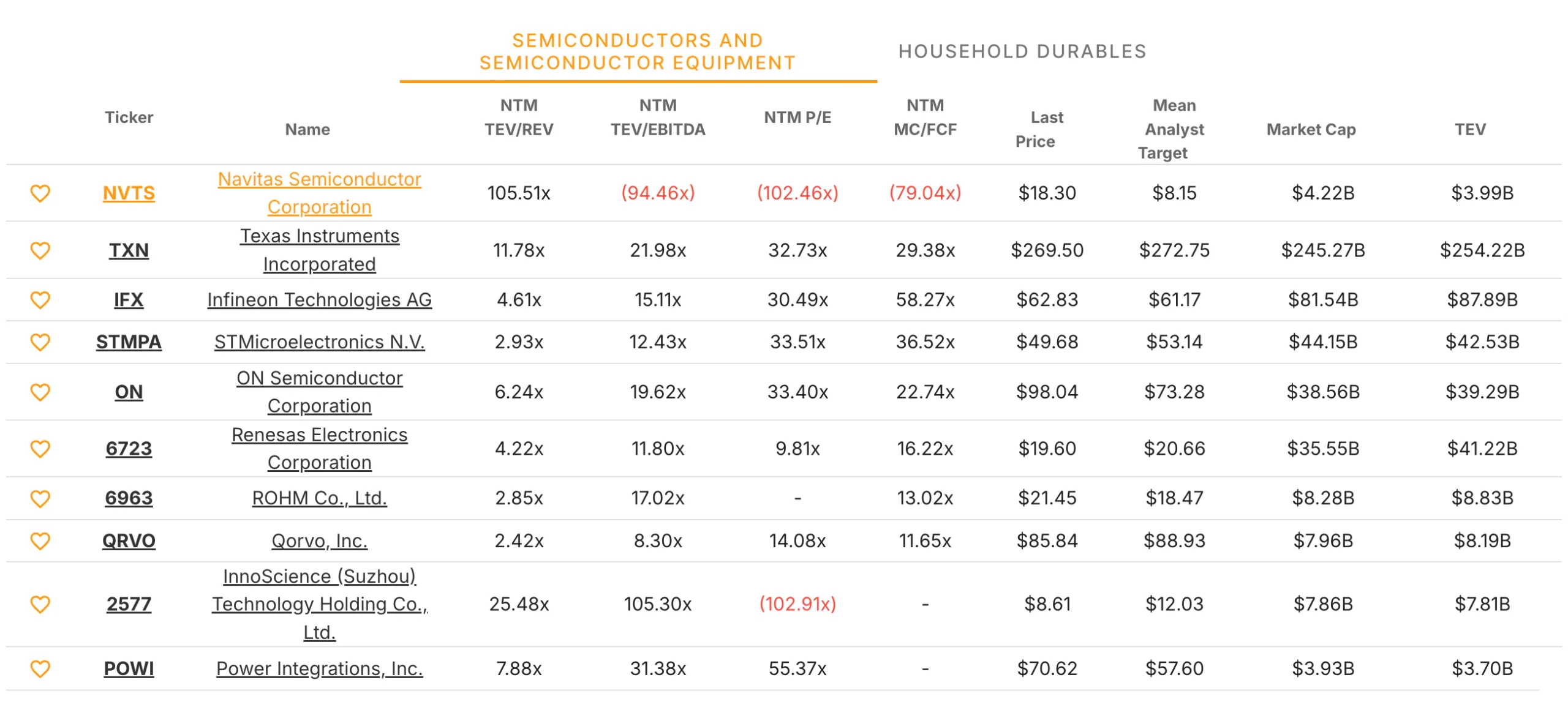

The volatility reflects both product mix shifts and pricing pressure from competing for design wins against well-capitalized incumbents such as Infineon, ON Semiconductor, and STMicroelectronics. Each of those companies has substantially more resources to invest in GaN and SiC capacity, and their ability to bundle power solutions with broader product portfolios gives them a commercial advantage that Navitas cannot yet match at its current scale.

The growth thesis increasingly centers on AI infrastructure as a demand driver alongside EV and consumer electronics markets. Data center power density is rising sharply as GPU clusters replace traditional server configurations, and GaN’s efficiency advantages become more valuable as rack power requirements climb.

The recent appointment of Gregory Fischer, a former Broadcom SVP, to the board signals a deliberate push to bring enterprise semiconductor credibility to those hyperscaler conversations.

Wall Street’s Take on NVTS Stock

The analyst community is notably cautious here. The street consensus target sits at $8.15, more than 55% below the current price of $18.30. That gap reflects a market that has priced in the AI infrastructure narrative well ahead of the revenue and profitability inflection that would justify it on a fundamental basis.

Analysts project revenue to recover to roughly $38 million in 2026, then accelerate to $65 million in 2027 and $122 million in 2028 as demand for AI infrastructure materializes and consumer electronics inventory normalizes. EPS losses are expected to narrow from -$0.18 in 2026 toward -$0.05 by 2028, reflecting operating leverage as volumes scale. The business remains pre-profitable through the forecast period.

At roughly 105 times forward revenue, the valuation multiple leaves very little room for execution misses. The April run that more than doubled the stock from its lows was driven by momentum and thematic enthusiasm rather than a fundamental re-rating, and the spread between where the stock trades and where analysts think it belongs is one of the widest in the semiconductor peer group.

What Has to Go Right for NVTS

The bull case rests on a specific set of conditions coming together in the right sequence.

What Has to Go Right:

- AI data center demand for GaN-based power solutions materializes at scale, and Navitas secures meaningful hyperscaler design wins

- Consumer electronics and EV markets recover from the inventory correction that pressured 2025 revenue

- Gross margins recover toward the 40% range as product mix shifts toward higher-value data center applications

- The company scales revenue fast enough to reach operating leverage before needing to raise additional capital

What Could Go Wrong:

- Larger competitors accelerate their own GaN and SiC investment, compressing Navitas’s technology lead and pricing power

- The AI infrastructure buildout takes longer to translate into power semiconductor procurement than the market currently assumes

- Revenue recovery stalls, extending the pre-profitability period and pressuring a valuation multiple that already assumes significant growth

- The stock’s momentum unwinds as quickly as it arrived, leaving the fundamental setup exposed at current prices

Should You Invest in NVTS?

The technology Navitas is commercializing is real, and the markets it serves are structurally growing. GaN and SiC power semiconductors will play a meaningful role in AI infrastructure, electric vehicles, and next-generation consumer electronics. That part of the thesis is not in question.

At issue is the price. At $18.30 with a street target of $8.15, the stock is trading as though the best-case scenario is already fully reflected. The April surge was driven by momentum, not by a material change in the company’s financial trajectory or a new design win announcement that would change the fundamental picture.

Add NVTS to your TIKR watchlist, track revenue recovery into 2026, and watch for gross margins to return to the 40% range. If the AI infrastructure demand signal arrives in the financials rather than just in the narrative, the setup becomes considerably more interesting. At the current price, patience is the better posture.

Analyze Navitas Semiconductor stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!