Key Takeaways:

- The 2-Minute Valuation Model values ASML stock at $905 per share in 2 years.

- That’s a potential 32% upside from today’s price of $686 per share.

- ASML’s EPS is projected to grow from about $20 in 2024 to $37.29 by 2027, representing an impressive 86% growth over three years.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

ASML (ASML) is the undisputed leader in semiconductor lithography systems. As the sole supplier of extreme ultraviolet (EUV) lithography machines, which are essential for producing advanced semiconductor chips, ASML holds a unique and powerful position in the global technology ecosystem.

With AI and high-performance computing driving demand for cutting-edge chips, the company appears well-positioned for sustained long-term growth.

Let’s analyze ASML’s financial outlook and valuation to determine if the current stock price represents an attractive entry point for investors.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings per share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why ASML Stock Looks Undervalued

Forecast

ASML is projected to deliver impressive earnings growth over the next three years. This growth trajectory shows a temporary dip in 2024, reflecting the current semiconductor industry correction, followed by a rebound starting in 2025 and accelerating through 2027.

The substantial growth in later years aligns with industry projections of a strong semiconductor expansion cycle driven by AI, high-performance computing, and continued digitalization across industries.

This earnings growth for ASML stock is likely to be driven by:

- Monopoly on EUV Technology: ASML is the sole provider of EUV lithography equipment, essential for manufacturing chips at 7nm and below. This technological monopoly creates a wide economic moat and pricing power.

- AI and High-Performance Computing Tailwinds: The explosive growth in AI applications and high-performance computing is driving demand for advanced semiconductors, which can only be manufactured using ASML’s equipment.

- Long-Term Supply Agreements: ASML has secured long-term purchase commitments from major customers like TSMC, Samsung, and Intel, providing earnings visibility and stability.

- Expansion Beyond EUV: It is developing High-NA EUV technology, which will be critical for future semiconductor nodes and represents the next generation of lithography innovation.

- Geopolitical Strategic Importance: Various governments now recognize semiconductor manufacturing as strategically important, leading to subsidies and investments that benefit ASML indirectly.

We’ll assume in our valuation that ASML will reach $37 in EPS in 2027.

Check out ASML’s full analyst estimates (It’s free) >>>

Is ASML Stock Undervalued Right Now?

ASML’s current valuation metrics suggest that the stock could be undervalued relative to its growth prospects.

Over the last 10 years, the tech stock has averaged a forward P/E multiple of 31x, with peaks above 51 during growth-oriented market periods. Currently, ASML stock trades at about 26 times forward earnings.

This compressed valuation could reflect broader market concerns about semiconductor industry cyclicality and near-term headwinds.

However, it may not fully account for ASML’s monopolistic position in EUV lithography and its critical role in enabling advanced semiconductor manufacturing.

We’ll use a conservative forward P/E multiple of 24x for our valuation, which is below the current and historical average trading multiple.

Fair Value of ASML Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $37

- Conservative forward P/E multiple: 24x

- Expected dividends over the next 2 years: $17

Expected Normalized EPS ($37) * Forward P/E ratio (24x) + Expected Dividends ($17) = Expected Share Price ($905)

The 2-year expected ASML stock price we would get from this valuation is $905 per share.

With ASML stock currently trading at around $686 per share, this implies a potential upside of 32% over the next two years or a 15% annualized return.

Remember, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

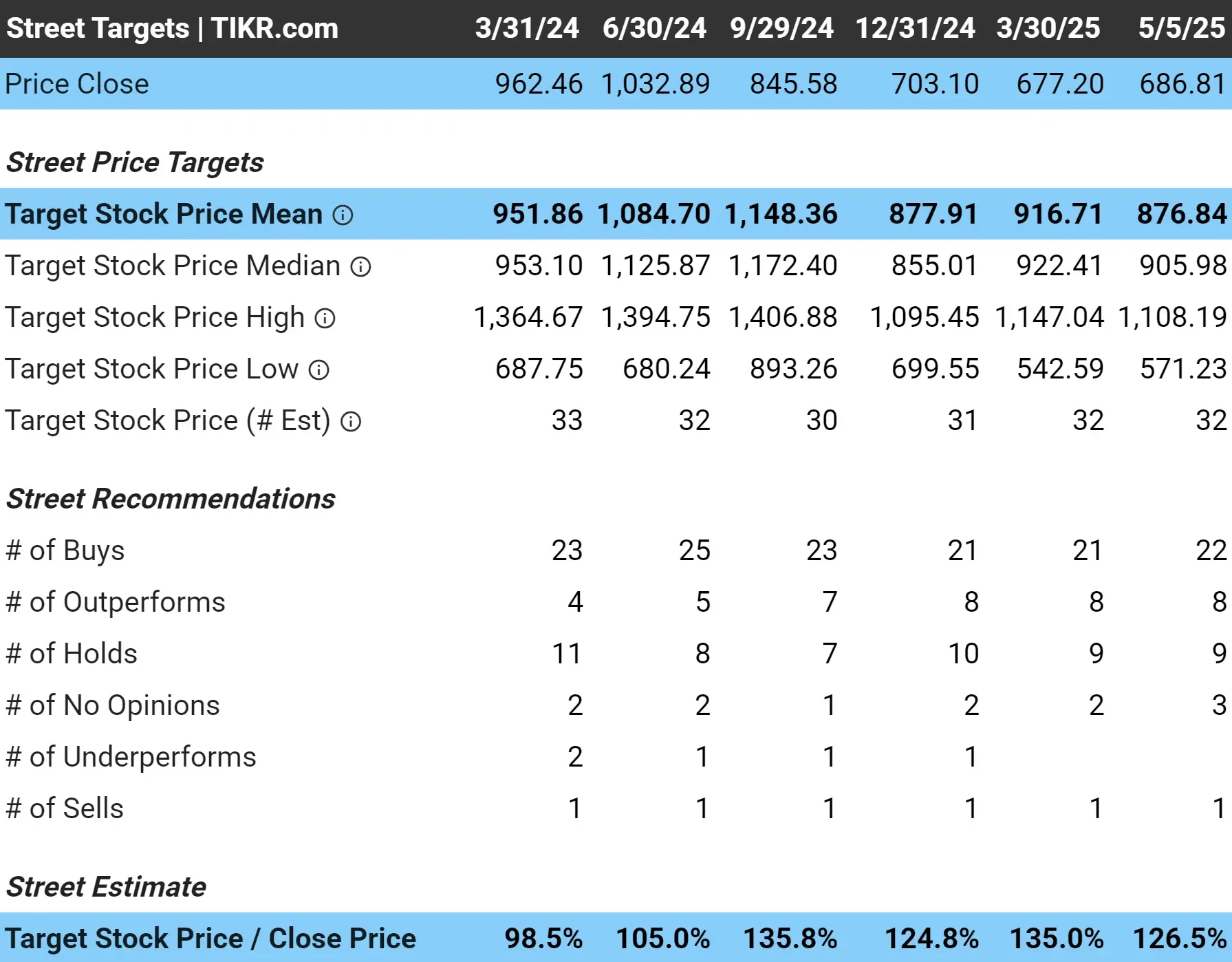

What is the Target Price for ASML Stock?

Analysts have an average price target of around $878 per share for ASML stock, indicating they see nearly 27% upside today for the chip maker based on the stock’s current share price:

Risks to Consider

Even though our valuation suggests the stock could be worth around $905 per share, investors should be aware of several risks for the stock:

- Semiconductor Cyclicality: The semiconductor industry is notoriously cyclical, with periods of overinvestment followed by corrections that can impact ASML’s near-term results.

- Geopolitical Tensions: Ongoing US-China trade tensions could restrict ASML’s ability to sell to Chinese customers, limiting its total addressable market.

- Concentration Risk: ASML relies heavily on a small number of large customers (TSMC, Samsung, Intel), creating vulnerability if any single customer reduces capital expenditures.

- High Valuation Relative to Market: While below its historical average, ASML’s forward P/E remains above the broader market, limiting upside if tech sector valuations fall.

- Execution Challenges: Developing and producing complex lithography systems presents technical challenges that could lead to delays or cost overruns.

TIKR Takeaway

ASML represents a unique opportunity to invest in a company with a virtual monopoly on technology essential to semiconductor advancement.

Its projected earnings growth and its current valuation below historical averages create an attractive entry point for long-term investors.

While near-term semiconductor industry challenges may create volatility, ASML’s position in the semiconductor supply chain and the structural growth drivers of AI, high-performance computing, and digitalization provide a strong foundation for long-term outperformance.

Is ASML stock a buy over the next 24 months? Use TIKR to check the stock’s analyst price targets and growth forecasts to see if it is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!