Key Stats for AMD Stock

- Thursday Performance: -5%

- 52-Week Range: $149 to $585

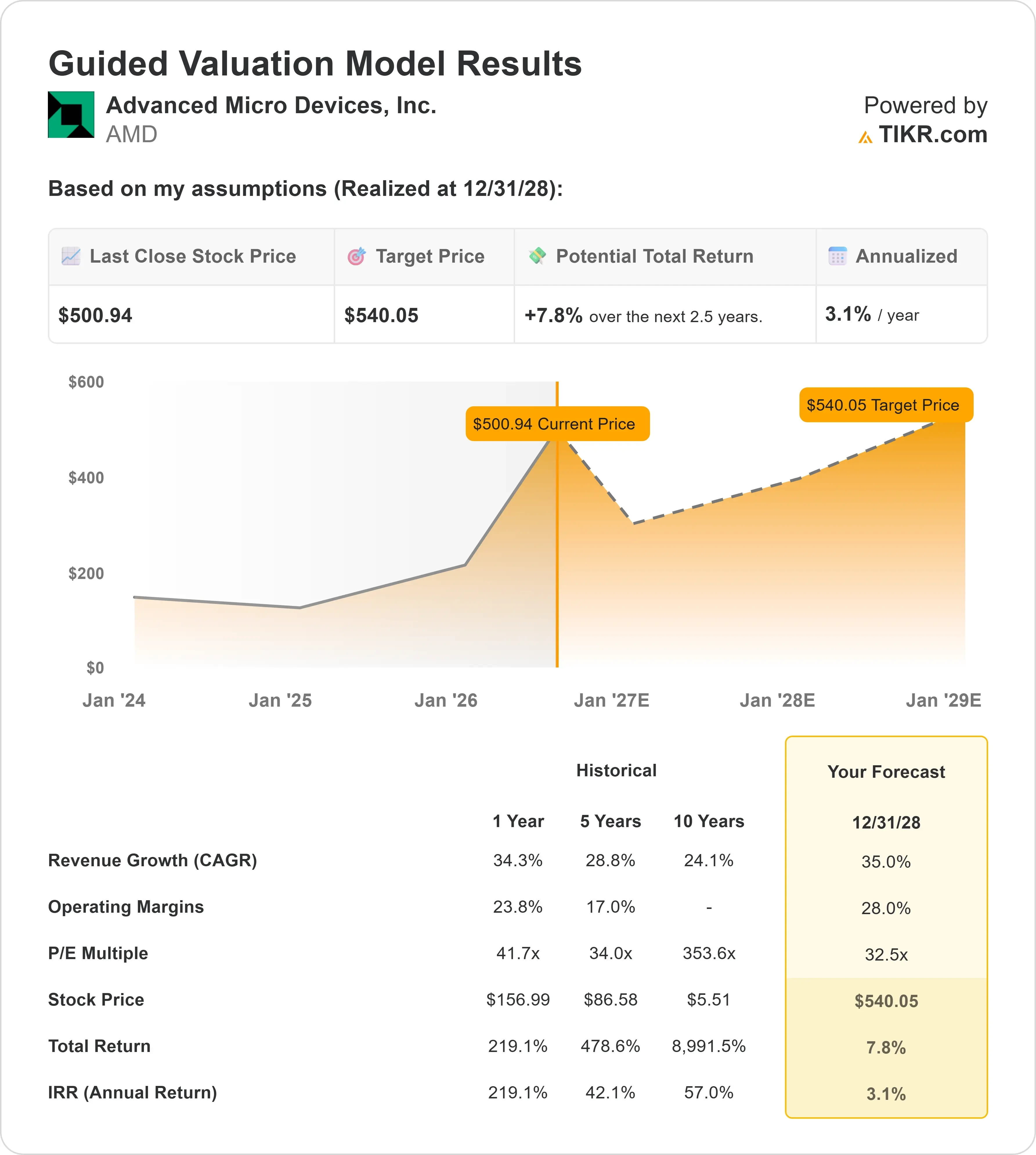

- Valuation Model Target Price: Around $540

- Implied Upside: Around 8%

Analyze your favorite stocks like Advanced Micro Devices with TIKR (It’s free) >>>

What Happened?

AMD has become one of Wall Street’s clearest bets on the emergence of a credible alternative to Nvidia in AI computing, but that optimism also makes the stock vulnerable when confidence in the industry’s spending boom weakens. That tension surfaced Thursday as AMD shares fell 5% to $501 during a broad semiconductor selloff. The stock traded between $492 and $519 before finishing near the session low, showing that selling pressure persisted through the close.

AMD fell because investors took profits in high-performing AI stocks and questioned whether massive data center investments would continue generating adequate returns. The Philadelphia Semiconductor Index dropped 4%, while AMD, Intel, and Micron each declined between 5% and 6%, confirming that the weakness extended across the industry. AMD competes primarily with Nvidia in AI accelerators and integrated server systems and with Intel in server processors. Although the companies define their segments differently, AMD’s latest Data Center revenue grew 57% to $5.8 billion, compared with Nvidia’s 92% growth to $75.2 billion and Intel’s 22% growth to $5.1 billion, showing that AMD is growing faster than Intel while Nvidia remains much larger in data-center revenue.

At Bank of America’s June technology conference, AMD CFO Jean Hu said the company’s server CPU business, which sells processors used in data centers, grew more than 50% in Q1 and is expected to grow more than 70% year over year in Q2, with roughly two-thirds of that growth coming from higher unit volumes. Hu said, “The demand is tremendous, supply is still tight,” and explained that AMD has worked with TSMC to secure capacity for the ramp. AMD expects to begin launching its MI450 AI accelerator in Q3, while customers are already testing full Helios AI server racks with production workloads. Management expects significant revenue increases in Q4 2026 and Q1 2027, while OpenAI’s and Meta’s 2027 forecasts exceed AMD’s original plans.

Wall Street remained bullish despite Thursday’s decline. KeyBanc raised its price target to $725 from $530, Bank of America lifted its target to $620 from $550, and TD Cowen increased its target to $675 from $600, with the firms emphasizing server processor demand and the expected MI450 and Helios ramp. EPYC is AMD’s family of server processors that competes with Intel’s Xeon chips, while Helios provides customers with a complete AI server rack and an alternative to Nvidia’s integrated systems. AMD’s Advancing AI event on July 22 and 23 and second-quarter earnings on August 4 will test whether strong customer forecasts are translating into Helios deployments, MI450 shipments, and reported revenue.

Value Advanced Micro Devices instantly (Free with TIKR) >>>

Is AMD Fairly Valued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): Around 35%

- Operating Margins: Around 28%

- Exit P/E Multiple: Around 33x

The 35% revenue-growth assumption requires AMD to expand EPYC server-processor supply, begin MI450 shipments on schedule, and convert customer forecasts and orders into shipments and recognized revenue.

The 28% operating-margin assumption depends on a richer Data Center mix and operating leverage, while spending on MI450, Helios, software, and supply readiness could limit near-term expansion.

See analysts’ growth forecasts and price targets for Advanced Micro Devices (It’s free) >>>

The 33x exit P/E is close to AMD’s five-year average of 34x and below its current next-12-month multiple of around 57x, meaning the model assumes substantial valuation compression rather than relying on a higher multiple.

Through the remainder of 2026, the largest business drivers are the Helios launch, Venice, AMD’s next-generation EPYC server processor, and improvements to ROCm, AMD’s open software stack for running AI workloads and its answer to Nvidia’s CUDA ecosystem.

Based on these inputs, the model estimates a target price of around $540 by the end of 2028, implying around 8% total upside and around 3% annually from the $501 closing price, leaving AMD fairly valued with future returns dependent on product execution and market-share gains.

How Much Upside Does AMD Stock Have From Here?

Investors can estimate Advanced Micro Devices’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Advanced Micro Devices in under 60 seconds with TIKR (It’s free) >>>