Key Takeaways:

- United has achieved a “structural, permanent and irreversible” transformation by winning brand loyal customers across its hub network.

- The airline is demonstrating remarkable resilience with the highest first-quarter pretax margin since COVID began, even in a weak economic environment.

- United’s revenue diversification strategy and operational excellence position it to outperform competitors during economic downturns.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

United Airlines (UAL) has emerged from the pandemic as a fundamentally transformed airline. Despite challenging macroeconomic conditions, it delivered Q1 earnings per share of $0.91 and achieved a 3% pretax margin.

Under CEO Scott Kirby’s leadership, United has successfully executed its “United Next” strategy, winning brand loyal customers and creating what management calls a “structural, permanent and irreversible” competitive advantage.

The United Airlines stock price today reflects investor concerns about the broader economic environment and softening travel demand, particularly in the government and domestic leisure segments.

However, the UAL stock price may not fully capture the airline’s strengthened competitive position and improved earnings resilience that should drive long-term outperformance.

For investors considering United Airlines stock, three key factors distinguish United from its peers and suggest the company is well-positioned to deliver strong returns even during economic uncertainty.

Let’s dive deeper.

1. Brand Loyalty Leadership Driving United Airlines Stock Outperformance

United Airlines has achieved market leadership in six of its seven hubs and significantly expanded its share of brand loyal customers across key markets.

This transformation represents the core thesis behind UAL stock’s investment appeal. The airline giant has moved from competing primarily on price to winning customers through superior service, product quality, and loyalty programs.

In Chicago, United expanded its passenger share lead of local origin traffic to 22 points ahead of its next largest competitor in Q4 of 2024, up from just 6 points in 2019.

Similarly, in Denver, United increased its gap ahead of its largest competitor to 10 points for Denver-based passengers. The airline also gained 2.1 points of market share in the Bay Area, demonstrating continued momentum in competitive markets.

This brand loyalty advantage creates what Kirby describes as a “spill airline” dynamic, where competitors can only gain passengers through lower prices.

During economic downturns, brand-loyal airlines like United maintain better pricing power while spill carriers face disproportionate pressure.

CFO Mike Leskinen noted that United expects to be one of only two airlines profitable in Q1, highlighting this competitive advantage that should continue to benefit United Airlines stock.

The loyalty transformation is further evidenced by credit card sign-up growth, with Denver and Chicago seeing over 100% growth in credit card acquisitions from 2019 to 2024.

These brand loyal customers tend to remain with the airline for decades, providing a stable revenue foundation that supports UAL stock through economic cycles and creates a sustainable moat for the business.

Find the best stocks to buy today with TIKR. (It’s free) >>>

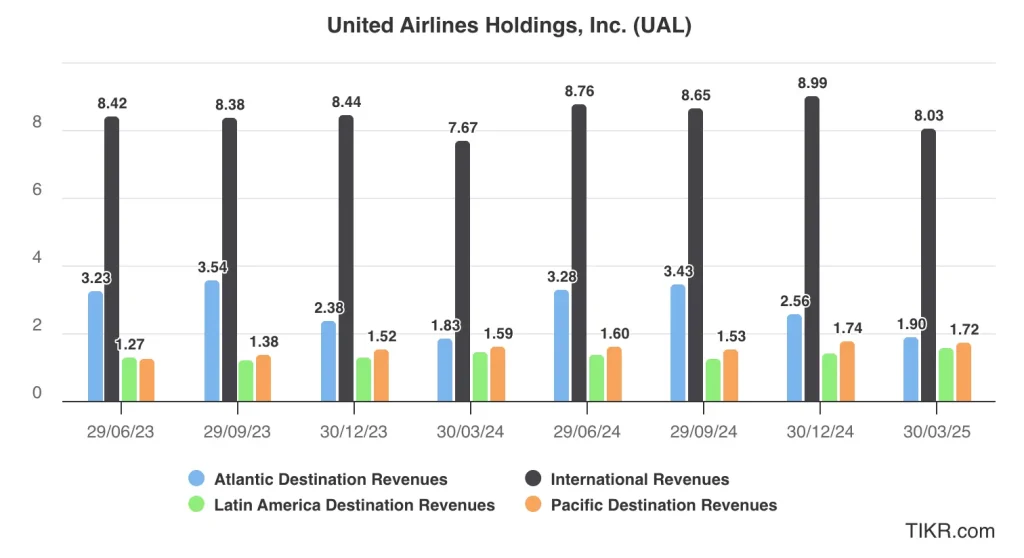

2. Revenue Diversification Strengthening UAL Stock Resilience

United’s diversified revenue streams provide downside protection compared to competitors more dependent on single revenue sources.

The airline has successfully cracked multiple market segments: price-sensitive customers through Basic Economy, domestic road warriors through fee elimination, premium travelers through enhanced products, and international markets through its extensive wide-body fleet.

These diversification efforts should continue to support United Airlines stock across various economic cycles.

International operations remain particularly strong, with international Polaris unit revenues up 8% and premium plus revenues up over 5% in Q1. United’s international franchise benefits from structural supply constraints, as many competitors retired aircraft during the pandemic and haven’t replaced them.

Additionally, airport slot constraints in major international markets create significant barriers to entry for new capacity. Premium cabin performance continues to outpace the main cabin, with overall premium unit revenues up mid-single digits in Q1.

This premiumization strategy, supported by investments in Polaris lounges, improved food service, and enhanced in-flight WiFi through Starlink deployment, creates sustainable revenue premiums.

The loyalty program represents another diversified revenue stream that grew 9% to $1.5 billion in Q1, with co-brand spending also up 9%. This revenue source has proven remarkably resilient through various economic cycles, providing stability for UAL stock investors.

United’s ability to maintain positive revenue growth even during demand weakness, with Q1 revenue up 5.4% to a record $13.2 billion, demonstrates the effectiveness of this diversification strategy and provides confidence in the long-term outlook for UAL stock.

Check out UAL’s full analyst estimates (It’s free) >>>

3. Operational Excellence and Cost Management Supporting United Airlines Stock

United’s operational improvements and cost management capabilities should support UAL stock during challenging periods. In Q1, the airline achieved its highest NPS scores and best on-time arrival performance since the pandemic, while maintaining the second-lowest first-quarter seat cancellation rate in company history.

These operational improvements directly translate to customer satisfaction and loyalty, further strengthening the investment case for United Airlines stock.

Management’s disciplined approach to capacity and cost management was evident in Q1, when the airline delivered CASM-ex growth of only 0.3% year over year despite inflationary pressures. As demand softened in February, United quickly adjusted by early retiring 21 aircraft, reducing capacity in less profitable routes, and eliminating red-eye utilization flying.

The company’s “no excuses” philosophy ensures management will take necessary actions to meet financial guidance. For 2025, United provides a base case scenario targeting $11.50-$13.50 EPS. Even in a recessionary scenario, the airline expects to earn $7-$9 per share, marking the first time United has remained profitable through a recession.

United’s balance sheet strength supports these operational capabilities, with $18.3 billion in liquidity and net leverage reduced to 2.0x. The airline generated over $2 billion in free cash flow in Q1 and has produced over $5 billion in free cash flow over the past 12 months, representing a 20% free cash flow yield at current valuation.

This operational resilience, strategic capacity adjustments, and cost flexibility positions UAL stock to deliver strong relative performance even during economic downturns.

Value stocks quicker with TIKR (It’s free, no card required) >>>

Valuation Setup for UAL Stock

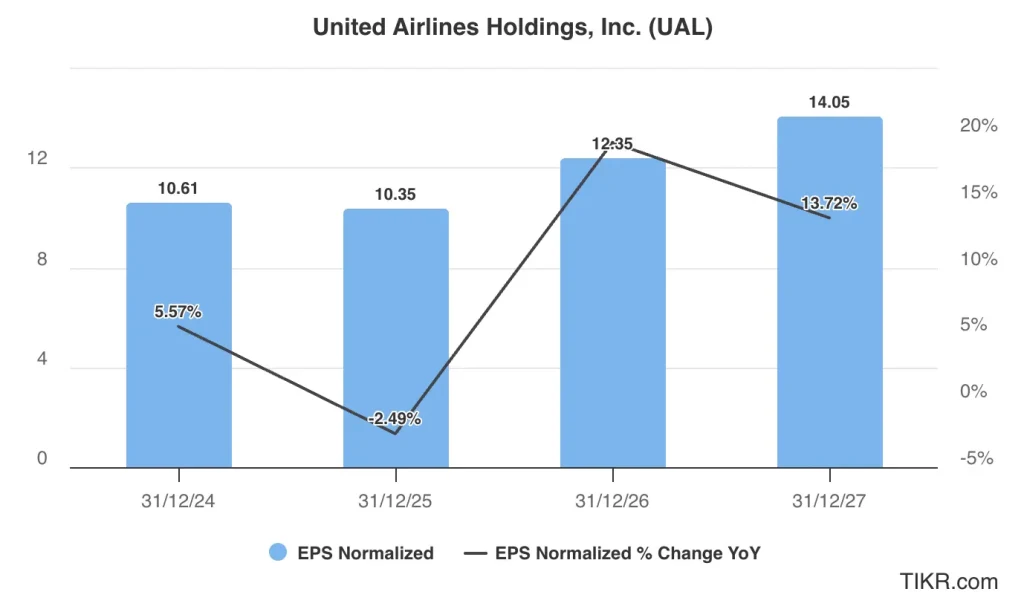

Analysts tracking UAL stock expect normalized earnings per share to expand from $10.61 per share in 2024 to $14.05 per share in 2027.

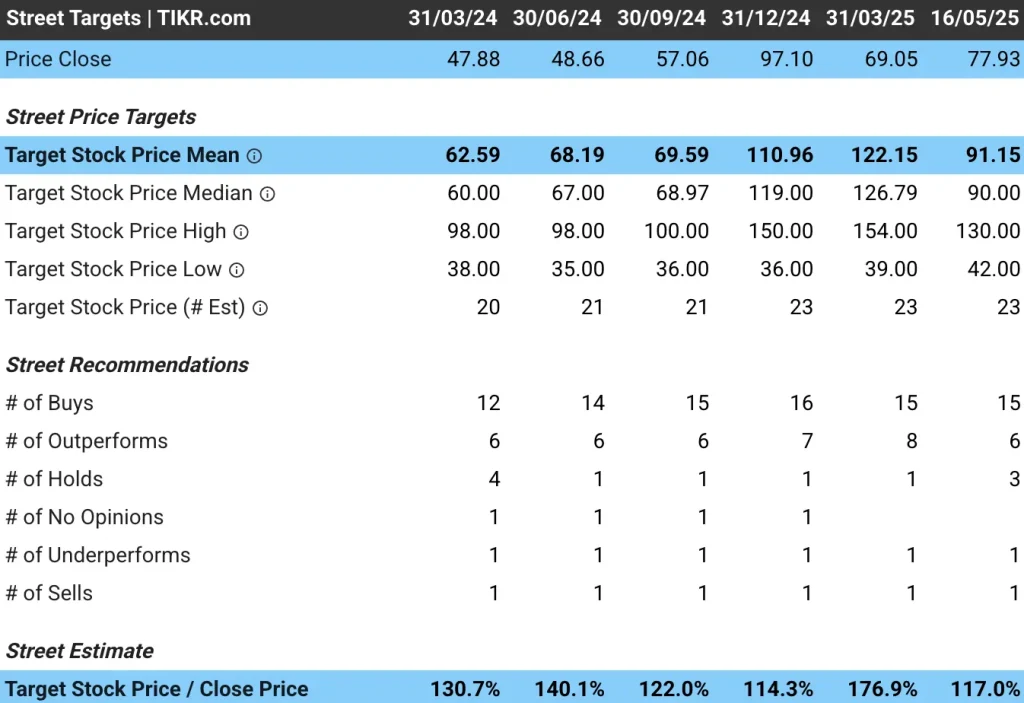

United Airlines stock trades at a forward price-to-earnings multiple of 7.4x, above its three-year average of 6x. If UAL stock is priced at 7x forward earnings, it will trade around $98 per share in early 2027, above the current price of $78.

Analysts tracking UAL stock have an average target price of $91, indicating a potential upside of 17% from current levels.

Out of 26 analysts who track United Airlines stock, 21 recommend “Buy,” three recommend “Hold,” and two recommend “Sell.” Analysts have a high target price of $130, while the lowest price target for UAL stock is $42.

TIKR Takeaway for United Airlines Stock

United Airlines has transformed from a traditional network carrier to a brand loyalty leader with diversified revenue streams and operational excellence.

While United Airlines stock faces near-term pressure from economic uncertainty, its structural advantages position it for outperformance during challenging periods.

For investors seeking exposure to the airline sector with downside protection and upside potential, UAL stock represents a compelling investment opportunity at current valuations.

Is United Airlines stock a buy over the next 24 months? Use TIKR to check the stock’s analyst price targets, 5-year growth forecasts, and see if the stock is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!