Key Stats for WTW Stock

- Past-Week Performance: -2%

- 52-Week Range: $276 to $353

- Current Price: $302

What Happened to WTW Stock?

Willis Towers Watson, more recognized as WTW, dropped 1.7% yesteday to $296.6 after shares plunged 12.1% on February 10 when Insurify launched an AI-powered insurance comparison tool built on ChatGPT, triggering a sector-wide selloff that dragged the entire U.S. insurance brokerage industry sharply lower.

The sharpest selling pressure came from the broader market’s reaction to Insurify’s ChatGPT-powered platform, which sparked a 3.9% single-day collapse in the S&P 500 Insurance index on February 10, its largest drop since October 2025, pulling WTW down alongside peers Aon and Arthur J. Gallagher.

Beneath the AI-driven panic, WTW’s own fundamentals told a stronger story, as the company delivered Q4 adjusted EPS of $8.12, growing 13% year-over-year excluding TRANZACT, while Corporate Risk & Broking posted its 12th consecutive quarter of high single-digit organic growth.

Nevertheless, the market continues re-rating WTW away from a legacy insurance broker toward a diversified specialty platform, with free cash flow surging to $1.5 billion at a 15.9% margin and three acquisitions, Newfront, Cushon, and FlowStone, reshaping its growth and technology profile simultaneously.

CEO Carl Hess stated on the Q4 earnings call that “our strategic investments in talent and innovation in 2025 have accelerated performance,” underscoring a strategy that drove 5% full-year organic growth and 130 basis points of adjusted operating margin expansion to 25.2%.

Adding to the conviction, JPMorgan analysts stated on February 10 that genuine AI disruption is “likely to take some time, at least 24 months,” calling the selloff overdone, while Piper Sandler labeled the dip a “potential buying opportunity for the insurance brokers.”

Looking further ahead, WTW’s expanding data center insurance franchise, now supporting 5 of the 10 largest global developers, its reinsurance JV, and its Newfront-powered technology platform collectively position the company to capture structurally higher-margin specialty revenue over the next three to five years.

Wall Street’s Take on Willis Towers Watson Stock

Despite the AI-driven selloff that knocked WTW down 12.1% on February 10, the stock’s fundamental trajectory points firmly higher as three acquisitions close, Newfront already integrated as of January 27, and Cushon and FlowStone expected to add roughly $300 million in combined annual revenue.

The fundamental case remains compelling, as WTW projects revenue climbing 8.7% to $10.6 billion in 2026 while expanding its EBIT margin to 25.7% and growing normalized EPS to $19.7, continuing a steady multi-year earnings compounding story that the current selloff obscures.

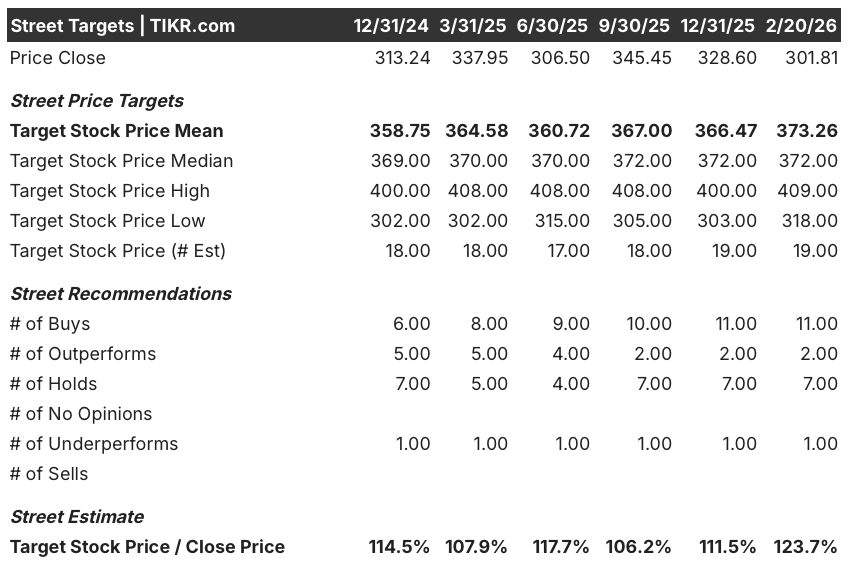

Wall Street stands firmly behind WTW, with 13 combined buy and outperform ratings against just 7 holds and 1 underperform, and a mean price target of $373.3 representing 23.7% upside from the February 20 close of $301.8.

The analyst target range reinforces the conviction, with the low target of $318.0 already sitting above the current price while the high target of $409.0 implies upside exceeding 35%, signaling that even the most cautious analysts see the AI-driven selloff as an overshoot.

What Does the Valuation Model Say?

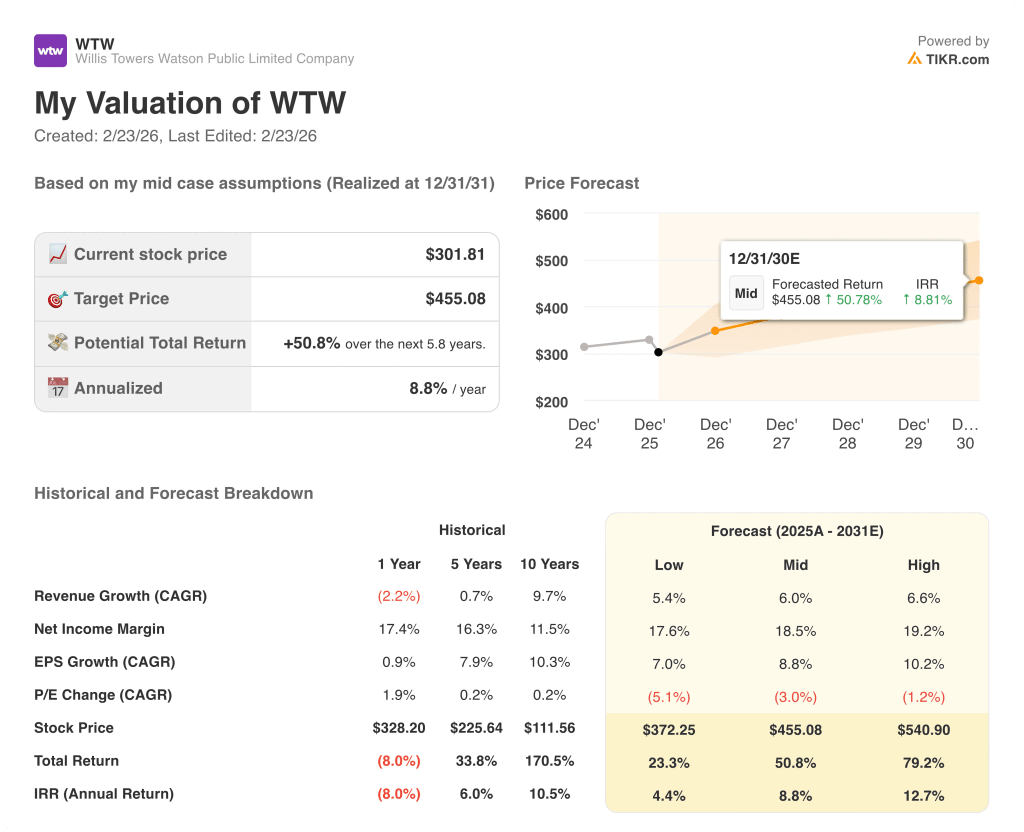

Reinforcing that view, a mid-case valuation model built on WTW’s 5% organic growth momentum, its $1.5 billion free cash flow base, and its accelerating specialty broking platform prices WTW at $455.1, implying a 50.8% total return and an 8.8% annualized IRR through December 2030.

In summary, the primary risk centers on multiple compression, as the model projects a 3.0% annual P/E contraction through the forecast period, meaning WTW must sustain consistent earnings growth just to offset valuation headwinds from a normalizing market environment.

At $296.6, WTW trades at a clear discount to every forward-looking measure available, making it an undervalued entry point for investors who look past the short-term AI disruption narrative and focus on the company’s deepening specialty platform and acquisition-driven growth runway.

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.