Key Stats for Paycom Stock

- 3 Months Price change for Paycom stock: -28%

- $PAYC Share Price as of Feb. 20: $115

- 52-Week High: $268

- $PAYC Stock Price Target: $151

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

What Happened?

Valued at a market cap of $6 billion, Paycom (PAYC) stock is down 25% in 2026. It tumbled 5% after after the cloud-based human capital management company reported fourth-quarter results and issued disappointing guidance for fiscal 2026.

While the company met Wall Street expectations for the quarter, its outlook for the coming year fell short of investor hopes.

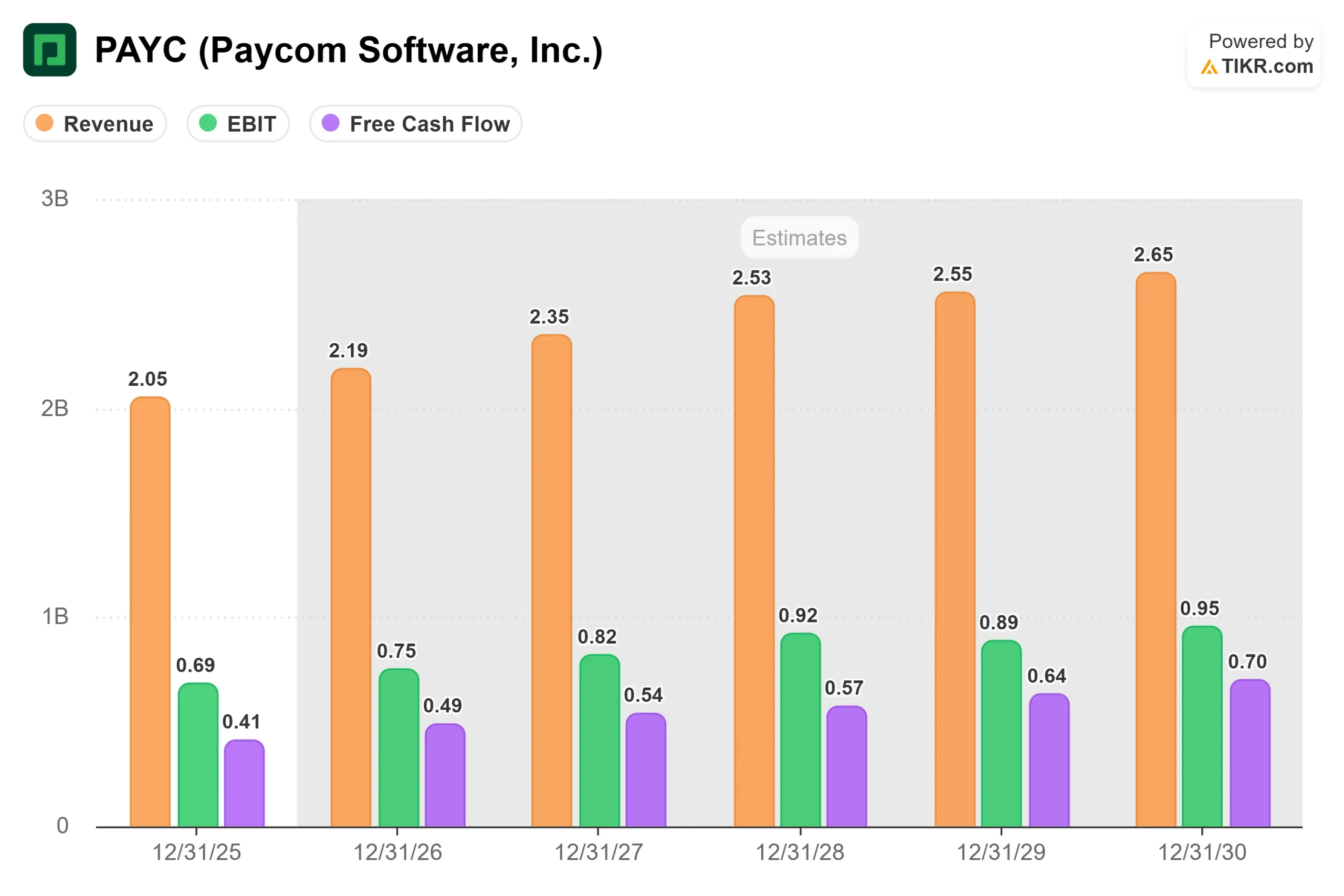

- Fourth-quarter revenue came in at $542.9 million, up 10.2% year-over-year and right in line with analyst estimates. Adjusted earnings per share of $2.45 also matched expectations.

- For the full year 2025, total revenue reached $2.05 billion with recurring revenue growth of 10%, ahead of the company’s initial 9% growth expectation.

- The problem was the forward guidance. Paycom issued fiscal 2026 revenue guidance of $2.175 billion to $2.195 billion, representing just 6% to 7% growth.

- This marks a deceleration from the 9% total revenue growth the company just posted for 2025, and came in below what many investors were expecting.

- The recurring revenue outlook was slightly better at 7% to 8% growth, but still represented a slowdown from the 10% achieved in 2025.

- The company’s initial 2025 guidance was 7% to 8% total revenue growth, and it ended up beating that by a full percentage point. This year’s 6% to 7% guide is about 1 percentage point lower than last year’s initial outlook.

CEO Chad Richison acknowledged that the company has opportunities to improve sales execution. He said Paycom has been focused on retraining its entire sales organization over the past three months to better communicate the value of the company’s “full solution automation” strategy.

The company recently brought in all its salespeople to ensure they understand the new product enhancements released since November that automate large portions of the system.

Richison emphasized that the company is not seeing any reluctance from prospects to buy Paycom’s products.

However, he noted that consumers and clients often have difficulty digesting the concept of full solution automation, so the company is working on how to better “plate” the value proposition.

Despite the sales challenges, Paycom did report some encouraging metrics. Annual revenue retention improved to 91% in 2025, up from 90% in 2024.

The company also experienced a record number of clients returning to the Paycom platform after leaving for what they perceived as lower-priced alternatives, only to find those solutions cost them “10x” more in the long run.

Client count grew 4% to approximately 39,200, with parent company groupings up 5% to about 20,300.

Revenue from clients with over 1,000 employees grew faster than total revenue, indicating continued upmarket momentum.

See analysts’ growth forecasts and price targets for PAYC stock (It’s free!) >>>

What the Market Is Telling Us About Paycom Stock

The sharp decline in Paycom stock reflects investor concerns that growth is decelerating despite the company’s heavy investment in AI and automation technology.

The stock is now down over 47% in the past year, significantly underperforming the broader market.

There are some positives worth noting.

- Paycom delivered very strong profitability metrics, with adjusted EBITDA margins of 43% in 2025, representing 180 basis points of margin expansion.

- The company generated $679 million in operating cash flow, up 27% year-over-year, and

- free cash flow of $404 million, up 20%.

- These metrics demonstrate that the business model remains highly profitable and cash-generative.

- The company’s IWant AI solution is gaining significant traction. Usage was up 80% in January alone compared to the fourth quarter.

- Forrester Research found that organizations using IWant experienced an ROI of over 400%, with managers saving up to 600 hours per year and employees collectively reclaiming 3,600 hours annually.

- IWant appears to be contributing to improved client retention as customers realize the productivity benefits.

- Paycom’s automation tools, such as Beti (which reduces payroll processing labor by up to 90%) and GONE (which automates PTO requests), represent genuine innovations that deliver measurable ROI for clients.

- The company argues it has the most automated HCM solution on the market, which should be a competitive advantage as labor costs rise and companies seek efficiency gains.

- However, the market is clearly skeptical about whether these product innovations will translate into accelerated growth.

- Paycom Software stock has been hit hard by concerns that AI could actually disrupt the company’s business model if emerging AI tools make it easier to handle HR and payroll tasks without traditional software platforms.

Management pushed back strongly against this narrative, with Richison stating that “AI is our friend at Paycom” and that the company can now develop new products and enter adjacent markets “within weeks or months” using AI development tools.

He positioned Paycom as well-suited to use AI to displace other industries that depend on payroll and HR data.

The company also made a change in sales leadership at the beginning of the year, which could signal that management recognizes execution issues need to be addressed.

Richison emphasized the focus is now on “quality over quantity” in sales, ensuring clients purchase for the right reasons and understand the full value of automation upfront.

Analysts remain cautiously optimistic despite the weak guidance. The consensus rating is “Moderate Buy” with a mean price target of $173, implying about 45% upside from current levels.

However, Jefferies analyst Samad Samana cut his price target to $130 from $190 while maintaining a Hold rating, reflecting concern about the growth trajectory.

For fiscal 2026, analysts expect EPS to grow 13.5% to $8.09, suggesting they believe profitability will remain strong even if revenue growth moderates.

The key question is whether Paycom can re-accelerate growth through improved sales execution or whether the 6% to 7% revenue growth guidance represents a new normal for the business.

Investors should watch for signs that the sales retraining is paying off, whether client retention continues improving toward historical levels, and whether the company can demonstrate that its AI and automation investments are translating into market share gains rather than just margin expansion.

Estimate a company’s fair value instantly (Free with TIKR) >>>

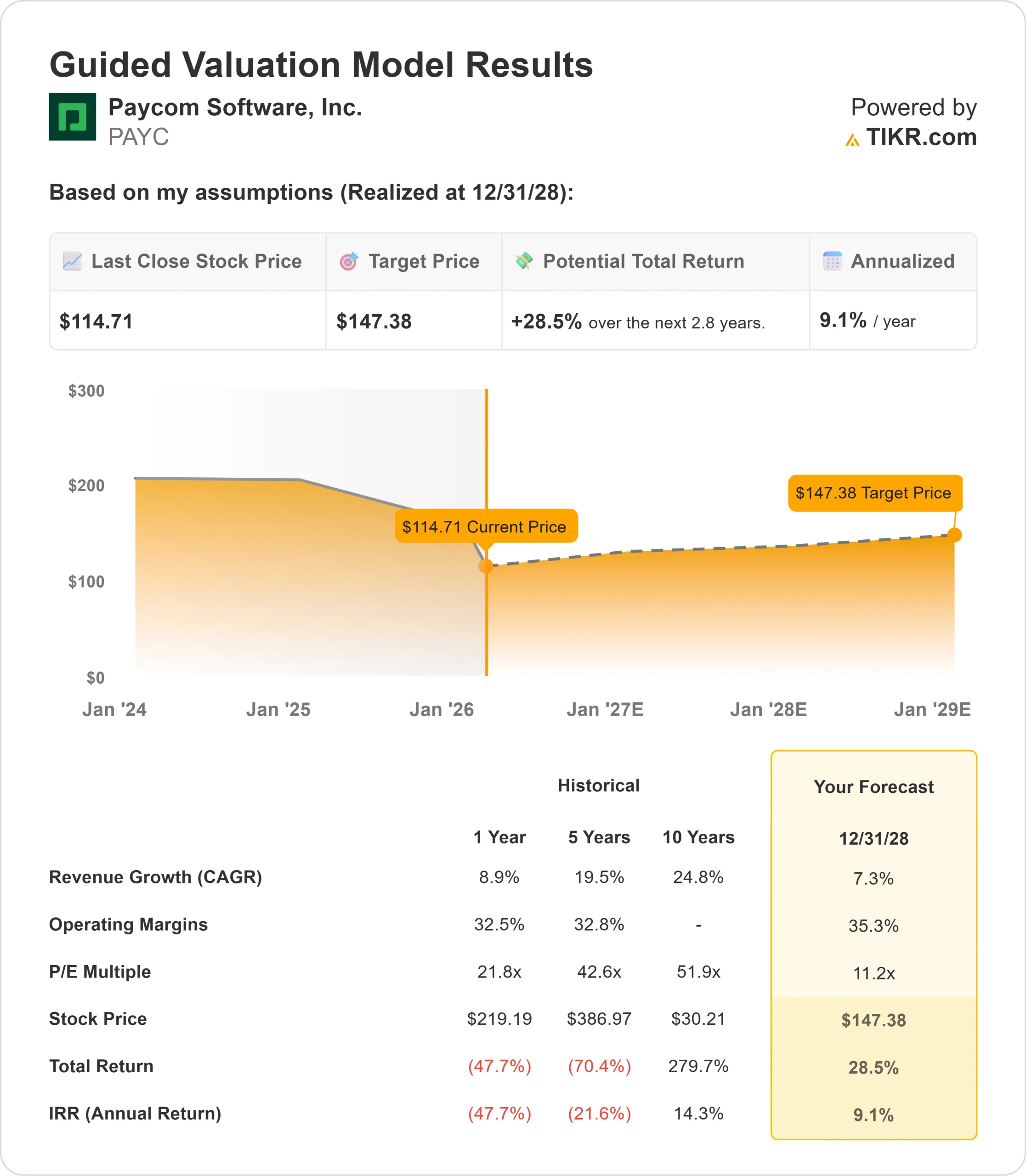

How Much Upside Does PAYC Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!