Key Takeaways:

- The Payout Promise: Management dropped a bombshell for income investors, confirming plans to increase shareholder distribution to “close to around 100% payout” for 2026 and 2027.

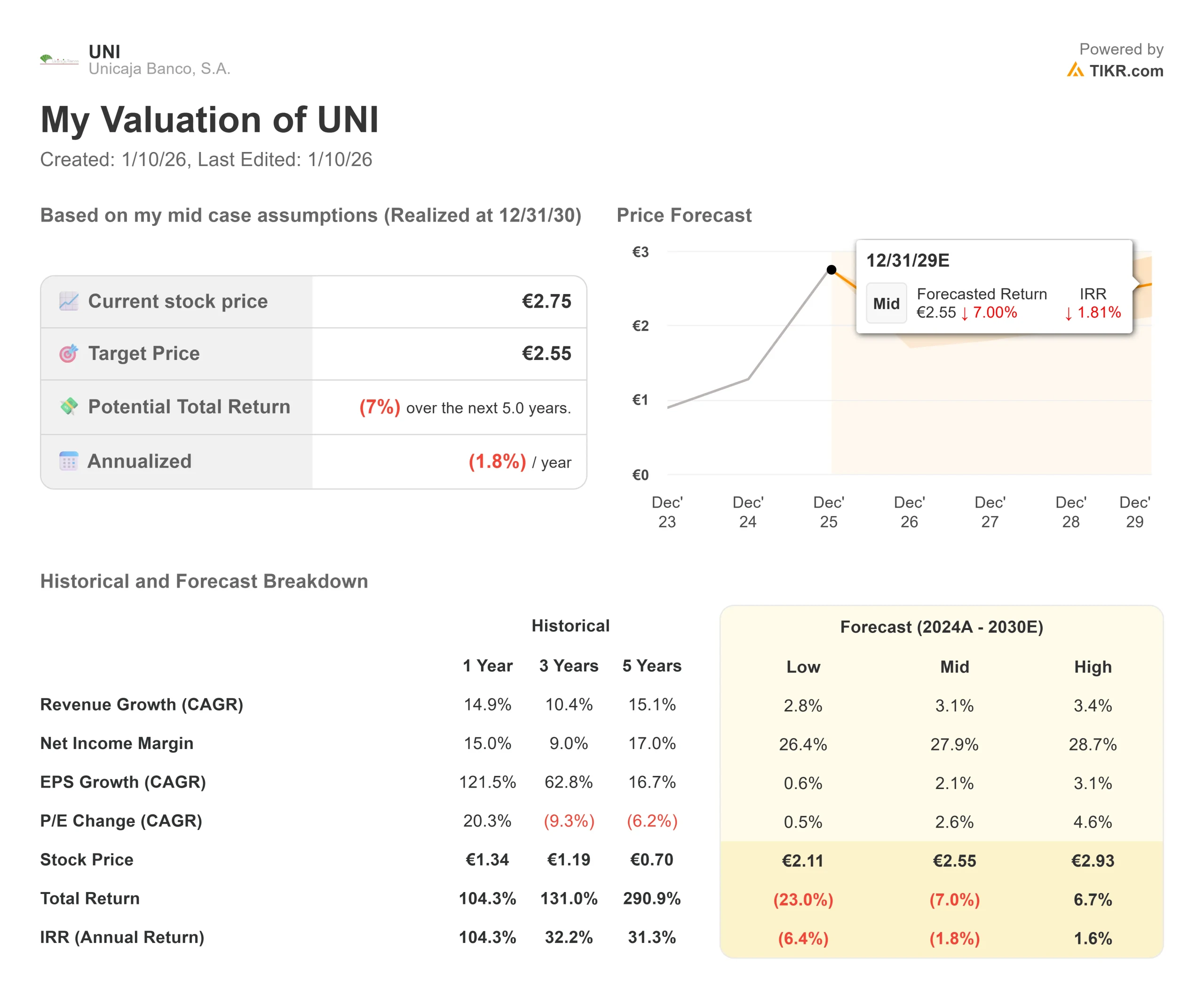

- Price Projection: Despite the generosity, our model suggests the stock price could drift down to €2.64 by December 2027.

- Expected Returns: This target implies a disappointing -2.0% annualized return, warning that the stock may be “dead money” at current levels.

- Guidance Bump: The bank raised its Net Interest Income (NII) guidance for 2025 to above €1.47 billion, citing resilience in customer spreads.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Unicaja Banco (UNI) is doing everything right to woo investors.

The Spanish lender has aggressively improved its profitability, with net income reaching €451 million in the first nine months of 2025, a massive improvement from previous years.

Even better, management is doubling down on returning cash to shareholders. In a recent call, they confirmed a strategy to distribute excess capital, targeting an 85% payout ratio in the short term and moving toward 100% for 2026 and 2027.

With the stock trading at €2.75, this sounds like a dividend dream. But is the market pricing in too much optimism?

While the yield is attractive, the underlying stock price faces headwinds from falling interest rates and a valuation that sits well above its historical average.

See analysts’ full growth forecasts and estimates for Unicaja Banco stock (It’s free) >>>

What the Model Says for UNI Stock

We evaluated Unicaja’s potential through 2027, balancing the lucrative capital return plans against the reality of a normalizing rate environment.

Our model suggests investors should tread carefully. Using a forecast of 1.4% Revenue Growth (CAGR) and 52.5% Operating Margins, the model projects the stock will settle around €2.64 by the end of 2027.

This implies a -2.0% annualized return over the next two years.

The thesis here is simple: The dividends you receive might be largely cancelled out by a slow decline in the share price as the valuation multiple compresses.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for UNI stock:

1. Revenue Growth: 1.4%

The “repricing” headwind is still blowing.

Management admitted that they still face “a couple more quarters of impact” from the repricing of their floating-rate loan book (mainly mortgages) as the Euribor falls.

However, they successfully offset this with lower deposit costs, leading them to raise 2025 NII guidance to >€1.47 billion.

Private sector lending also showed signs of life, growing 39% year-on-year to €7.1 billion in new production.

We forecast modest revenue growth of 1.4% CAGR through 2027, as volume growth battles against lower interest margins.

2. Operating Margins: 52.5%

Unicaja’s cost of risk is performing better than expected, currently tracking at 24 basis points, below their initial guidance of 30 bps.

Non-performing loans (NPLs) are down 20% year-on-year, and the bank holds significant provisions that act as a safety buffer.

We project operating margins to remain strong at 52.5%, supported by these low credit costs and ongoing efficiency measures.

3. Exit P/E Multiple: 9.5x

Unicaja currently trades at roughly 11.4x earnings, which is a premium compared to its peers and its own history.

Our model assumes an exit multiple of 9.5x by 2027.

We chose a multiple that is lower than the current price to ensure we have a built-in margin of safety. Banks are cyclical, and paying double-digit multiples for them at the peak of the cycle often leads to poor long-term returns. As rates normalize, we expect the valuation to revert to a more standard level.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

The potential outcomes are tightly clustered, suggesting limited upside even in the best case (these are estimates, not guaranteed returns):

- Low Case: If the economy slows and NPLs rise, the stock could deliver a -6.4% annual return.

- Mid Case: If the 100% payout plan executes perfectly, but the multiple contracts, returns remain stuck at -1.8% annual return.

- High Case: Only if the market sustains a high premium multiple do we see a barely positive 1.6% annual return.

See what analysts think about UNI stock right now (Free with TIKR) >>>

How Much Upside Does Unicaja Banco Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!