Key Takeaways:

- The “Fun 101” Pivot: Target is attempting to reignite growth with “Fun 101,” a new merchandising strategy aimed at bringing “greater cultural relevance” and “trend-right energy” back to its aisles.

- Discretionary Drag: Despite growth in Food & Beverage, the core business is struggling. Comparable sales fell 2.7% in Q3, dragged down by “continued softness” in Home and Apparel.

- Price Projection: The valuation model points to a target of $128 by 2030, assuming a slow and steady stabilization of margins.

- Underwhelming Returns: With an implied 4.8% annualized return, the model suggests the stock offers little upside relative to the risks, potentially making it “dead money” for the next few years.

Target (TGT) is at a crossroads.

Once the darling of retail, the company is now fighting to stay relevant in a consumer environment that punishes “discretionary” spending.

CEO Brian Cornell remains optimistic, touting the “stores-as-hubs” model and a new partnership with OpenAI to personalize the shopping experience.

However, the results tell a different story.

While Target Circle 360 (their membership program) drove a 35% jump in same-day delivery sales, the high-margin “fun stuff”, clothes, home decor, and electronics, isn’t moving.

LTM Operating Margins have slipped to 4.7%, well below their pandemic peaks.

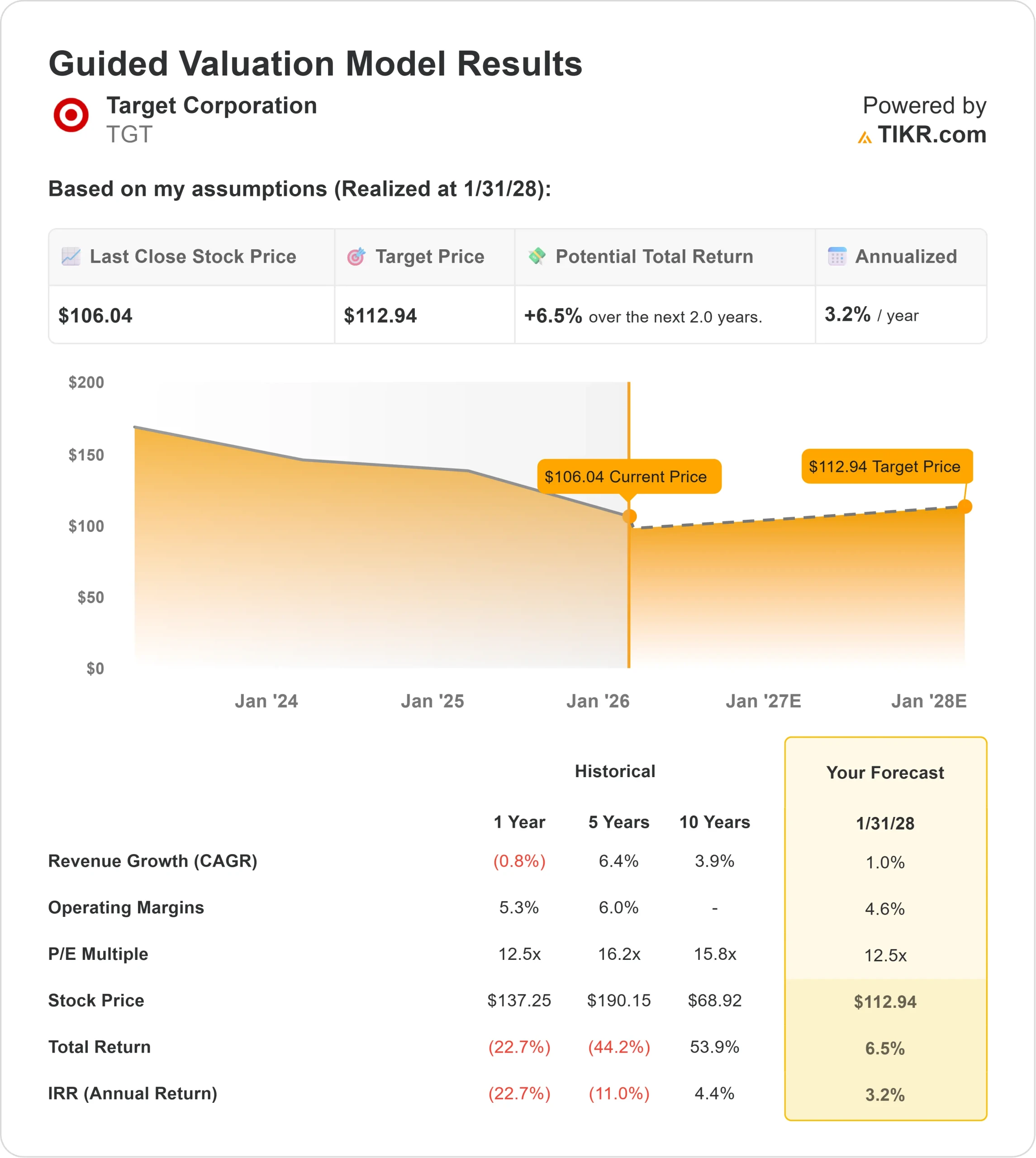

With the stock trading at $106, roughly 13x forward earnings, it looks cheap. But is it a bargain, or a classic value trap?

What the Model Says for TGT Stock

This analysis evaluates Target’s potential through 2030, balancing the reliable dividend against the lack of organic growth.

The model signals “Avoid / Value Trap.”

Using a forecast of 1.0% Revenue Growth (CAGR) and 3.3% Net Income Margins, the model points to a target price of $128 by January 2030.

This implies a disappointing 4.8% annualized return from today’s levels.

Essentially, the model suggests that unless Target can radically improve its margins or reignite sales growth, investors are simply collecting a dividend while the stock price stagnates.

Wall Street is equally skeptical.

The average street target for early 2025 has dropped to $97, which is actually below the current share price, signaling that analysts see further downside before any recovery.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for TGT stock:

1. Revenue Growth: 1.0%

While the “Drive Up” and digital segments are growing mid-single digits, they are merely offsetting the decline in physical store traffic.

Management highlighted that “consumers are choiceful, stretching budgets,” which disproportionately hurts Target’s “nice-to-have” assortment compared to Walmart’s “need-to-have” grocery dominance.

The model forecasts a meager 1.0% CAGR, reflecting a business that is struggling to expand its top line in a high-inflation world.

2. Operating Margins: 3.3% (Net)

Profitability is being squeezed from both sides.

Gross margins are under pressure from markdowns needed to clear slow-moving inventory, while SG&A expenses remain sticky.

Although management expects margin relief from lower shrink (theft) rates returning to pre-pandemic levels, the “mix shift” towards lower-margin groceries continues to be a headwind.

The model assumes Net Income Margins will average 3.3%, which is historically low for Target but realistic given the current competitive landscape.

3. Exit P/E Multiple: 12.5x

Target currently trades at a forward P/E of roughly 13.8x, which is already a discount to the broader market.

The model assumes an exit multiple of 12.5x by 2030.

This multiple reflects a mature, low-growth retailer. Without a clear catalyst for margin expansion, it is difficult to argue for a higher valuation.

What Happens If Things Go Better or Worse?

The “Base Case” offers bond-like returns with equity-like risk, a poor trade-off (these are estimates, not guaranteed returns).

- Low Case: If recession strikes and discretionary spending collapses further, the stock could fall to $115, delivering a measly 2.0% annual return (mostly from dividends).

- Mid Case: If the “Fun 101” initiatives succeed, the model points to a 21% total return over four years, hardly exciting.

- High Case: Only if Target re-attains 4% margins and 2% growth does the stock become interesting, potentially hitting $160 for a 10.8% annual return.

See what analysts forecast for the next 5 years for TGT stock (Free with TIKR) >>>

How Much Upside Does TGT Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!