Key Stats for Apollo Global Management Stock

- Past-Week Performance: -3%

- 52-Week Range: $103 to $175

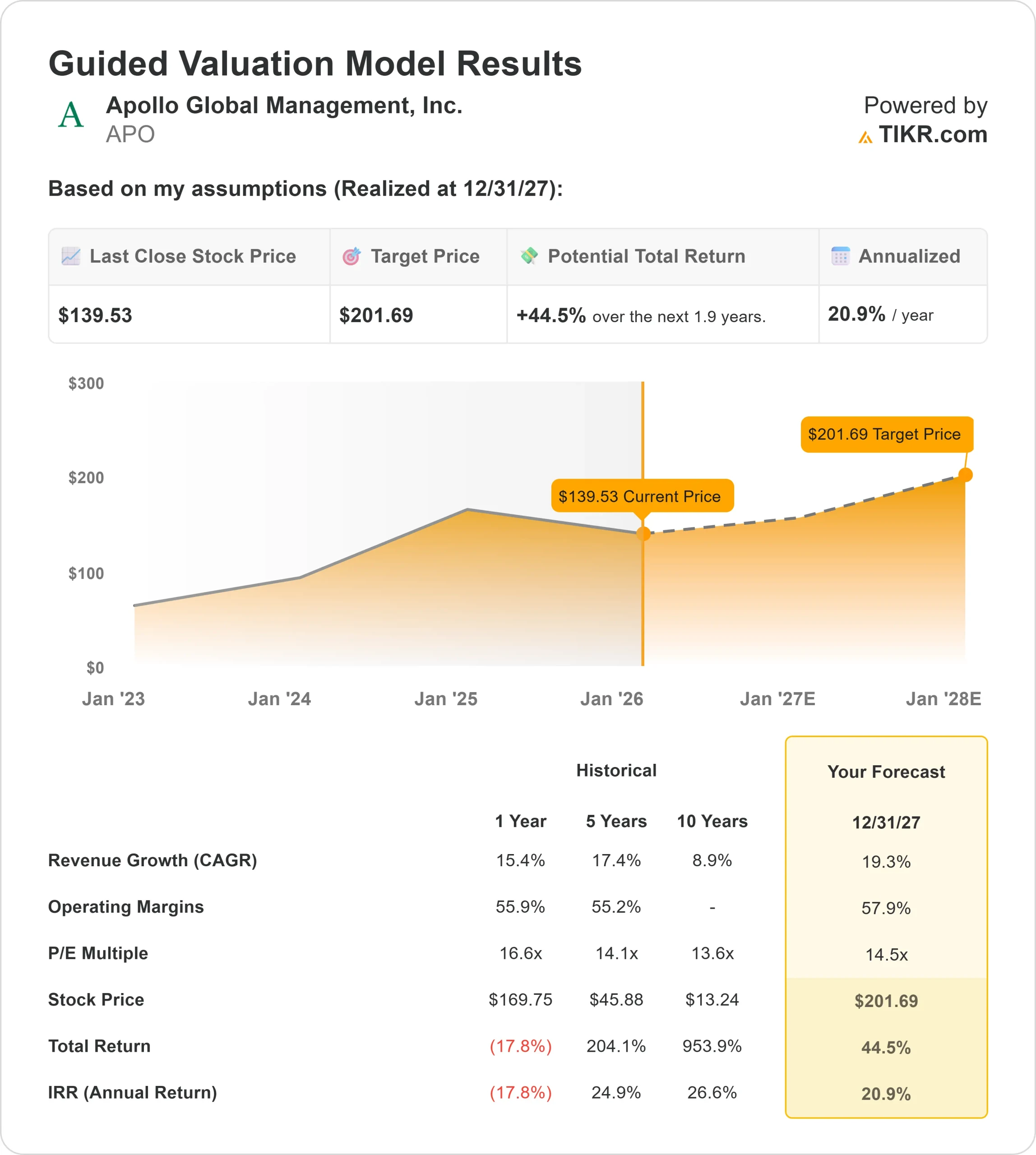

- Valuation Model Target Price: $202

- Implied Upside: 44.5% over 1.9 years

Value your favorite stocks like Apollo with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Apollo Global Management (APO) stock fell about 3% over the past week, trading lower across several sessions and finishing near $140, toward the middle of its recent trading range.

The pullback followed renewed pressure across alternative asset managers as Treasury yields moved higher, which weighed on financial stocks tied to valuation-sensitive fee income and investment returns. That rate-driven backdrop reduced risk appetite for the group during the week.

Investor positioning also played a role, with Apollo coming into the week after a strong multi-month rally that had pushed shares toward recent highs.

As rates moved up and broader financials softened, incremental profit-taking emerged, contributing to a controlled decline rather than a sharp selloff.

Analyst activity remained active, with several firms adjusting price targets to reflect updated assumptions around rates and asset valuations.

While targets moved in both directions, overall sentiment stayed constructive, helping limit downside and keep the stock well above prior support levels.

See analysts’ growth forecasts and price targets for Apollo (It’s free) >>>

Is Apollo Global Management Undervalued?

Under valuation model assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 13.4%

- Operating Margins: 48.0%

- Exit P/E Multiple: 14.0x

Based on these inputs, the model estimates a target price of $202, implying 44.5% total upside from recent levels over the next 1.9 years.

Over the next year, results are likely shaped by Apollo’s ability to deploy capital into higher-yielding private credit opportunities while maintaining discipline on underwriting as financing conditions evolve.

Growth in fee-related earnings remains closely tied to fundraising momentum across credit and hybrid strategies, which tend to deliver more stable and recurring revenue compared to traditional private equity.

Performance fees could reaccelerate if realizations pick up, particularly as older vintages move closer to exit windows in a more supportive market environment.

Expense control and scale benefits remain important, as operating leverage plays a key role in translating asset growth into earnings expansion.

Apollo Global Management appears undervalued at current levels, with future performance primarily driven by execution in credit deployment, fundraising consistency, and realization activity rather than multiple expansion alone.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>