Key Takeaways:

- The “Win Now” Reset: New CEO Elliott Hill (the “Intern to CEO”) has launched the “Win Now” strategy, aggressively “rightsizing” the Classics business to clear space for new innovation.

- China Headwinds: Management admitted the recovery in China is facing a “longer road” and requires a “fresh way of thinking” regarding their digital and monobrand footprint.

- Price Projection: The valuation model points to a target of $93 by 2030, assuming the turnaround eventually gains traction.

- Muted Returns: Despite the upside potential, the model implies a modest 8.3% annualized return, signaling that the stock may be “dead money” until growth re-accelerates.

Nike (NKE) is attempting one of the most high-profile turnarounds in retail history.

After losing ground to upstarts like On and Hoka, the company has brought back company veteran Elliott Hill to right the ship.

His “Win Now” plan is already in motion.

In the latest quarter, Nike aggressively cut back on its “Classics” franchises (like Air Force 1) to fix the marketplace and make room for new launches like the Structure 26 and the Nike Mind wellness platform.

North America is showing early signs of life, with meaningful growth returning through wholesale partners.

However, the numbers are still ugly.

LTM Revenue has dipped to $46.5 billion, and the company is battling “transitory headwinds” to margins as it liquidates old inventory.

With the stock trading at $65, investors are asking: Is this the bottom, or a value trap?

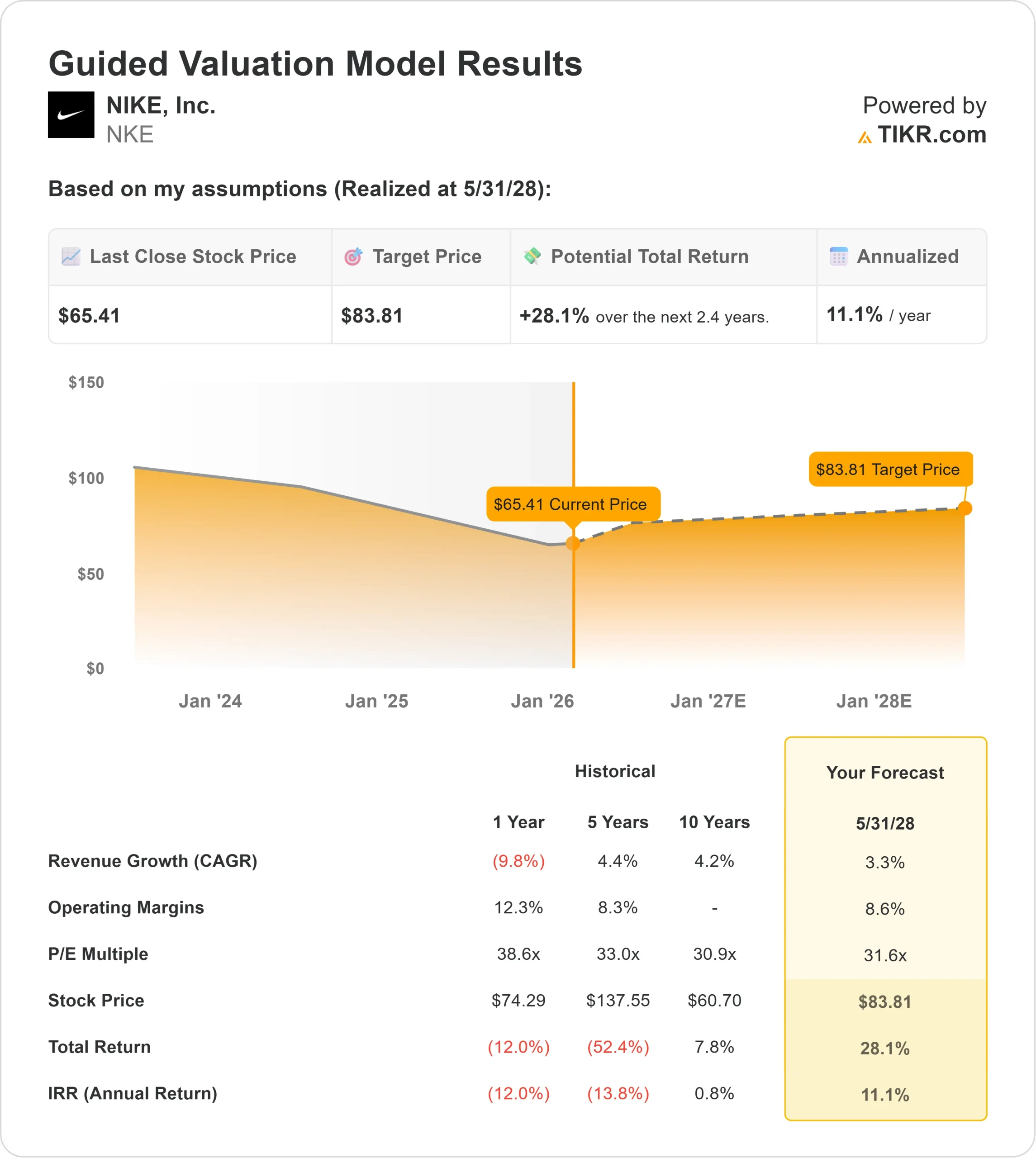

What the Model Says for NKE Stock

This analysis evaluates Nike’s potential through 2030, weighing the brand’s immense power against its current growth struggles.

The model signals a “Hold.”

Using a forecast of 3.3% Revenue Growth (CAGR) and 6.7% Net Income Margins, the model points to a target price of $93 by May 2030.

This implies an 8.3% annualized return from today’s levels.

While positive, this return barely beats the market’s historical average, suggesting investors are not being paid enough of a “risk premium” to wait for the turnaround.

Wall Street is slightly more optimistic in the short term.

The average street target is roughly $77 for January 2027, implying a 17% upside over the next 12 months as analysts bet on a quicker recovery.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for NKE stock:

1. Revenue Growth: 3.3%

The days of double-digit growth appear to be over for now.

While North America is stabilizing, China remains a drag.

Management explicitly stated that “it’s not happening at the level or the pace we need” in China, forcing a strategic reset.

The model forecasts a modest 3.3% CAGR, assuming the new “Air” innovations can offset the decline in legacy franchises.

2. Operating Margins: 6.7% (Net)

Profitability is under pressure.

The “Win Now” actions involve heavy investments in marketing (up significantly to reignite the brand) and “structural headwinds” from tariffs and product costs.

While Gross Margins remain healthy at 41.1%, the bottom line is being squeezed by the cost of the turnaround.

The model assumes Net Income Margins will average 6.7%, reflecting a business that is spending heavily to regain market share.

3. Exit P/E Multiple: 31.6x

Nike currently trades at a forward P/E of roughly 34.5x, a premium that reflects its “blue chip” status rather than its current growth rate.

The model assumes an exit multiple of 31.6x by 2030.

This multiple assumes the market will continue to treat Nike as a premium consumer staple, even with slower growth. If the market re-rates Nike like a standard apparel stock (closer to 20-25x), the downside could be significant.

What Happens If Things Go Better or Worse?

The “Base Case” offers market-matching returns, but the variance is high depending on the success of the new product pipeline (these are estimates, not guaranteed returns).

- Low Case: If the brand fails to resonate with Gen Z, the model points to a $93 target (Base Case) or potentially lower, risking steady but unexciting returns.

- Mid Case: If the “Win Now” strategy stabilizes the ship, the model points to a 42% total return by 2030.

- High Case: If Nike re-ignites double-digit growth, the stock could run to $136, delivering a strong 18.3% annual return.

See what analysts forecast for the next 5 years for NKE stock (Free with TIKR) >>>

How Much Upside Does NKE Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!