Key Stats for Mastercard Stock

- 52-Week Range: $465 to $602

- Current Price: $472

- Street Mean Target: $647

- Street High Target: $735

- Analyst Consensus: 29 Buy, 7 Outperform, 3 Hold

- TIKR Model Target (Dec. 2030): $856

Mastercard Stock Beats Q1 Estimates, Then Falls Anyway — Here Is What the Market Is Pricing Wrong

Mastercard Incorporated (MA), the global payments network that processes transactions across more than 150 currencies without holding any credit risk, reported Q1 2026 adjusted EPS of $4.60, beating the $4.40 analyst consensus, as net revenue of $8.4 billion rose 12% year over year on a currency-neutral basis.

The reaction was a 3% decline on the day of the print.

What the market sold was cross-border travel.

CFO Sachin Mehra said on the Q1 call that starting in March, Mastercard began seeing the impact of the Middle East conflict on cross-border travel, with cross-border volume growth slowing to 13% compared with 15% a year ago.

The geographic exposure is real but bounded: Mehra noted that the GCC and Israel together represent roughly 6% of Mastercard’s global cross-border volumes, both inbound and outbound.

Value-added services and solutions, the segment covering security, tokenization, AI-powered analytics, and dispute resolution, grew 18% on an organic currency-neutral basis in Q1 — with no acquisition contribution in the figure.

CEO Michael Miebach said on the May 28 Bernstein conference that consumer spending growth had continued into the first two weeks of May, describing trends as “stable to slightly better” across Mastercard’s network metrics.

Mastercard repurchased $4 billion of its own stock in Q1 and an additional $1.7 billion through April 27, with Mehra explicitly citing the current price as the reason for accelerating the pace of buybacks.

The company maintained its full-year outlook for adjusted net revenue growth at the high end of the low-double-digit to low-teens range on a currency-neutral basis, unchanged from guidance issued at the start of the year.

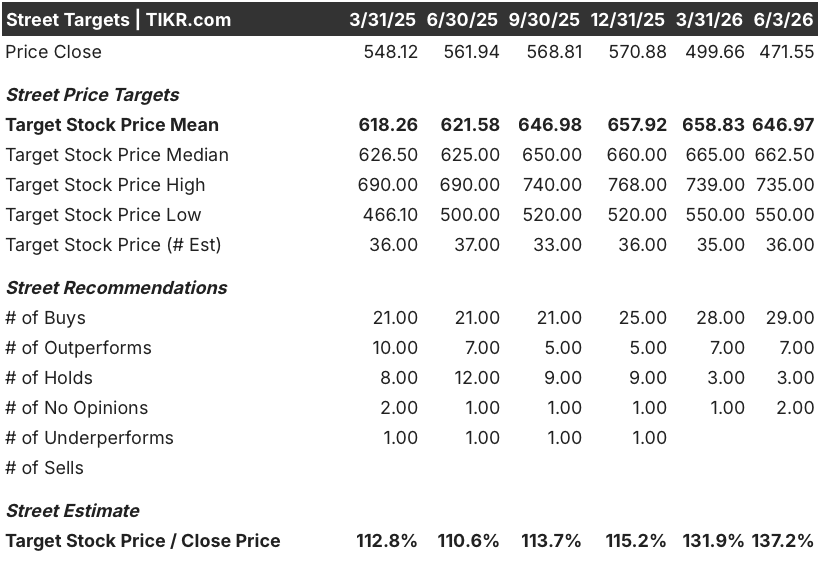

Why 36 Analysts Still Have Buy Ratings on MA Stock Despite the Selloff

The selloff in Mastercard stock has not moved Wall Street’s conviction.

Thirty-six of 39 analysts covering MA carry buy-equivalent ratings, with a mean price target of around $647, implying roughly 37% upside from the current price.

The earnings trajectory supporting that conviction is consistent: EPS Normalized came in at $4.60 in Q1 2026, up 23.3% year over year from $3.73 in Q1 2025, and consensus projects EPS of around $5 for Q2 2026, representing roughly 15% growth over the prior year period.

Looking further out, consensus calls for EPS of approximately $5 for Q3 and $5 for Q4 2026, building to an estimated $21 for the full year, and analysts project continued double-digit EPS growth into 2027.

The J.P. Morgan team, carrying an overweight rating with a $655 target, acknowledged that the Middle East conflict is expected to weigh on Q2 growth but described the impact as manageable, citing limited exposure and clear disclosure.

TD Cowen, with a buy and a $671 target, said clearer messaging around stablecoins and agentic commerce, combined with faster adoption, should reduce uncertainty and support continued growth.

The strategic story has expanded since Q1: Mastercard’s planned acquisition of BVNK, a stablecoin infrastructure platform with send, receive, store, and convert capabilities across digital asset rails, adds a revenue stream in a market the company currently does not participate in at scale.

In May, Mastercard also won a New York State Department of Financial Services BitLicense for its U.S. transaction services unit, clearing a regulatory prerequisite for regulated digital currency settlement services.

At the current price, a business generating 18% organic VAS growth, beating every Q1 estimate, holding full-year guidance, and deploying capital at this rate of buyback is priced as though the Middle East headwind is permanent — Mastercard stock is undervalued at these levels.

MA Stock Is Growing EPS Faster Than Visa and American Express — and Trades Below Both on a Price Basis

Mastercard stock carries the highest EPS among its two closest peers: MA printed $4.60 in Q1 2026, ahead of American Express (AXP) at $3.99 and Visa (V) at $3.10 in the same quarter.

The gap widens on forward estimates, with consensus projecting MA EPS of around $5 for Q2 2026, compared with around $4 for AXP and around $3 for V, a spread that reflects Mastercard’s faster network growth, its higher mix of VAS revenue, and the compounding effect of an accelerated buyback program reducing the share count more aggressively than peers.

Looking into 2027, the EPS trajectory for MA is expected to reach approximately $6 on a quarterly basis, versus approximately $5 for AXP and approximately $4 for V, suggesting the earnings lead is not compressing but widening — and at $472, Mastercard stock is priced as though that trajectory carries more risk than the peer comparison data supports.

Is Mastercard Stock Undervalued in 2026? What the TIKR Model Shows for MA

TIKR’s base case values Mastercard stock at approximately $856 by December 2030, implying around 82% total return from the current price of $472, or roughly 14% annualized over approximately 4.6 years.

The mid-case assumes revenue growing at around a 9% CAGR, net income margins of approximately 47%, and EPS growing at around 11% annually — a moderate deceleration from Mastercard’s five-year historical EPS CAGR of roughly 22%; the non-trivial tension is whether the P/E multiple, which the model assumes contracts at around 3% annually, compresses faster than the earnings growth rate can offset, particularly if stablecoin competition or regulatory scrutiny widens from the UK and EU proceedings currently underway.

If revenue growth holds near 10% and margins sustain above 49%, the high case produces a stock price of approximately $1,436 by December 2030, representing a total return of around 205% and an IRR of roughly 14%. If growth disappoints at around 8.5% revenue CAGR and margins settle near 44%, the low case delivers approximately $872, still roughly 85% above today’s price with an IRR of around 7%.

What happened to Mastercard stock in 2026?

Mastercard stock declined roughly 22% from its 52-week high of $602 to a current price of $472, primarily driven by investor concern over the Middle East conflict’s impact on cross-border travel volumes.

The underlying business beat Q1 estimates and held full-year guidance.

Is Mastercard stock a buy in 2026?

Thirty-six of 39 covering analysts carry buy-equivalent ratings on MA stock, with a mean target of around $647 and a high target of $735.

TIKR’s base-case valuation model implies approximately $856 by December 2030, suggesting meaningful upside from current levels.

What is driving Mastercard’s value-added services growth?

Mastercard’s value-added services segment, which is now approximately 40% of total net revenue, grew 18% organically in Q1 2026. Key drivers include security solutions (the largest VAS category), tokenization, AI-powered fraud and analytics tools, and dispute resolution products including Ethoca.

Roughly 60% of VAS revenues are network-linked, meaning they grow structurally as transaction volumes rise.

What is BVNK and why did Mastercard acquire it?

BVNK is a stablecoin infrastructure platform with capabilities to send, receive, store, and convert digital assets across multiple chains and denominations. Mastercard announced the planned acquisition to capture fee revenue from the growing B2B, remittance, and me-to-me digital asset payment market — a segment the company currently accesses only through third-party partners.

Should You Invest in Mastercard Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Mastercard Incorporated stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Mastercard Incorporated alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MA stock on TIKR for Free →