Key Stats for Adobe Stock

- 52-Week Range: $224 to $421

- Current Price: $256

- Street Mean Target: $327

- Street High Target: $487

- Analyst Consensus: 12 Buy, 3 Outperform, 20 Hold, 4 Sell

- TIKR Model Target (Nov. 2030): $501

Adobe Stock Bounces 8% on Software Rotation as Q2 Earnings Loom

Adobe (ADBE), the maker of Photoshop, Acrobat, and the Firefly generative AI suite, rallied roughly 8% in early June 2026 as retail and institutional investors rotated back into beaten-down software following Nvidia CEO Jensen Huang’s comments that AI agents will drive more software demand, not less.

The iShares Expanded Tech-Software Sector ETF surged nearly 42% from its April low, and Adobe stock was among the names swept up in the move, with shares jumping between 6% and 8% as part of a broader software recovery that included ServiceNow, Salesforce, and Workday.

Adobe stock had been one of the more visible casualties of the AI disruption narrative, falling around 30% year-to-date before the bounce, driven in part by fears that tools like Anthropic’s Claude Design would undercut demand for the company’s creative software.

The timing matters: Adobe is set to report Q2 fiscal 2026 results on June 11, and the company guided for revenue of $6.43 billion to $6.48 billion and non-GAAP EPS of $5.80 to $5.85.

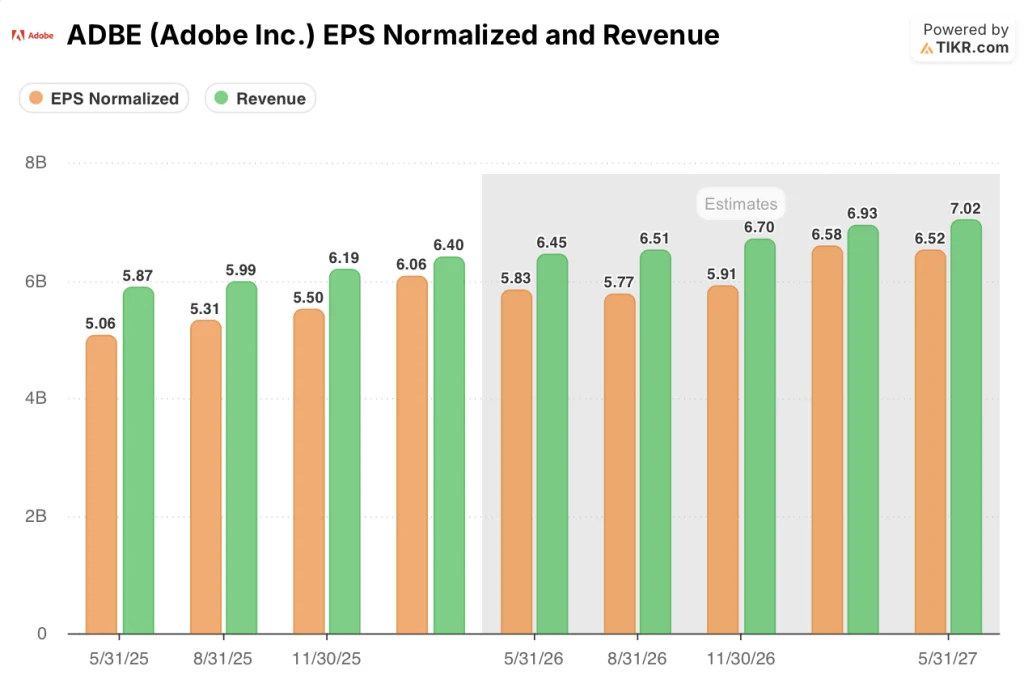

The selloff came despite Adobe delivering a strong Q1, with revenue of $6.40 billion growing 12% year-over-year, non-GAAP EPS of $6.06 growing 19%, and operating cash flow of $2.96 billion, a Q1 record.

“We’ve got great innovation in flight,” CFO Dan Durn said on the Q1 earnings call, outlining the company’s capital allocation framework. “We’ve got an organic engine that we’re pleased with the innovation we’re bringing and the strategy that we’re executing against.”

Adobe also completed its acquisition of Semrush during the quarter, adding a brand visibility and SEO platform that positions the company in the emerging generative engine optimization space, where enterprise clients increasingly need to manage how their brands appear across AI-driven discovery channels.

The company surpassed 850 million monthly active users across Acrobat, Creative Cloud, Express, and Firefly in Q1, growing 17% year-over-year, a data point the company is using as its leading indicator for future ARR conversion.

Firefly, Adobe’s generative AI studio, grew its ending ARR to over $250 million with subscription and credit pack ARR up 75% quarter-over-quarter, while generative credit consumption rose more than 45% quarter-over-quarter.

One honest wrinkle: the traditional stock photo business saw a steeper-than-expected decline in Q1, which management acknowledged was happening faster than planned; on a like-for-like basis, however, that drag reduced total ARR growth by only around 30 basis points.

Analysts Cut Adobe Stock Targets but Hold Their Conviction on ADBE’s EPS Trajectory

Wall Street’s relationship with Adobe stock has been openly uncomfortable in 2026.

The street mean target has compressed from $565 at the start of 2025 to around $327 today, a 42% collapse in analyst price targets against a backdrop where the underlying business kept delivering double-digit growth.

Twelve analysts maintain a Buy or equivalent rating, three rate it Outperform, twenty hold it at Neutral, and four recommend selling it; the distribution reflects genuine disagreement about how much the AI disruption narrative is structural versus cyclical.

The sharpest negative catalyst came in late April, when Mizuho cut its rating to Neutral and trimmed its price target to around $270, flagging competitive pressure from Canva in the prosumer and SMB segments and noting that Adobe’s AI-first annual recurring revenue represented less than 2% of its roughly $26 billion total ARR base.

The EPS picture is what keeps bulls engaged: Adobe delivered non-GAAP EPS of $6.06 in Q1, up 19.3% year-over-year, and consensus now expects around $5.83 in Q2, up around 15% year-over-year, with full-year estimates continuing to show mid-teens growth.

Street consensus projects EPS normalized of around $5.83 for Q2 fiscal 2026, $5.77 for Q3, and $5.91 for Q4, with the next fiscal year estimate reaching around $6.58 in Q1 of fiscal 2027.

The revenue trajectory is similarly constructive: consensus estimates around $6.45 billion for Q2 and around $6.51 billion for Q3, implying roughly 10% year-over-year growth each quarter, consistent with the company’s reaffirmed full-year ARR growth target of 10.2%.

At $256 with the street mean at $327, the implied upside from consensus alone is around 28%. Given that EPS is growing 19% while the stock has repriced to its lowest levels since before the pandemic recovery period, ADBE is undervalued relative to where its earnings trajectory sits today.

If Firefly and the AI-first product suite never convert their 850 million MAU into meaningful ARR, the discount is permanent, not temporary.

ADBE Revenue Growth Trails Oracle and Salesforce, and the Gap Is Widening

Adobe’s revenue grew 9.90% year-over-year in the most recent quarter, while Oracle (ORCL) posted 20.08% growth in the same period and consensus estimates project Oracle accelerating to around 27% by the next quarter.

Salesforce (CRM) is running closer to Adobe at around 9.90% revenue growth currently, but the two companies are diverging on the forward trajectory, with Salesforce consensus holding near 9% through fiscal 2027 while Oracle’s estimates climb toward around 37%.

The competitive read for Adobe stock is uncomfortable but not fatal: Adobe is not losing ground to Salesforce on revenue growth, but Oracle’s AI infrastructure tailwind is pulling capital toward a faster-growth narrative in the same enterprise software spending cycle that Adobe is trying to win.

Is Adobe Stock Undervalued in 2026? TIKR’s $501 Model Says the Selloff Went Too Far

TIKR’s base case values Adobe at approximately $501 by November 2030, implying around a 96% total return from the current price of around $256, or roughly 16% annualized over approximately 4.5 years.

The TIKR model is built on mid-case assumptions of around 11% revenue CAGR from 2025 through 2035, a net income margin around 36%, and EPS CAGR around 15%, with a P/E multiple contracting around 3% annually from current levels.

Given that Adobe has already delivered a 10-year revenue CAGR of 17.4% and a 10-year EPS CAGR of 26%, the mid-case is a material step down from history.

The market has already priced in deceleration; what it has not priced in is that the deceleration still produces double-digit compounding. At around $256 versus a mid-case target of around $501, ADBE looks mispriced for a business this durable.

If Adobe sustains closer to the high-case trajectory, the TIKR model produces a stock price around $1,144 by November 2034 with an IRR around 19%. If growth disappoints at the low end, the model still generates a stock price around $642 with an IRR around 11% — still well above the current price.

The scenario that justifies the current price essentially requires growth to fall below even the low case, which would mean a company losing competitive ground across three separate billion-dollar product lines simultaneously.

What is Adobe stock’s price target?

The street mean target is around $327, implying roughly 28% upside from the current price of around $256. The street high target is around $487.

TIKR’s mid-case valuation model targets around $501 by November 2030, implying around 96% total return.

Is Adobe stock a buy right now?

Twelve analysts rate Adobe stock a Buy and three rate it Outperform out of 39 analysts currently covering the stock.

The bull case rests on 19% non-GAAP EPS growth in Q1, a $26 billion ARR base, and a $25 billion buyback authorization.

The bear case centers on AI competition from tools like Anthropic’s Claude Design and Canva in the SMB segment.

Why did Adobe stock drop in 2026?

Adobe stock fell roughly 30% in the first months of 2026 as investors repriced software sector risk following Anthropic’s launch of Claude Design in April, which automates design creation and was seen as a direct competitive threat. The stock also absorbed pressure from sector-wide AI disruption fears following weak results from IBM and ServiceNow.

Should You Invest in Adobe Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Adobe Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Adobe Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ADBE stock on TIKR for Free →