Key Stats for WESCO Stock

- Past-Week Performance: +4.8%

- 52-Week Range: $125.2 to $319.7

- Current Price: $262.1

What Happened?

WESCO International (WCC), a business-to-business distributor of electrical, communications, and utility products, posted record full-year data center sales of $4.3 billion in FY 2025, up 50% year over year, confirming that AI infrastructure buildout has structurally reset the company’s revenue profile, with shares trading at $262.13.

On February 10, WESCO reported Q4 net sales of $6.07 billion, beating the IBES estimate of $6.03 billion, while adjusted EPS of $3.40 missed the $3.88 consensus, dragged by public power margin pressure and a one-time $10 million interest expense adjustment that hit the quarter unexpectedly.

The sharpest forward signal came from the company’s record total backlog, up 19% year over year, with the Communications and Security Solutions segment, which houses WESCO’s data center business, reporting a backlog up nearly 40% to a record level, while January 2026 sales per workday rose 15% with growth composition matching Q4 across all three business units.

John Engel, Chairman, President and CEO, stated on the Q4 2025 earnings call that “we’re not anywhere near, not even remotely close to seeing a peak in the cycle for AI-driven data centers,” tying directly to management’s guidance for mid-teens data center sales growth in 2026 and the company’s Fortune 500 top-10 AI ranking.

WESCO’s 2026 guidance for $14.50 to $16.50 in adjusted EPS, $500 million to $800 million in free cash flow, and a $1.5 billion debt refinancing completed February 27 at materially lower rates positions the company to convert data center momentum into shareholder returns, supported by a 10%-plus dividend increase to $2.00 per share and a long-term EBITDA margin target above 10% by 2030.

Wall Street’s Take on WCC Stock

The record $4.3 billion in FY 2025 data center sales, up 50% year over year, represents a structural shift in WESCO’s earnings mix that analysts believe will drive normalized EPS 21.2% higher to $15.65 in FY 2026, as TIKR estimates.

TIKR estimates EBITDA expanding from $1.54 billion in FY 2025 to $1.72 billion in FY 2026, a gain of 11.8%, supported by the CSS segment’s 40% backlog growth and mid-teens data center revenue guidance that management anchored to January’s 15% sales-per-workday increase.

The FCF inflection is the most underappreciated element of the story: TIKR estimates free cash flow surging from $54 million in FY 2025 to $670 million in FY 2026, a recovery driven by working capital normalization as inventory and receivables growth decelerates to roughly half the rate of sales.

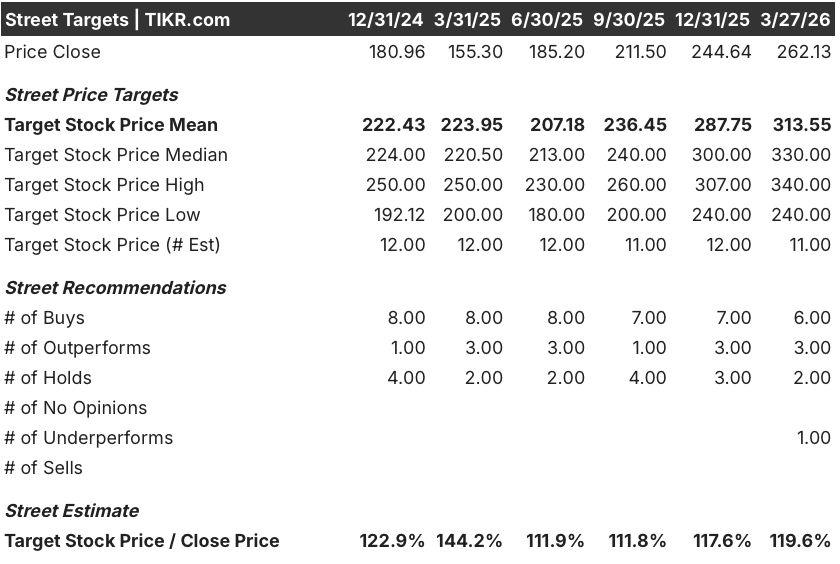

Wall Street currently sits at 6 buys, 3 outperforms, 2 holds, and 1 underperform, with a mean price target of $313.55, implying 19.6% upside from the March 27 close of $262.13, a consensus that reflects confidence in data center durability but embeds limited credit for UBS recovery.

The spread between the $240.00 low target and $340.00 high target reflects one binary question: how fast public power customers, who face transformer inventory overhangs and competitive pricing pressure, return to growth, which management guided will not occur until late 2026.

What Does the Valuation Model Say?

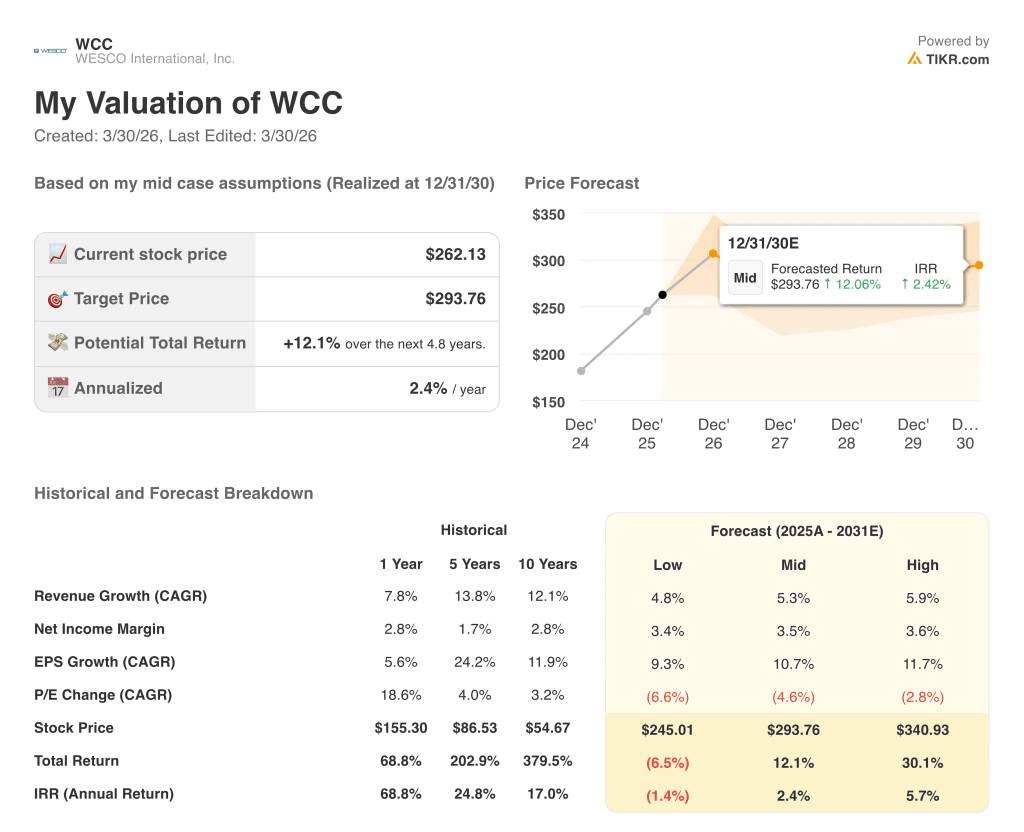

TIKR’s mid-case price target of $293.76 assumes a 5.3% revenue CAGR and 10.7% EPS CAGR through 2030, inputs directly supported by the CSS segment’s record backlog and management’s double-digit grid services growth outlook for FY 2026.

The market is pricing WCC at 18x forward earnings despite a 21% EPS growth rate in FY 2026, a compression that ignores the $670 million free cash flow recovery TIKR estimates for the same year.

The 19% total backlog growth and January’s 15% sales-per-workday gain confirm that WESCO’s earnings acceleration is already in motion, not a projection, making the current multiple look historically narrow.

The one development that breaks the model is a stall in data center capital spending, which management acknowledged drives roughly 18% of total sales and whose mid-teens growth assumption underpins the entire EBITDA margin expansion path from 6.5% to 6.8%.

Q2 earnings on April 30 will be the first read on whether UBS margins are stabilizing and whether the $670 million FCF target is tracking; watch the gross margin line within UBS, the single number that cracked the Q4 beat.

Should You Invest in WESCO International, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WCC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track WESCO International, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WCC stock on TIKR for Free →