Key Takeaways:

- CEO Transition: Vulcan Materials completed a leadership transition in January 2026, with Ronnie Pruitt assuming the CEO role after Tom Hill’s decade-long tenure, inheriting a business with trailing 12-month free cash flow exceeding $1 billion and aggregate cash gross profit per ton up 27% over 2 years.

- Dividend Raised: Vulcan Materials raised its quarterly dividend to $0.52 per share last February, a 6% increase from $0.49, marking 9 consecutive years of dividend growth and reflecting management’s confidence in sustained cash generation ahead of Q4 2025 earnings on February 17.

- Price Projection: Vulcan Materials stock could reach $370 by December 2027, grounded in 6% revenue growth toward $8 billion, operating margins expanding to 23%, and a 32x earnings multiple consistent with the stock’s 10-year historical P/E range.

- Total Upside: Vulcan Materials’ $370 target represents a total return of 13% from the current price of $328, translating to an annualized return of 7% per year over 1.9 years.

Breaking Down the Case for Vulcan Materials Co.

Vulcan Materials Company (VMC), the largest construction aggregates producer in the United States, faces a pivotal Q4 2025 earnings test on February 17 with analyst expectations of $2.13 EPS on $2 billion in revenue.

Last January, DA Davidson downgraded the stock to Neutral at $306, citing narrowing price realization potential and moderation in infrastructure bid activity as the primary near-term risk factors.

B. Riley (RILY) countered last January with a Buy initiation and a $345 price target, describing the business as a toll road on US construction with natural local monopolies across its 80-country footprint serving 200 million square feet of data center projects.

Full-year 2025 revenue is estimated at $8 billion, with EBITDA expanding 17% to $2 billion and operating margins improving from 19% in 2024 toward 21%, supported by the Vulcan Way of Operating across 127 technology-equipped plants.

COO-turned-CEO Ronnie Pruitt stated at the Q3 call: “Our trailing 12 months aggregate cash gross profit per ton was $11.51, 27% higher than just 2 years ago.”

The company disposed of its asphalt and construction services assets in October 2025 and announced the divestiture of its California concrete business, redeploying capital toward aggregate-centric acquisitions with leverage maintained just below the 2 to 2.5x EBITDA target range.

Only 40% of IIJA infrastructure funds have been spent, trailing 12-month highway starts are up 17% in Vulcan-served states, and the company’s M&A pipeline remains active under a new CEO with $1 billion in annual free cash flow at his disposal.

At a forward P/E of 39x against a consensus Buy and a mean target of $329, the stock trades near its 52-week high of $331, leaving investors to determine whether the Q4 earnings report and 2026 guidance can justify that premium before the surface transportation authorization expires in September.

What the Model Says for VMC Stock

Vulcan’s infrastructure tailwinds are real, but with the stock at $328 already trading above the analyst consensus target of $320, the market has priced the near-term construction cycle before Q4 2025 earnings even land on February 17 (which is expected to be released today).

The model’s assumption of 6.3% revenue growth and 22.5% operating margins, conservative relative to the current forward earnings multiple of 34.9x the market prices today, supports a 32.3x exit multiple and produces a target price of $370.

At a total return of 13% from the current price of $328, the annualized return of 6.7% falls well short of the standard 10% equity hurdle rate, and with the consensus target at $320, near-term downside of 2% compounds that shortfall further.

The model signals a Hold. Vulcan’s 6.7% annualized return does not clear the 10% hurdle, meaning the stock’s current price already absorbs much of the infrastructure cycle upside the model’s assumptions are built on.

Vulcan’s 6.7% annualized return falls well below the 10% equity hurdle rate, offering insufficient risk compensation at current prices. At a 32.3x exit multiple, this represents modest capital appreciation, justified only if the 22.5% operating margin assumption holds through 2027.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Vulcan Materials stock:

1. Revenue Growth: 6.3%

Vulcan posted a 4.7% revenue decline in 2024 to $7 billion, as weather disruptions suppressed shipment volumes, but the 5-year historical CAGR of 8.5% shows the underlying growth rate when demand conditions cooperate.

The 2025 revenue estimate of $8 billion represents 7.8% growth, as Q3 shipments recovered 12% on improved weather and strong public demand, directly supporting the model’s 6.3% assumption as a slight moderation from the current recovery pace.

Only 40% of IIJA infrastructure funds have been spent, trailing 12-month highway starts are up 17% in Vulcan states, and 200 million square feet of data center projects sit within the company’s footprint, all of which sustain the demand base the 6.3% assumption requires.

The September 2026 expiration of the current surface transportation authorization introduces a real funding gap risk, and any delay in reauthorization directly removes the public construction volume the 6.3% growth assumption depends on to offset ongoing single-family residential weakness.

This sits above the 1-year historical revenue growth of -4.7%, as the Q3 2025 shipment recovery and unspent IIJA funds provide a credible demand floor, and any reauthorization delay or single-family drag would pull growth back toward the 4.6% 2026 consensus estimate.

2. Operating Margins: 22.5%

Vulcan stock’s past 12 moths’ operating margin stands at 20.4%, up from 19.1% in 2024, as the Vulcan Way of Operating reduced aggregate unit cash costs 2% in Q3 2025 and aggregate cash gross profit per ton reached $11.51, 27% above levels from 2 years prior.

The 2026 consensus estimate puts EBIT margins at 22.4%, nearly identical to the model’s 22.5% assumption, making this the most externally validated input in the entire model with strong near-term execution data supporting it.

Reaching 22.5% requires the Vulcan Way of Operating to continue delivering cost discipline across 127 technology-equipped plants, while mid-single-digit pricing holds in a market where DA Davidson last January flagged narrowing price realization potential as a primary downgrade catalyst.

The asphalt and concrete divestitures completed last October remove lower-margin downstream revenue from the consolidated base, structurally improving blended margins and providing direct support for the 22.5% operating margin assumption without requiring unusual cost outperformance.

If pricing gains decelerate toward the low end of mid-single-digit guidance and volume growth disappoints, margin expansion stalls at current levels near 20%, and the 32.3x exit multiple then prices a business delivering margins no better than it does today.

This sits above the 1-year historical operating margin of 18.3%, as the portfolio reset and Vulcan Way of Operating cost disciplines have structurally shifted the margin profile upward, and sustaining 22.5% requires both pricing momentum and continued technology-driven cost improvement through 2027.

3. Exit P/E Multiple: 32.3x

A terminal P/E multiple converts Vulcan’s projected 2027 earnings into a stock price, and at 32.3x, it reflects what the market would pay for a dominant aggregates franchise with natural local monopolies at the end of the forecast period.

Vulcan’s current forward P/E as of last February sits at 34.9x on normalized earnings, meaning the model’s 32.3x exit multiple is a modest discount to today’s market pricing, making the multiple assumption conservative relative to where the stock currently trades.

The 10-year historical P/E of 29.2x sits below the 32.3x exit assumption, meaning the model prices Vulcan at a premium to its long-run average, justified only if margin expansion to 22.5% and sustained infrastructure demand hold through the exit year.

The 32.3x exit multiple already captures the benefit of margin expansion and revenue growth through the income statement, and awarding a premium multiple on top of those gains would double-count the same improvement the model already prices through earnings.

If Q4 2025 earnings disappoint on February 17 and 2026 guidance comes in below consensus, the market-assigned multiple contracts from its current 34.9x toward the 10-year average of 29.2x, and the resulting stock price falls well below the $370 target.

This sits above the 1-year historical P/E of 31x, as the model conservatively discounts the stock below where the market assumption of 34.9x for the next twelve months, and any Q4 2025 earnings disappointment or 2026 guidance miss on February 17 compresses the multiple back toward that lower exit level, pulling the $370 target price down with it.

What Happens If Things Go Better or Worse?

Vulcan Materials stock’s range through 2029 is set by 3 real variables: the pace of IIJA infrastructure spending conversion, Vulcan Way of Operating cost discipline under new CEO Ronnie Pruitt, and whether the September 2026 surface transportation reauthorization sustains public construction demand.

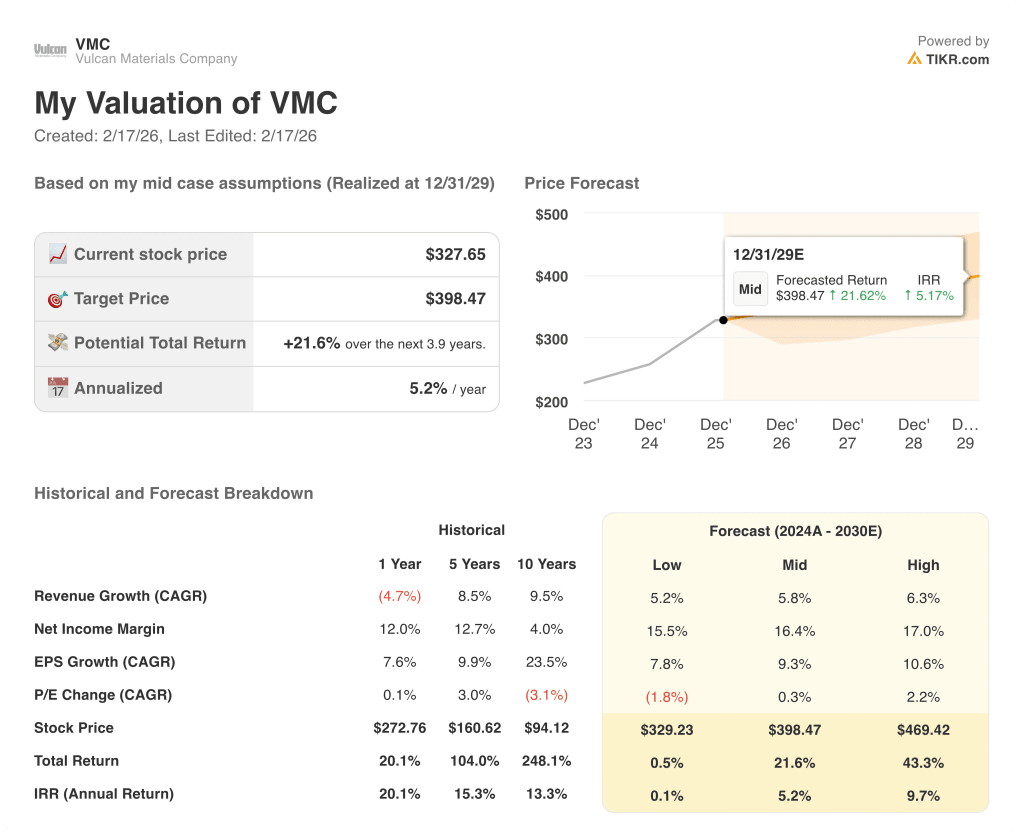

- Low Case: If surface transportation reauthorization stalls and single-family residential weakness persists longer than expected, revenue grows around 5.2% and net income margins stay near 15.5% → 0.1% annualized return

- Mid Case: With IIJA funds continuing to convert into shipments, data center demand sustaining aggregate volumes, and Vulcan Way of Operating cost disciplines holding, revenue grows near 5.8% and margins improve toward 16.4% → 5.2% annualized return

- High Case: If private non-residential construction accelerates beyond current backlog trends, new CEO Pruitt executes aggregate-centric M&A, and reauthorization passes smoothly, revenue reaches 6.3% and margins approach 17% → 9.7% annualized return

How Much Upside Does Vulcan Materials Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!