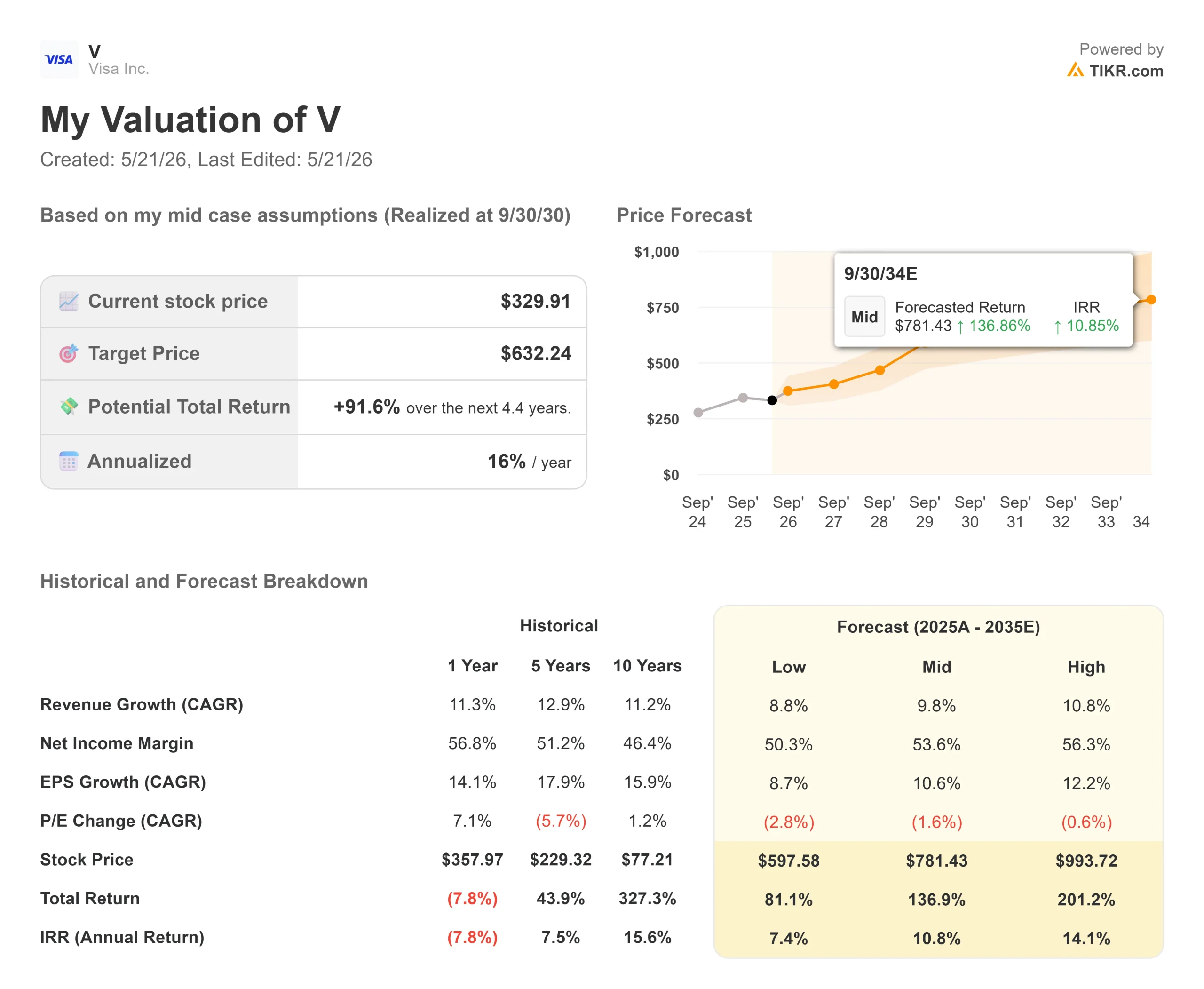

Key Stats for Visa Inc. Stock

- Current Price: $329.91

- Target Price (Mid): ~$632

- Street Target: ~$399

- Potential Total Return: ~92%

- Annualized IRR: ~16% / year

- Earnings Reaction: +8.26% (April 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Visa Inc. (V) jumped 8.26% on April 28 after reporting its strongest revenue quarter since 2022. Three weeks later, at the J.P. Morgan 54th Annual Global Technology, Media and Communications Conference on May 19, CFO Christopher Suh went beyond the earnings call, laying out the mechanics of Visa’s next phase in more detail than most investors have seen. The stock sat at $329.91 at the May 19 close, still about 12% below its 52-week high of $375.51. That gap is what this article is about.

“The Best Quarter in Over a Decade”

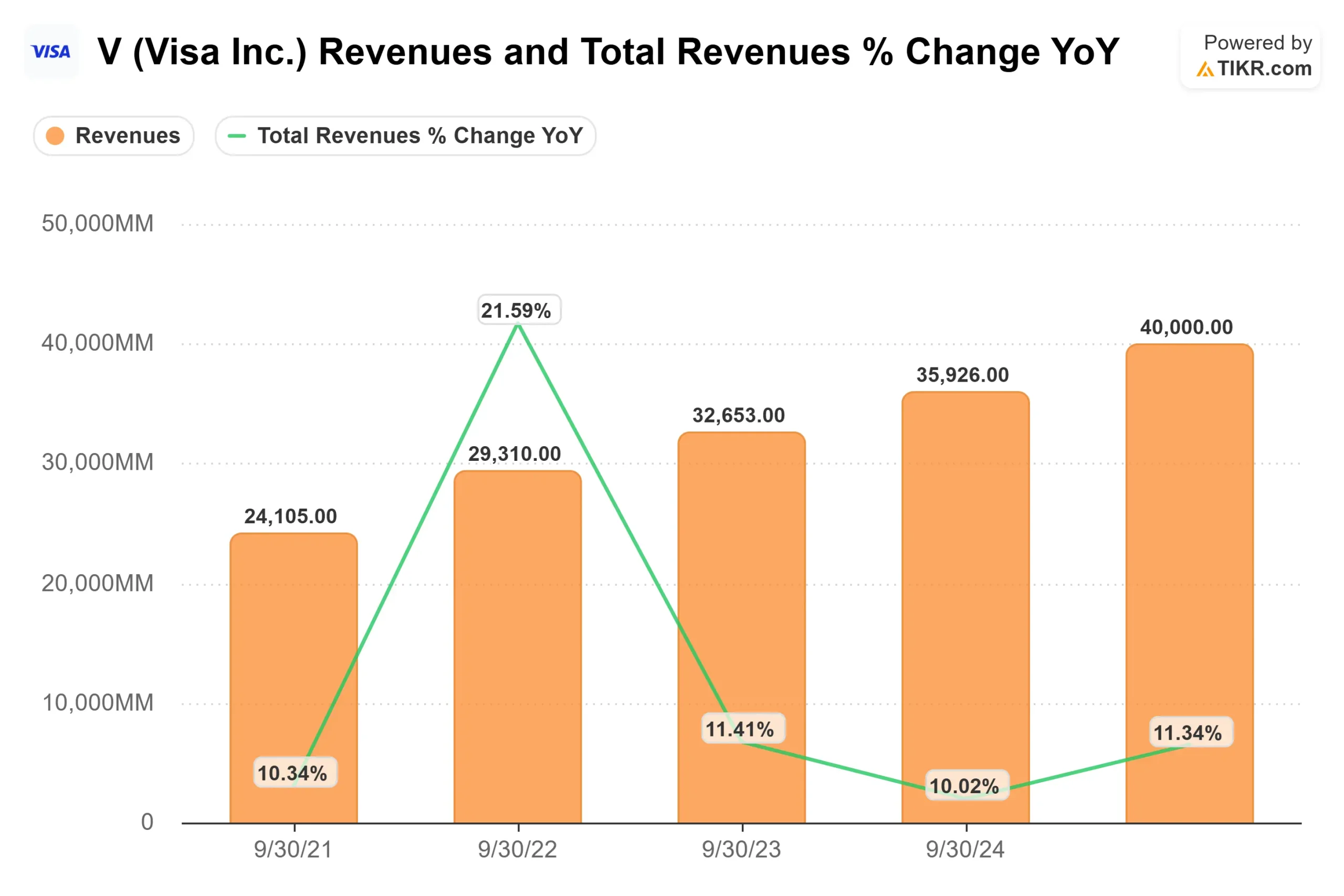

Suh described Q2 fiscal 2026 as “the best quarter of growth that we’ve seen in over a decade, excluding kind of the pandemic recovery period.” Revenue hit $11.2 billion, up 17% year-over-year, and value-added services, or VAS, Visa’s portfolio of software-like products, including risk solutions, tokenization, and data analytics, hit $3.3 billion. That is 30% of net revenue, growing 27%. For context, in fiscal 2019, VAS and commercial solutions combined were 23% of total revenue. VAS alone is now 30%.

But Suh’s bigger message at J.P. Morgan was structural. Visa is building what he calls a “Visa as a Service” stack, a layered infrastructure that lets banks, merchants, and developers build on top of Visa’s network, analogous to how cloud hyperscalers work. Each layer generates new revenue while flowing transactions back through Visa’s rails.

“We enable an ecosystem, all the participants in the ecosystem to build on our stack,” Suh said. “In turn, that grows the stack, it grows the ecosystem and the participants in it, including Visa.”

That framing redefines where Visa’s free cash flow growth comes from. It is not just more card swipes. It is a deepening platform attaching revenue at multiple layers above the core network.

See historical and forward estimates for Visa Inc. stock (It’s free!) >>>

A Volume Update That Postdated the Earnings Call

On the Q2 earnings call, Visa disclosed volume trends through April 21. At J.P. Morgan on May 19, Suh updated through May 14 a detail that earned no coverage because it postdated the call.

“We’ve seen all those levers U.S. payments volume, processed transactions, cross-border both travel and e-commerce all improve a little bit from that April 21 date,” he said. Cross-border, which softened in late April due to Ramadan timing and Middle East travel disruption, had recovered to February levels by mid-May. Suh was clear: the April dip was timing-driven, not a demand signal.

The reason Visa absorbed the disruption without meaningful damage is diversification. No single region represents more than 25% of Visa’s inbound cross-border volume, and e-commerce now accounts for roughly 40% of total cross-border. On the domestic side, U.S. payments volume grew 8% in Q2, with credit up 10% and debit up 7%. Commercial payment volume accelerated to 11% year-over-year growth, up from high single digits a year prior. Visa Direct, Visa’s push-payment network for real-time payouts, grew transactions 23% in the quarter.

Three Growth Vectors the Market Underweights

Tokenization is further along than most investors recognize. Over 50% of Visa’s e-commerce transactions are now tokenized, up 30% year-over-year. Tokens replace static card numbers with dynamic, transaction-specific credentials, which raises authorization rates and reduces fraud. Suh’s stated goal is near-100% e-commerce tokenization. The gap from 50% to near-100% is still a long runway, and stored credentials represent a separate, large opportunity that Visa is actively targeting.

Agentic commerce, where AI agents execute purchases on behalf of users, is what Suh called “beyond linear,” a new category rather than an extension of existing e-commerce. He sees it expanding Visa’s addressable market through four channels: accelerating payments digitization, unlocking B2B scenarios that have historically resisted digitization, creating net-new transactions as agents split and route payments, and potentially lifting global GDP growth by 80 to 150 basis points, according to third-party forecasts cited by Suh. Visa’s response is the Visa Trusted Agent Protocol, or VTAP, which sets security and trust standards for agents transacting with Visa credentials. Owning that trust layer is exactly where Visa’s existing competitive strength already sits.

Pismo and core banking modernization are the least-discussed pieces. Pismo, Visa’s cloud-native issuer processor and core banking platform, has expanded into 15 new countries since the acquisition, including France, the Philippines, Paraguay, and Romania in Q2. The landmark signal: Wells Fargo has entered an agreement to migrate its core banking to Pismo’s platform. Suh called it “endorsed by a very significant client.” Large banks replacing legacy core systems is a structural, multiyear opportunity, and Visa now offers a modern, cloud-native stack with global distribution to serve it. Visa also completed its acquisition of Prisma and Newpay in Argentina in February 2026 for $1.5 billion, adding a credit/debit issuer processor and a real-time payment and ATM network in a market where real-time payments represent 45% of private consumption expenditure.

The FIFA Catalyst Is 20 Days Out

One near-term catalyst Suh addressed directly: the FIFA World Cup 2026 begins roughly 20 days from the May 19 conference date, across 16 U.S. host cities through July. Visa is a global sponsor. Suh gave a concrete example: a Latin American client with 20 million cards ran a Visa World Cup campaign and saw a 10% uplift in active cards, translating directly into higher payment volume. Visa raised its full-year fiscal 2026 revenue guidance to low double-digit to low teens growth, and the World Cup is an explicit part of that rationale. The tournament should produce a measurable cross-border and VAS tailwind in Q3 and Q4.

See how Visa Inc. performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $329.91

- Target Price (Mid): ~$632

- Potential Total Return: ~92%

- Annualized IRR: ~16% / year

See analysts’ growth forecasts and price targets for Visa Inc. stock (It’s free!) >>>

The TIKR mid-case model, realized at 9/30/30, is driven by two CAGR engines: VAS expansion, now at 27% growth and 30% of revenue, and CMS acceleration, with commercial payment volume at 11% growth and Visa Direct at 23% transaction growth. Together they shift the revenue mix toward higher-margin, recurring services. The mid-case assumes a revenue CAGR of around 10% through the period and a net income margin of around 54%. LTM EBIT margin per TIKR stands at 67.1%, showing the operating leverage already embedded in the business.

The primary risk is regulatory. The Credit Card Competition Act legislation that would require merchants to route transactions over alternative networks remains a legislative overhang on the stock. Visa’s strategic answer is the ongoing shift toward VAS and CMS, both outside the interchange economics that regulators target. The more the mix shifts toward services, the less exposed total revenue becomes.

Per TIKR, the Street currently shows 28 Buys, 7 Outperforms, 3 Holds, 0 Underperforms, and 0 Sells, with a mean price target of $398.74, implying about 21% upside from today. The TIKR mid-case implies about 92% over roughly four and a half years. The difference is time horizon, not a quality disagreement.

Conclusion

The first clean test of this thesis arrives with Visa’s Q3 fiscal 2026 earnings, expected in late July the first quarter to fully capture FIFA World Cup volume. Watch VAS revenue as a percentage of total net revenue. If it holds above 25% growth and cross-border re-accelerates, the re-rating toward the Street’s $399 target becomes hard to argue against. If VAS growth decelerates materially below 20%, the mix-shift thesis needs revisiting. July’s report will answer the question.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Visa Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Visa Inc., and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Visa Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Visa Inc. on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!