Key Stats for Union Pacific Stock

- 52-Week Range: $211 to $276

- Current Price: $275

- Street Mean Target: $291

- Street High Target: $330

- Analyst Consensus: 13 Buys / 2 Outperforms / 7 Holds / 1 Underperform / 1 Sell

- TIKR Model Target (Dec. 2030): $422

Union Pacific Stock Beats Q1 Estimates as Merger Case Strengthens

Union Pacific (UNP), the Omaha-based freight railroad operating roughly 32,000 miles of track across the western United States, posted record first-quarter results on April 23 and filed an amended merger application with Norfolk Southern on April 30.

Adjusted earnings per share came in at $2.93, beating the consensus estimate of $2.86, while total operating revenue grew 3.2% to $6.22 billion against analyst estimates of $6.20 billion.

Freight revenue, the core revenue line that captures what customers pay to move cargo, rose 4% to $5.9 billion on 1% lower volume, with core pricing gains and higher fuel surcharge revenue each contributing meaningfully to the top-line advance.

CEO Jim Vena stated on the Q1 2026 earnings call that “we are more convicted now than we ever have been when you take a look at what’s in the merger application and all the detail that we’re putting forward,” directly linking the regulatory process to a structurally stronger long-term case.

The proposed $85 billion combination with Norfolk Southern, which would create the first coast-to-coast U.S. freight railroad, underpins the long-term thesis: projected annual shipper savings of $3.5 billion, removal of approximately 2.1 million trucks from U.S. roads, and 1,200 net new union jobs by year three.

The quarter was not without headwinds: fuel expense rose 7% on a 7% increase in average fuel price from $2.51 to $2.69 per gallon, and CFO Jennifer Hamann flagged that April fuel costs were running above $4 per gallon, which will pressure Q2 margins specifically.

Union Pacific reaffirmed its full-year 2026 outlook for mid-single-digit reported EPS growth and operating ratio improvement, while also reiterating its three-year CAGR target of high-single-digit to low-double-digit EPS growth through 2027.

Brokerages Lift UNP Targets as Merger Conviction Builds

The Q1 beat sparked a broad wave of price target increases across the Street, with at least nine brokerages raising their targets in the days following the April 23 report, signaling that analyst conviction on Union Pacific stock is rising despite near-term fuel noise.

The current consensus stands at 13 Buys, 2 Outperforms, 7 Holds, 1 Underperform, and 1 Sell, with a Street mean target of around $291, implying around 6% upside from the current price of $275.

The Street high sits at $330, held by both Morgan Stanley and Jefferies, reflecting how wide the range of outcomes is once the merger timeline becomes clearer.

Jefferies, rating the stock Buy with a target of $325, argued that near-term fuel costs are a transitory headwind and that efficiency gains and pricing discipline should offset the pressure, while remaining “most convicted on the long-term strategic and financial merits of the combined UP-NSC transcontinental network.”

Raymond James, also at Buy with a target of $310, emphasized that productivity gains and latent network capacity continue to drive the core Union Pacific story, with the Norfolk Southern merger adding longer-term upside rather than serving as the foundational bull case.

Benchmark, at Buy with a target of $300, noted that “ultimately, independent of the merger, we continue to believe business development wins, productivity gains, and operating leverage put UNP in a favorable position,” separating the standalone railroad quality from the optionality value of the combination.

Wall Street’s split between strong bulls targeting $310 to $330 and more cautious holders near $270 to $285 reflects a genuine debate: whether the STB approval timeline accelerates or extends, and whether any required concessions materially dilute the financial case for a coast-to-coast network.

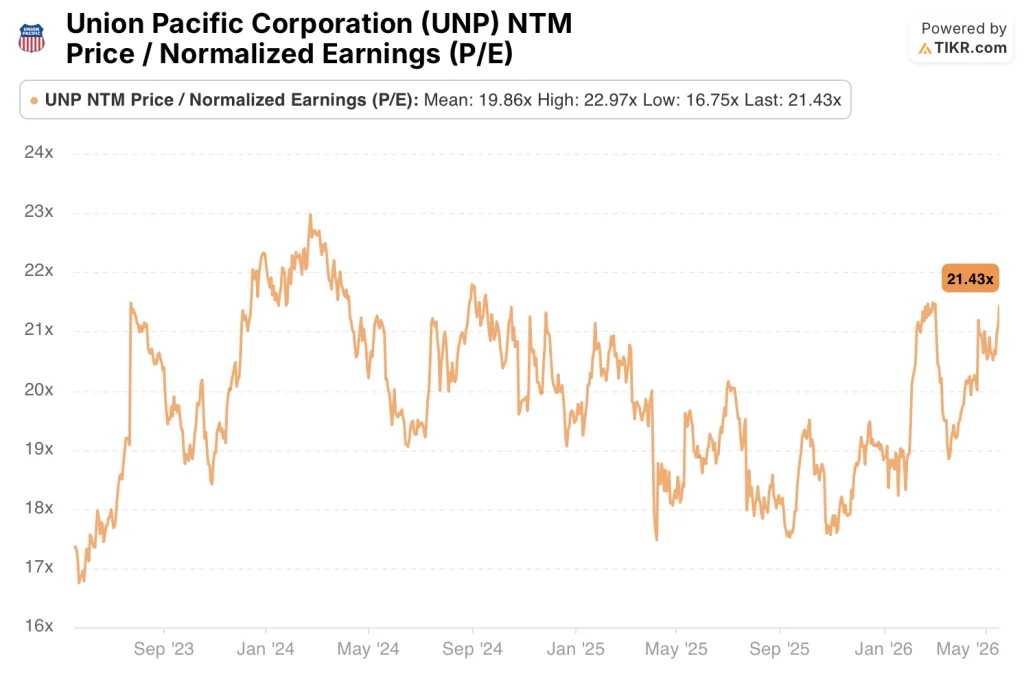

At 21x forward earnings against a historical mean of around 20x, Union Pacific stock appears overvalued on a standalone multiple basis, with the merger outcome representing the only credible path to justifying a sustained premium to historical norms.

TIKR’s Model Points to $422 for UNP as Merger Optionality Stacks

TIKR’s valuation model prices Union Pacific at $422 by December 2030, implying a 53% total return from the current price of $275 over the next 4.6 years, or 9.7% annualized.

The mid-case assumptions behind that target are not heroic: 7% revenue CAGR and net income margins expanding to 33%, figures that reflect a combined network absorbing industrial and intermodal volume rather than a standalone railroad running at peak efficiency.

At 21x forward earnings above its historical mean of around 20x, Union Pacific stock carries a stretched entry multiple, and the $422 target only holds if the merger runway materializes on the timeline the April 30 filing implies.

TIKR’s low case reaches $473 by 2035 at a 6.5% IRR, anchored to 6.3% revenue growth and 31% net income margins, consistent with a standalone Union Pacific running cleanly without merger synergies.

The mid case reaches $607 at a 9.6% IRR under 7% revenue growth and 33% margins, reflecting successful integration and the freight volume recovery that three consecutive record intermodal quarters suggest is already underway.

The high case produces $753 at a 12.4% IRR, requiring 7.7% revenue growth, 34% margins, and synergy realization that exceeds the $3.5 billion annual projection the merger application projects.

Should You Invest in Union Pacific Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Union Pacific Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Union Pacific Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UNP stock on TIKR for Free →