Key Stats for Adobe Stock

- 52-Week Range: $224 to $423

- Current Price: $256

- Street Mean Target: $328

- Street High Target: $487

- Analyst Consensus: 12 Buys / 3 Outperforms / 20 Holds / 1 No Opinion / 4 Sells

- TIKR Model Target (Nov. 2030): $415

Adobe Launches a $25 Billion Buyback and a New AI Platform as Investor Confidence Erodes

Adobe Inc. (ADBE), the creator economy’s largest software platform with over 850 million monthly active users, announced a $25 billion stock repurchase program and unveiled its CX Enterprise AI agent suite following Q1 fiscal 2026 earnings in March, as the company attempts to reframe a 30% year-to-date decline in Adobe stock around execution rather than fear.

Adobe delivered Q1 revenue of $6.40 billion, growing 12% year-over-year and beating the IBES estimate of $6.28 billion by more than $120 million, a result that validated the underlying business even as sentiment on the stock remained deeply negative.

The earnings beat was driven by strength across both customer groups: Business Professionals and Consumers subscription revenue reached $1.78 billion, up 16% year-over-year, while Creative and Marketing Professionals subscription revenue hit $4.39 billion, up 12%.

The single most clarifying metric in the quarter was Firefly, Adobe’s generative AI studio, which crossed $250 million in ending ARR while generative credit consumption rose more than 45% quarter-over-quarter, a pace that more than doubled from the prior year’s baseline and reflects real workflow adoption, not experimental use.

CFO Dan Durn stated on the Adobe Summit 2026 investor day that “our new $25 billion share repurchase authorization is a direct expression of confidence in our robust cash flow and the long-term value we are delivering to investors,” a remark tied directly to the $2.96 billion in operating cash flow Adobe generated in Q1 alone.

Adobe completed its acquisition of Semrush in late April, adding SEO and generative engine optimization capabilities to the CX Enterprise platform at a moment when enterprise customers are asking how to ensure their brands remain visible as consumers shift discovery toward LLMs and AI agents.

The $25 billion buyback, which runs through April 2030, follows a period in which Adobe reduced its net share count by nearly 10% over the prior three years, and it comes alongside new partnerships with AWS, Anthropic, Google Cloud, IBM, Microsoft, NVIDIA, and OpenAI, each of which expands the distribution surface for Adobe’s AI agent capabilities.

Adobe Stock Draws a Cautious Majority as AI Disruption Fears Outpace Q1 Results

The core tension in Adobe stock analysis right now is not about whether the business is growing, it is about whether growth will hold as agentic AI tools commoditize creative workflows from below.

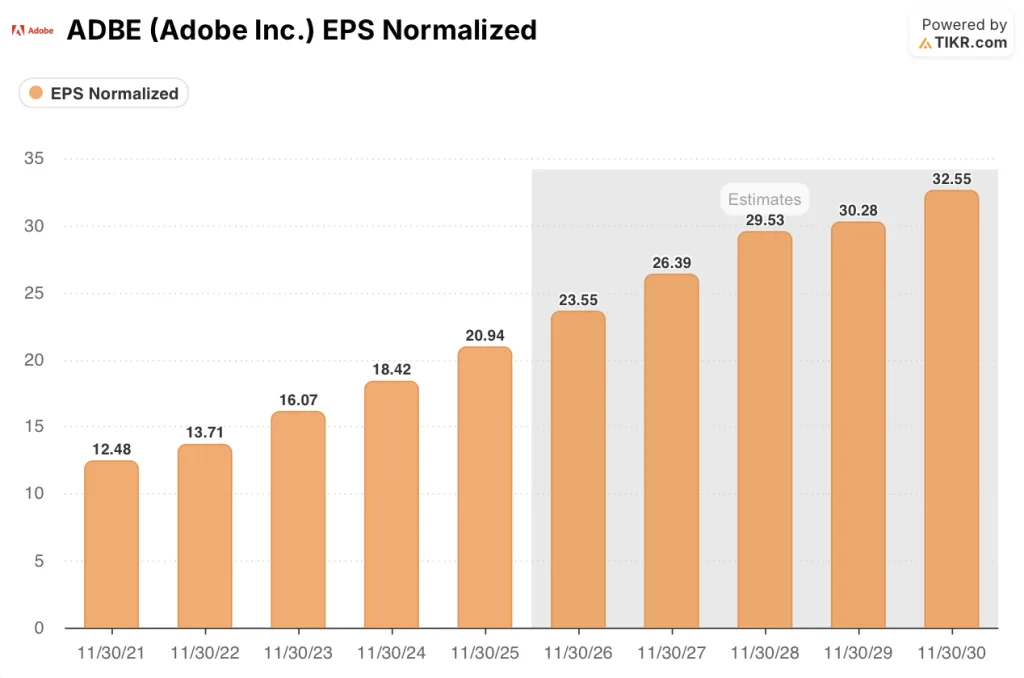

Adobe’s Q1 non-GAAP EPS of $6.06 grew 19% year-over-year, the fastest pace in several quarters, and on an annual basis consensus projects EPS climbing from $20.94 in fiscal 2025 toward around $24 in fiscal 2026 and roughly $33 by fiscal 2030, a compounding trajectory anchored to CC Pro expansion and the scaling Firefly ARR book.

That EPS trajectory is real: in Q1, AI-first applications ending ARR more than tripled year-over-year, and the three CX enterprise product lines collectively exceed $1 billion each in ARR, with aggregate growth above 20% year-over-year.

Despite those results, 34 of the 40 analysts currently covering ADBE have moved to a Hold or worse stance, with 20 Holds and 4 Sells as of the latest data, a distribution that reflects broad-based concern rather than isolated dissent.

The Wall Street mean price target for Adobe stock sits at around $327, implying roughly 28% upside from the current price of $256, yet that gap has been widening for months as targets compress alongside the stock rather than converging toward it.

Mizuho’s April downgrade to Neutral, cutting its price target to $270 from $315, captured the bear case explicitly: competition in the prosumer and SMB segments from tools like Canva is threatening Adobe’s long-term terminal value, while Firefly’s AI-first ARR still represents less than 2% of the company’s roughly $26 billion total ARR base.

The bull case, anchored by the 15 Buy or Outperform ratings still on record, rests on the idea that Adobe’s 850 million monthly active users, double-digit ARR growth across enterprise CXO solutions, and the Semrush acquisition create a defensible moat that smaller AI-native entrants cannot replicate.

Trading at this valuation with Q1 EPS of $6.06 already 19% above the prior year and a $25 billion buyback reducing share count meaningfully through 2030, Adobe stock appears undervalued given the disconnect between its earnings growth rate and the multiple the market is currently assigning it.

TIKR’s Model Points to $415 for Adobe Stock: The Case Depends on One Number

TIKR’s base case values Adobe at $415 per share, projecting a 9.6% revenue CAGR through 2035 and a 36% net income margin, assumptions grounded in Adobe’s $26 billion ARR base, Firefly’s 45%-plus quarterly credit consumption growth, and the Semrush GEO capabilities now integrated into the CX Enterprise stack.

With TIKR’s mid-case implying around 63% total return over 4 and a half years and Adobe’s Q1 EPS of $6.06 already growing at 19% year-over-year, the stock is undervalued relative to the earnings trajectory the model supports at current prices.

The entire argument hinges on whether Firefly crosses from a $250 million ARR line item into a $1 billion-plus business before AI-native competitors capture the SMB and prosumer segments Adobe currently dominates.

What Has to Go Right

- Firefly ending ARR, which grew 75% quarter-over-quarter in Q1, sustains a pace that brings it toward the $1 billion ARR threshold management identified as the next major milestone, giving the market a concrete re-rating catalyst.

- The Semrush acquisition, completed in late April, adds SEO and generative engine optimization to CX Enterprise at a moment when enterprise customers are funding brand visibility budgets specifically because their brands are disappearing from LLM-driven discovery.

- The $25 billion buyback reduces share count meaningfully, with roughly $3.89 billion already remaining on the prior authorization exiting Q1, compounding per-share earnings growth on top of the organic EPS trajectory.

- Enterprise CXO solutions across content supply chain, customer engagement, and brand visibility collectively grew above 20% year-over-year in Q1, with the pipeline for LLM Optimizer, Sites Optimizer, and Brand Concierge generating over 650 active customer trials.

What Could Go Wrong

Anthropic’s Claude Design launch in April put a competing design and prototyping tool directly inside a widely used AI chat interface, accelerating the timeline on which prosumer users may reach for free AI tools instead of Creative Cloud subscriptions.

AI-first ARR remains below 2% of total ARR per Mizuho’s analysis, and if the freemium MAU base of 80 million creative users converts at a slower pace than Adobe’s model assumes, the phase-shift from usage to ARR growth could extend beyond fiscal 2026.

Adobe’s traditional stock licensing book, approximately $450 million in revenue, is declining faster than management anticipated, and if generative AI does not fully absorb that demand at equivalent or better unit economics, aggregate ARR growth faces a structural headwind.

Shantanu Narayen’s departure as CEO, announced in March, introduces leadership transition risk at exactly the moment Adobe’s AI product roadmap requires the most consistent execution, and the successor has not yet been named.

Is Adobe stock a buy right now?

The valuation case for Adobe stock is stronger than the current consensus suggests.

TIKR’s base case targets around $415 per share, implying roughly 63% total return over 4 and a half years from the current price of $255.64. Q1 non-GAAP EPS of $6.06 grew 19% year-over-year, and the $25 billion buyback reinforces per-share earnings compounding.

The key variable is Firefly ARR velocity: if it sustains its 75% quarter-over-quarter growth pace into the back half of fiscal 2026, the re-rating case becomes much easier to defend.

Should You Invest in Adobe Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Adobe Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Adobe Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ADBE stock on TIKR for Free →