Key Stats for Union Pacific Stock

- This Week Performance: -4%

- 52-Week Range: $204.7 to $268.4

- Current Price: $244.1

What Happened?

Union Pacific (UNP), the western railroad operator whose 32,000-mile network moves everything from grain to consumer goods, posted a best-ever $7.1 billion in net income for 2025 even as its proposed $85 billion merger with Norfolk Southern hit a regulatory wall that now defines the stock’s next chapter at $244.10, well below its 52-week high of $268.14.

Last January, the Surface Transportation Board rejected the merger application as incomplete after Union Pacific submitted nearly 7,000 pages, then on February 4 the railroad signed a $1.2 billion locomotive modernization deal with Wabtec covering more than 1,700 AC4400 engines, the largest such investment in rail industry history, sending shares up 3.3% to $249.60.

Union Pacific’s adjusted operating ratio, the railroad industry’s core efficiency measure showing what percentage of each revenue dollar goes to costs, improved 60 basis points to 59.3% in 2025, as the company moved 1% more volume with 3% fewer employees, a workforce productivity record that outpaces peer BNSF’s reported efficiency trajectory.

Chief Executive Jim Vena stated at the Barclays 43rd Annual Industrial Select Conference on February 18 that “we are even more sure and convicted that we can gain 24 to 48 hours on those cars by removing the touch points,” tying that service advantage directly to the competitive pressure the combined railroad would place on rivals forced to respond with price cuts.

With a committed merger refiling deadline of April 30, a 2027 close target, $3.3 billion in 2026 capital investment anchored to Gulf Coast terminal expansion and Wabtec deliveries beginning that year, and a reaffirmed high-single to low-double-digit EPS CAGR through 2027, Union Pacific has stacked three reinforcing catalysts that could close the gap back toward $268.

Wall Street’s Take on UNP Stock

The STB refiling deadline of April 30 and the $1.2 billion Wabtec modernization program together confirm that Union Pacific’s efficiency compounding is structural, not cyclical, and the earnings trajectory reflects that directly.

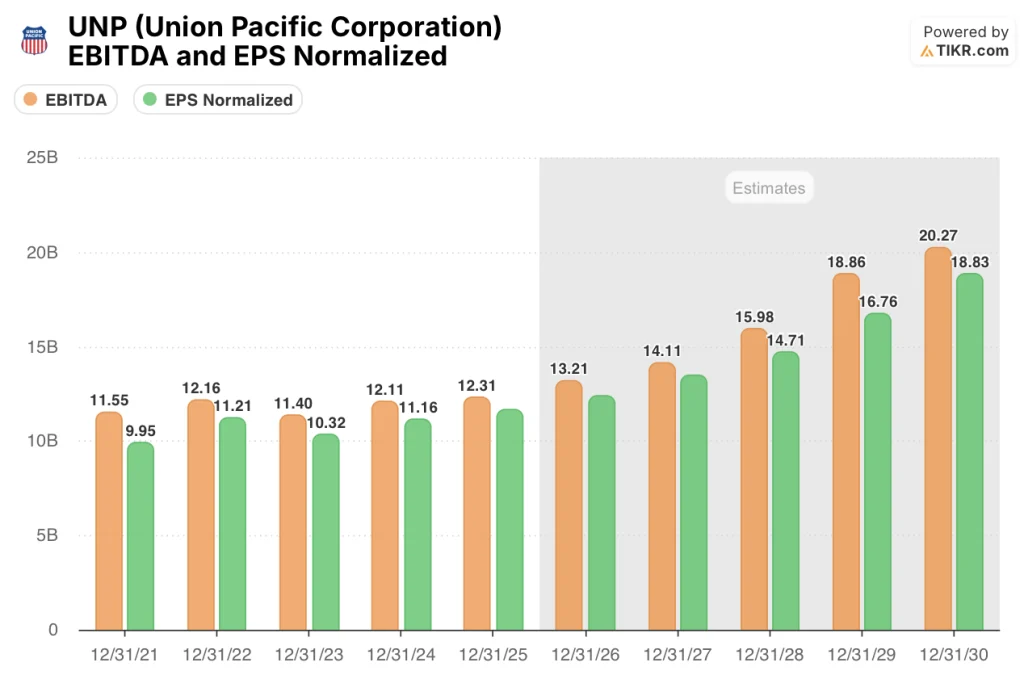

Meanwhile, Union Pacific’s EBITDA is estimated to grow from $12.3 billion in 2025 to $20.3 billion by 2030, while normalized EPS compounds from $11.66 to $18.83, a 7.3% CAGR that makes the mid-single-digit 2026 guide look like a floor, not a ceiling.

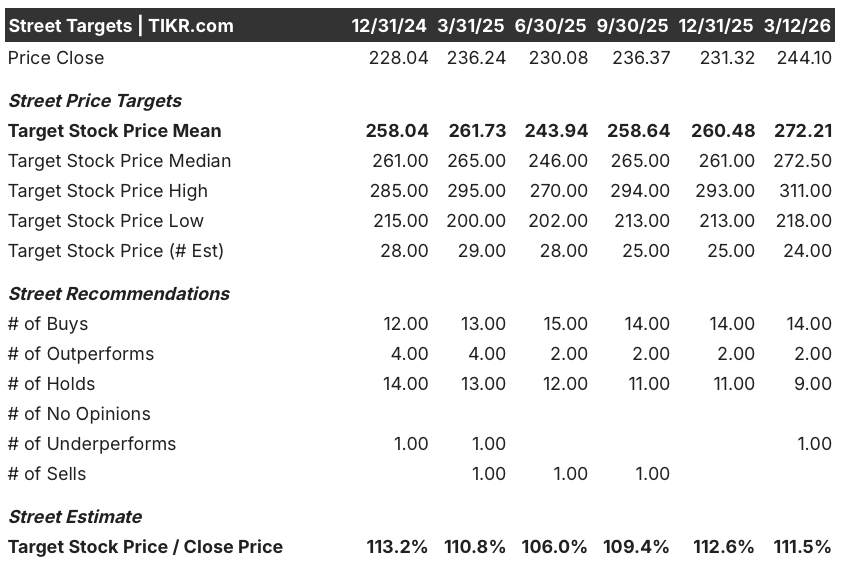

Fourteen analysts currently rate UNP a buy or outperform, nine hold, and one underperforms, with a mean price target of $272.21 implying 11.5% upside from $244.10, a consensus that prices in regulatory progress but not full merger optionality.

The spread between the analyst low target of $218 and the high of $311 maps precisely onto the two forces already introduced: the $218 floor reflects a prolonged STB delay scenario, while the $311 ceiling prices in a first-half 2027 merger close and the $2 billion in net revenue synergies management has committed to.

What Does the Valuation Model Say?

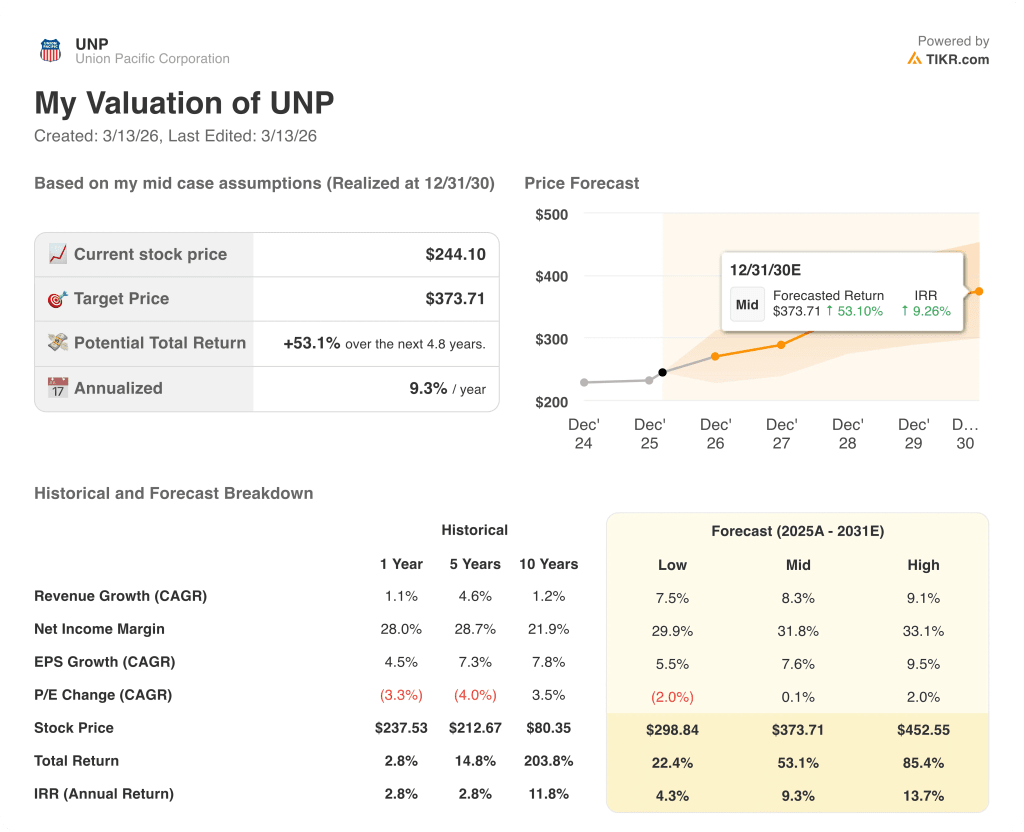

The TIKR mid-case values UNP at $373.71 by December 2030, a 53.1% total return on the current price, driven by an assumed revenue CAGR of 8.3% and net income margin expansion from 28.3% to 31.8%.

The market is treating the April 30 refiling as a delay, but the EBITDA margin is already tracking from the 2023 trough of 47.3% back toward 52.2% in 2026 and 54.4% by 2030, a 420-basis-point recovery the current price does not reflect.

Union Pacific moved 1% more volume with 3% fewer employees in 2025, the operational proof that the 8.3% revenue CAGR assumption in the TIKR model is grounded in demonstrated network capacity, not projection optimism.

CFO Jennifer Hamann confirmed on January 27 that the company fully expects to improve its operating ratio in 2026 and remain the industry leader in both operating ratio and return on invested capital, signaling that margin discipline holds even without macro tailwinds.

The core risk is a prolonged STB review or outright rejection of the Norfolk Southern merger application, which would eliminate the $2 billion net synergy target and force Union Pacific to redeploy the paused $4 billion to $4.5 billion share buyback program as its primary value lever instead.

Watch the April 30 STB refiling: if Union Pacific submits on schedule and the comment period compresses toward 45 days as Vena has targeted, the first-half 2027 merger close timeline holds and the TIKR mid-case target of $373.71 comes into view.

Should You Invest in Union Pacific Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UNP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Union Pacific Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UNP stock on TIKR for Free →