Key Stats for JPMorgan Stock

- This Week Performance: -2.7%

- 52-Week Range: $202.2 to $337.3

- Current Price: $287.5

What Happened?

JPMorgan (JPM), the largest US bank by assets, deliberately absorbed a $9 billion expense increase in 2026 while guiding for $104.5 billion in net interest income, betting that scale compounds into dominance.

The Q4 earnings report delivered $46.8 billion in quarterly revenue, up 7% year-over-year, with equities markets revenue surging 40% and full-year ROTCE hitting 20%, while the $2.2 billion Apple Card reserve build masked underlying earnings strength.

The engine is a $19.8 billion technology budget in 2026 alone, with AI doubling production use cases in a single year, and the February 23 company update confirming Q1 investment banking fees tracking mid-to-high-teens growth across debt, equity, and advisory markets.

Jeremy Barnum, Chief Financial Officer, stated at the February 23 company’s special call that “our PPNR CAGR continues to outpace both revenue and expense growth, demonstrating the power of sustained investment in the scale of franchise,” directly tied to the $9 billion expense increase the market is currently penalizing.

With Apple Card integration unlocking a partnership with the world’s most valuable consumer technology company, $19.8 billion in annual technology spend compounding against a $337 52-week high, and private credit market stress emerging March 12 creating potential capital deployment opportunities, JPMorgan’s structural advantages sharpen precisely when competitors face stress.

Wall Street’s Take on JPM Stock

The $9 billion expense increase the market is penalizing directly funds the technology platform and Apple Card integration that underpin JPMorgan’s path to $104.5 billion in net interest income and sustained ROTCE above 17%.

The normalized EPS figures, which strip out one-time items like the $2.2 billion Apple Card reserve build to show the bank’s true recurring earnings power, climb from $19.73 in FY 2025 to a forecast $21.91 in FY 2026 and $29.78 by FY 2030, a 7.7% CAGR, while total revenue grows from $182.5 billion to a projected $223.1 billion over the same period.

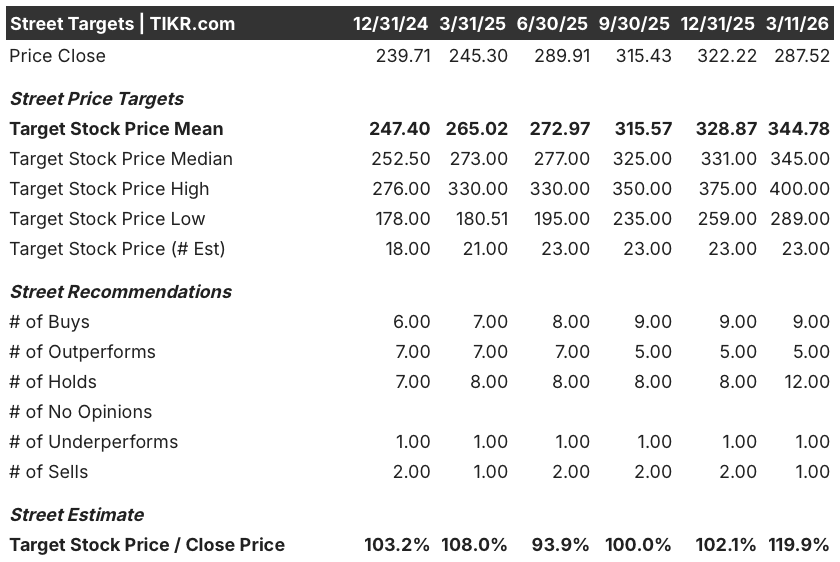

Sentiment is more divided than the bull case suggests: 23 analysts cover JPM with 9 buys, 5 outperforms, 12 holds, 1 underperform, and 1 sell, producing a mean price target of $344.78 that implies nearly 20% upside from the current $287.52 price.

The analyst target range spans $289 on the low end to $400 on the high, where the ceiling case prices in full Apple Card integration upside and accelerating investment banking recovery, while the floor reflects execution risk if the $9 billion expense build fails to convert into revenue growth.

What Does the Valuation Model Say?

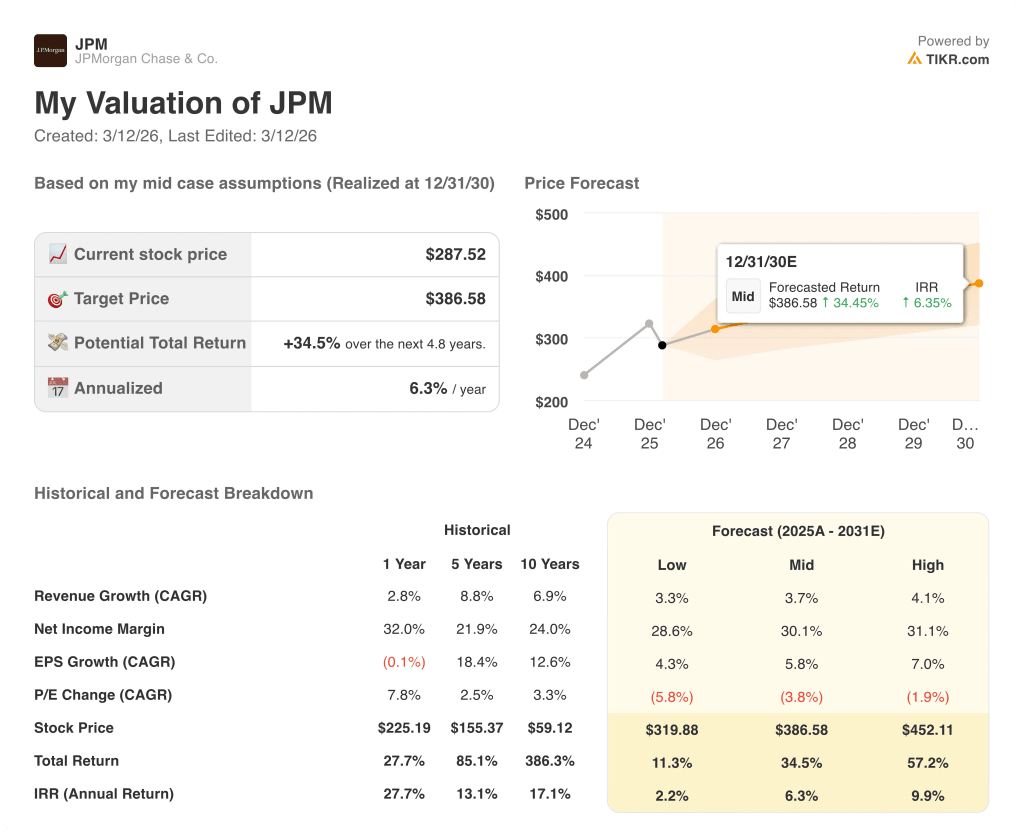

The TIKR mid-case target of $386.58 by December 2030 implies 34.5% total return at a 6.3% annualized IRR, pricing in 3.7% revenue CAGR and net income margins stabilizing around 30.1% as the expense cycle peaks and operating leverage reasserts.

The market prices JPMorgan as an expense problem, but normalized EPS grew from $12.09 in FY 2022 to $19.73 in FY 2025, a 63% recovery the current valuation does not fully credit.

AI doubled production use cases in a single year while the $19.8 billion technology budget identified $600 million in efficiency savings, directly validating the model’s assumption that investment spend converts into margin over time.

Jamie Dimon stated at the February 23 company update that JPMorgan can deploy $40 billion to $50 billion organically over the next five years, confirming that excess capital, not earnings weakness, drives the current discount.

The primary risk is private credit market stress: JPMorgan’s March 12 loan markdowns signal a potential credit cycle turn that would pressure the model’s 30.1% net income margin assumption and compress ROTCE toward the lower scenario band.

Q1 2026 earnings, where investment banking fees are tracking mid-to-high-teens growth and markets revenue is also guiding mid-teens, will confirm whether the $104.5 billion full-year NII target is tracking and whether the expense investment is delivering.

Should You Invest in JPMorgan Chase & Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up JPM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track JPMorgan Chase & Co. credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze JPM stock on TIKR for Free →