Key Stats for Emerson Electric Stock

- This Week Performance: +0.9%

- 52-Week Range: $90.1 to $165.2

- Current Price: $139.6

What Happened?

Emerson‘s Ovation business, the power plant control system platform now winning behind-the-meter data center automation contracts, posted 74% order growth in Q1 as the $139.57 industrial automation leader raised its adjusted EPS guide to $6.40-$6.55 on 9% underlying order growth, its fourth consecutive quarter of acceleration.

Stephens on February 9 raised its Emerson price target to $155 from $145 and lifted FY 2026 adjusted EPS estimates to $6.48 on the strength of broad order momentum across power, LNG, and Test & Measurement, which grew orders 20% in the quarter.

Trailing 12-month orders grew 6% against a $7.9 billion backlog up 9% year-over-year, while software annual contract value hit $1.6 billion with 9% growth and a path to 10%-plus for the full year, converting Emerson’s $42 billion portfolio transformation into recurring revenue visibility.

On February 4, Emerson released next-generation Nigel AI, upgrading its LabVIEW test automation assistant from advisor to author, compressing engineering workflows from hours to minutes and generating over $100 million in outstanding quotations for the related Ovation Virtual Advisor product alone.

Lal Karsanbhai, President and CEO, stated at the Citi conference on February 18 that “the entire American administration’s industrial policy favors those 5 markets,” connecting Emerson’s growth verticals in power, LNG, semiconductor, life sciences, and defense directly to the 18% North American order surge.

Emerson Electric’s 2028 framework targeting $21 billion in revenue, 30% adjusted segment EBITA margins, and $8 in adjusted EPS, backed by $10 billion in planned shareholder returns and 240 basis points of margin expansion, frames the current $139.57 price against an earnings power story the market has yet to fully credit.

Wall Street’s Take on EMR Stock

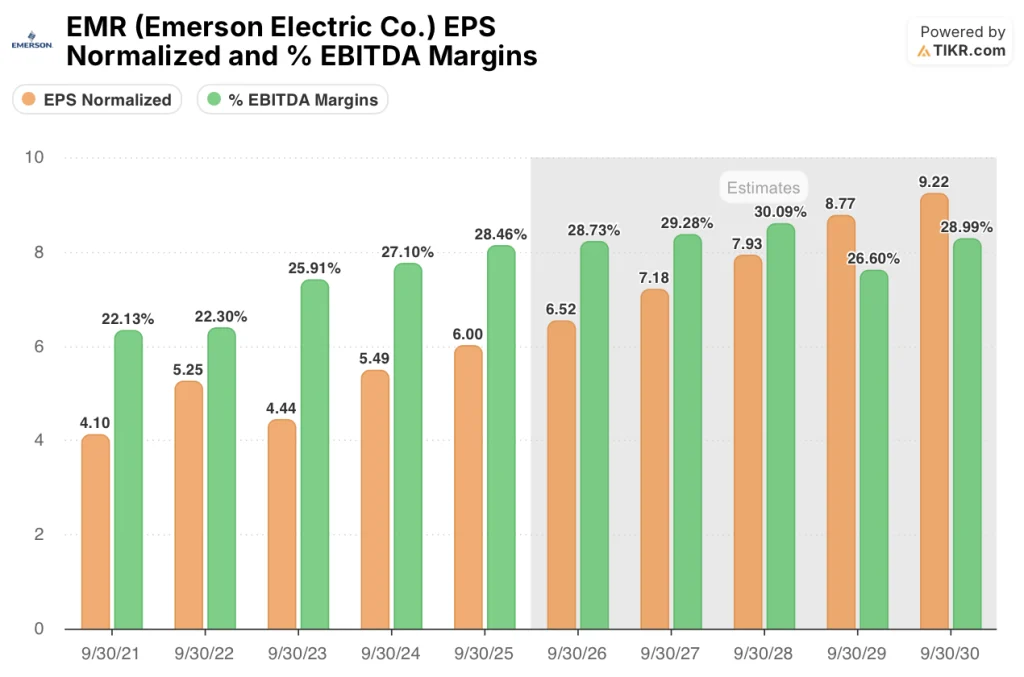

Emerson’s 74% Ovation order surge and 9% overall order acceleration translate directly into the raised FY 2026 adjusted EPS guide of $6.40-$6.55, with consensus projecting 8.6% EPS growth to $6.52 as the $42 billion portfolio transformation begins converting backlog into earnings.

Adjusted segment EBITA margin reached 27.7% in Q1 against a 28% full-year target and a 2028 goal of 30%, while consensus projects EBITDA margins expanding from 28.7% in FY 2025 to 30.1% by FY 2028E.

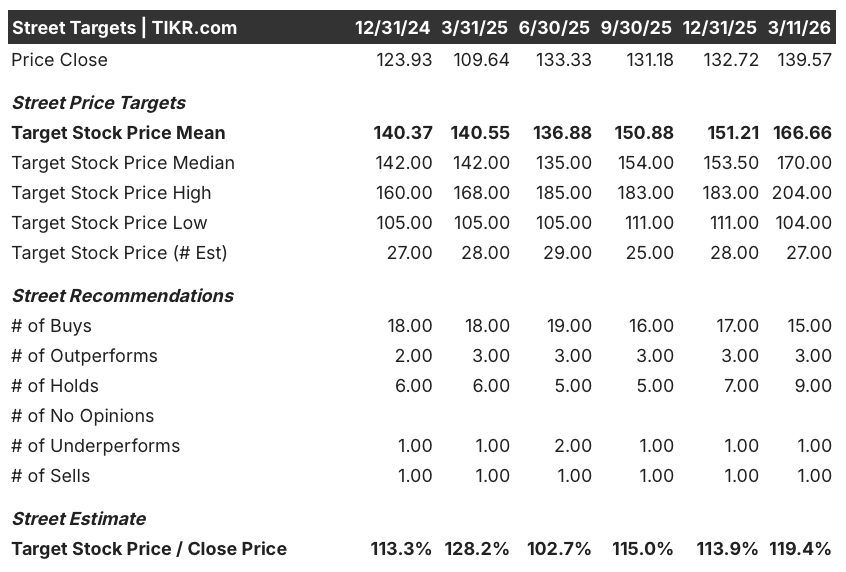

Wall Street’s conviction tilts decisively bullish: 15 buys, 3 outperforms, 9 holds, 1 underperform, and 1 sell among 29 analysts produce a $166.66 mean price target, implying 19.4% upside from $139.57 as the Street prices in sustained order momentum and margin expansion toward the 2028 framework.

Targets range from $104 at the low, reflecting risk that European and Chinese softness in chemicals and automotive persists, to $204 at the high, pricing in full achievement of the $8 adjusted EPS and 30% EBITA margin targets by 2028 as power and LNG orders convert to shipments.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of $198.72 implies 42.4% total return over 4.5 years. It assumes 5.5% revenue CAGR and net income margins expanding from 18.9% to 20.3%, driven by the 240 basis points of margin expansion Emerson committed to at its November Capital Markets Day.

The market prices Emerson at 21.4x FY 2026E EPS of $6.52 while the 2028 framework targets $8 in adjusted EPS, suggesting the current multiple ignores 23% earnings growth over the next two fiscal years.

Four consecutive quarters of accelerating orders (4%, 4%, 6%, 9%) and a $7.9 billion backlog up 9% validate the model’s 5.5% revenue CAGR before the greenfield power generation cycle even begins.

Over $100 million in outstanding quotations for the Ovation Virtual Advisor, released less than two quarters ago, confirms that Emerson’s AI-embedded software strategy is generating commercial traction, not just product announcements.

Sustained weakness in China (down low single digits) and European chemicals could compress order growth below mid-single digits and stall the margin expansion path from 28% to 30%.

Q2 FY 2026 results will reveal whether the 1%-2% underlying sales growth and $1.50-$1.55 EPS guide hold, confirming the backlog-to-revenue conversion that underpins the second-half acceleration to 6%.

Should You Invest in Emerson Electric Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up EMR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Emerson Electric Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze EMR stock on TIKR for Free →