Key Stats for TransDigm Stock

- Past-Week Performance: -3.2%

- 52-Week Range: $1,137.1 to $1,623.8

- Current Price: $1,140

What Happened?

TransDigm Group (TDG) — the Cleveland-based maker of highly engineered, proprietary aerospace components whose parts are embedded in virtually every commercial and military aircraft — posted a fiscal Q1 adjusted EPS of $8.23, beating the IBES estimate of $8.10, while raising full-year revenue guidance to a $9.94 billion midpoint even as its stock sits 30% below its 52-week high of $1,623.83, currently trading at $1,140.03.

On February 3, TransDigm reported Q1 net sales of $2,285 million against an IBES estimate of $2,258 million, raised its fiscal 2026 EBITDA As Defined guidance midpoint by $60 million to $5,210 million, and lifted its adjusted EPS midpoint to $38.38, though that figure trails the LSEG consensus of $39.03 due to higher interest expense tied to its $2 billion debt raise completed February 13 to fund three pending acquisitions.

The operational backbone of that guidance raise is a 52.4% EBITDA As Defined margin in Q1, achieved despite roughly 200 basis points of dilution from recently closed acquisitions, supported by 17% pro forma commercial OEM revenue growth as Boeing and Airbus resumed production ramp-ups after supply chain disruptions that dragged on through fiscal 2025; Jefferies, which raised its price target to $1,635 from $1,565 on February 9, cited this commercial aerospace recovery as the central re-rating catalyst.

CEO Michael Lisman stated on the Q1 2026 earnings call that “our Q1 results ran ahead of our expectations, and we raised our sales and EBITDA As Defined guidance for the year,” directly anchoring the guidance revision to first-quarter outperformance driven by Boeing and Airbus production recovery and diligent cost execution across TransDigm’s 53 operating units.

TransDigm’s $2.2 billion acquisition of Jet Parts Engineering and Victor Sierra Aviation — proprietary aftermarket parts and PMA (manufacturer-approved alternative parts) businesses that collectively generated $280 million in 2025 revenue — combined with the $960 million Stellant Systems deal and roughly $10 billion in remaining M&A capacity, positions the company to compound its aftermarket revenue base, sustain free cash flow of approximately $2.4 billion in fiscal 2026, and extend a capital allocation model that has consistently targeted 20% IRR on acquisitions across both commercial and defense end markets.

Wall Street’s Take on TDG Stock

The Q1 guidance raise — revenue midpoint up $90 million to $9.94 billion and EBITDA As Defined up $60 million to $5.21 billion — confirms that TDG’s Boeing and Airbus production recovery is converting into financials faster than management itself projected.

TDG’s 52.4% EBITDA as Defined margin in Q1, achieved while absorbing 200 basis points of dilution from recently integrated acquisitions, signals that the company’s base businesses expanded margins beyond expectations, supporting TIKR’s mid-case net income margin estimate of 26.3% through fiscal 2031.

The TIKR model projects EPS growing at an 8% CAGR through fiscal 2031, grounded in the company’s fiscal 2026 adjusted EPS midpoint of $38.38 and management’s track record of delivering 20% IRR on every acquisition it has closed, including the three pending deals worth $3.16 billion combined.

Twelve analysts rate TDG a Buy, four an Outperform, and six a Hold, with a mean price target of $1,591.25 — implying 39.6% upside from the current $1,140.03 close, a spread that reflects how sharply the stock has dislocated from the Street’s fundamental view since its 52-week high of $1,623.83.

The analyst price target range runs from $1,317.00 on the low end to $1,900.00 on the high end; the low anchors to the tariff and interest expense risks that dragged Q1 net income 9.7% below the prior year, while the high reflects full commercial OEM recovery and successful integration of Stellant, Jet Parts Engineering, and Victor Sierra.

What Does the Valuation Model Say?

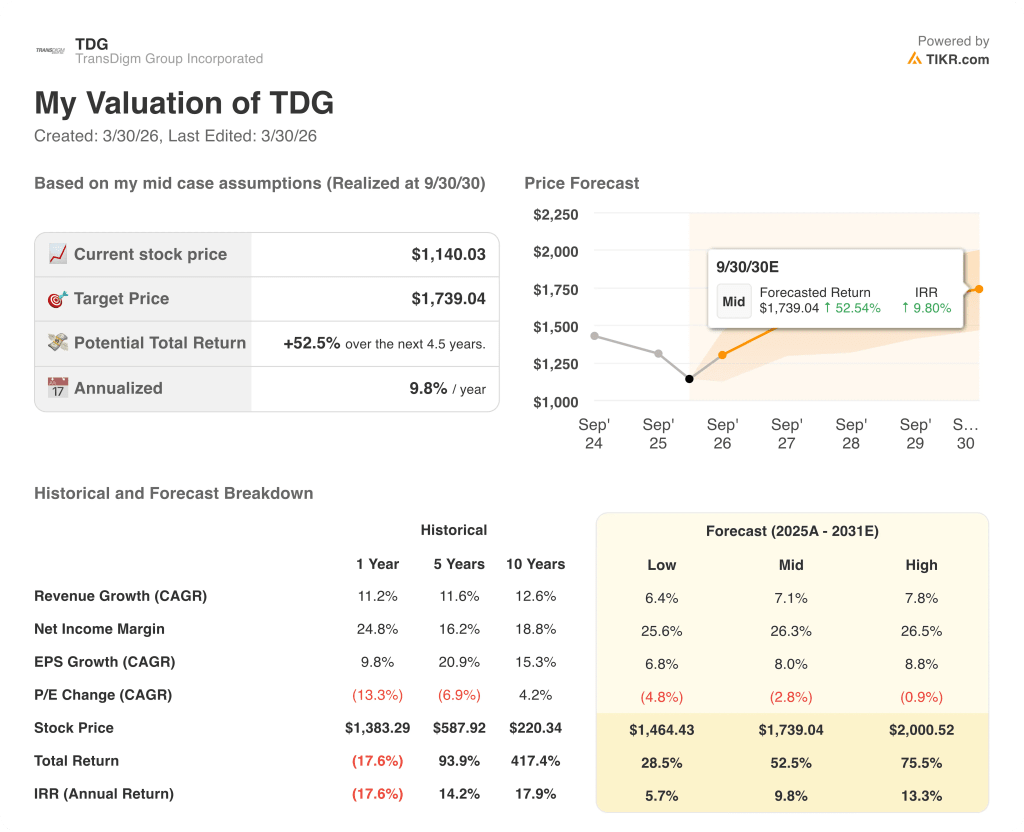

Wall Street’s best ideas don’t stay hidden for long. Catch analyst upgrades, earnings beats, and revenue surprises on thousands of stocks the moment they happen with TIKR for free →TIKR’s mid-case target of $1,739.04, realized at September 30, 2030, assumes a 7.1% revenue CAGR from fiscal 2025 through fiscal 2031 — a rate the company has already cleared on a one-year basis at 11.2% and a ten-year basis at 12.6%, making the model assumption conservative relative to history.

The market prices TDG as though its debt load is a structural ceiling, yet 75% of the $30 billion gross debt balance is fixed through fiscal 2029, and free cash flow guidance of $2.4 billion for fiscal 2026 alone covers more than two-thirds of the $3.16 billion acquisition spend.

CFO Sarah Wynne confirmed on the Q1 call that the company deployed over $100 million in share repurchases opportunistically in the quarter, a direct signal that management views the current price as a mispricing, not a fair valuation.

The primary risk to the TIKR model’s 7.1% revenue CAGR assumption is a stall in Boeing and Airbus production ramp-ups; management guided commercial OEM revenue growth in the high single digits to mid-teens, and any slip back toward the low end collapses the margin mix and FCF generation that anchors the $1,739.04 target.

The Q2 fiscal 2026 earnings report is the next confirmation point: watch whether commercial aftermarket bookings convert the double-digit book-to-bill ratio from Q1 into revenue growth above 7%, which would validate that distributor inventory headwinds are reversing from drag to tailwind as management signaled on the February 3 call.

Should You Invest in TransDigm Group Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TDG stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track TransDigm Group Incorporated alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TDG stock on TIKR for Free →