Super Micro Computer, Inc. (NASDAQ: SMCI) has been one of the market’s hottest AI hardware stories. After a massive run-up, the stock now trades near $45/share, well off its highs but still supported by strong demand for AI-optimized servers.

In recent weeks, Supermicro began volume shipments of its NVIDIA Blackwell Ultra systems and rack-scale AI solutions, giving customers pre-validated, plug-and-play infrastructure that can scale from a single rack to full data centers. These new systems are designed for cutting-edge workloads like multimodal AI, real-time reasoning, and advanced training.

Rapid revenue growth, a clean balance sheet, and surging infrastructure spending have fueled investor interest. But with margins still thin and competition from larger rivals intensifying, analysts appear divided on what comes next.

This article explores where Wall Street analysts think SMCI could trade by 2028. We have pulled together consensus targets, growth forecasts, and valuation models to get a sense of the stock’s possible trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

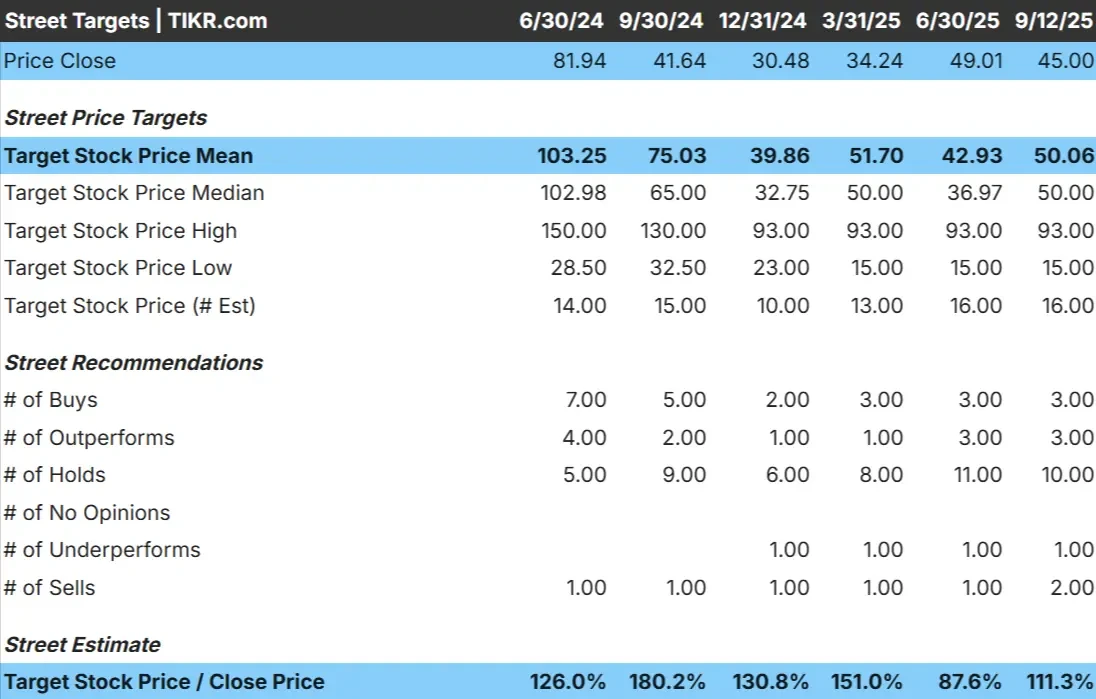

Analyst Price Targets Say SMCI Is Undervalued

SMCI trades at about $45/share today. The average analyst price target sits near $103/share, which suggests roughly +126% upside. Forecasts show a wide spread and reflect divided sentiment:

- High estimate: ~$150/share

- Low estimate: ~$29/share

- Median target: ~$103/share

- Ratings: mix of Buys, Holds, and a few Sells

It looks like analysts see potential for strong gains, but the wide range of targets suggests conviction is weak. For investors, the key point is that expectations are highly uncertain, and the stock may swing sharply depending on how AI server demand and execution unfold.

See analysts’ growth forecasts and price targets for SMCI (It’s free!) >>>

SMCI: Growth Outlook and Valuation

The company’s fundamentals still look solid, but not without risks:

- Revenue may grow about 30% annually over the next 2 years

- EBIT margin sits near 6%, leaving little room for cost pressures

- Shares trade at ~17x forward earnings, which looks reasonable but not cheap

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests ~$74/share by 2028

- That would imply ~64% upside, or about 19% annualized returns

These numbers suggest SMCI could keep compounding if AI infrastructure spending remains strong. For investors, the valuation looks fair relative to growth rather than deeply discounted. Upside likely depends on the company sustaining rapid revenue growth while also expanding profitability over time.

Value stocks like SMCI in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

SMCI has managed to capture strong growth as AI infrastructure demand accelerates. Orders for GPU-optimized servers are expanding quickly, creating a revenue stream that appears well-tied to one of the biggest technology themes of the decade. Global demand from hyperscalers and enterprises remains a key driver, with data center spending showing no signs of slowing in the near term.

On top of this, SMCI’s product flexibility looks like a competitive edge. The company can design and deliver customized server solutions at speed, which helps it win contracts against larger but slower-moving rivals. Combined with its clean balance sheet and history of rapid revenue growth, these factors help explain why bulls believe SMCI can maintain momentum in the AI hardware market.

These trends provide confidence that SMCI may continue to grow alongside AI adoption, supporting the idea that today’s valuation leaves room for upside if execution remains strong. For investors, this makes SMCI an attractive but still risky way to play the infrastructure side of AI growth.

Bear Case: Margins and Competition

Despite the positives, SMCI’s thin margins remain a concern. With EBIT margin near 6%, even modest cost increases or pricing pressure could weigh heavily on profits. Competition from larger players like Dell and HP is also fierce, as these companies are investing heavily to secure their share of the AI server market.

Another risk is that hardware cycles tend to be boom-and-bust. If demand cools after the current wave of AI investment, SMCI’s earnings could fall sharply. Since analyst targets already assume healthy execution, any stumble in growth or profitability could lead to a re-rating.

The bear case is that SMCI’s valuation reflects high expectations, but its fundamentals leave little room for error. For investors, this means SMCI could deliver far weaker returns than the bullish narrative implies if demand proves less durable or competition eats into margins.

Outlook for 2028: What Could SMCI Be Worth?

Based on current forecasts, SMCI could trade in the $74/share range by 2028. That would represent about 64% upside, or roughly 19.2% annualized returns. The scenario assumes continued double-digit revenue growth and steady demand for AI-driven infrastructure.

While this would represent strong performance, the outlook already builds in a fair amount of optimism. To deliver returns at the higher end of the range, SMCI may need to outperform on margins, win share from larger competitors, or sustain demand longer than many expect. Without that, gains could be more modest.

For investors, SMCI looks like a potential long-term compounder in AI hardware, but the path to outsized returns may depend on the company exceeding today’s already ambitious expectations.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.