Advanced Micro Devices (NASDAQ: AMD) has become one of the most closely watched names in semiconductors. Known for its CPUs, GPUs, and growing role in AI, AMD trades at about $159 today, off its 52-week high of $187 but well above the lows from early 2023.

The company has recently surged deeper into AI, unveiling its upcoming Instinct MI450 GPU, launching a new “MegaPod” supercluster design, and striking partnerships in areas like AI-powered drug discovery.

This article reviews where Wall Street analysts think AMD could trade by 2027. We have compiled consensus targets, valuation assumptions, and recent price action to outline the stock’s possible trajectory. These figures reflect current analyst models and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Solid Upside

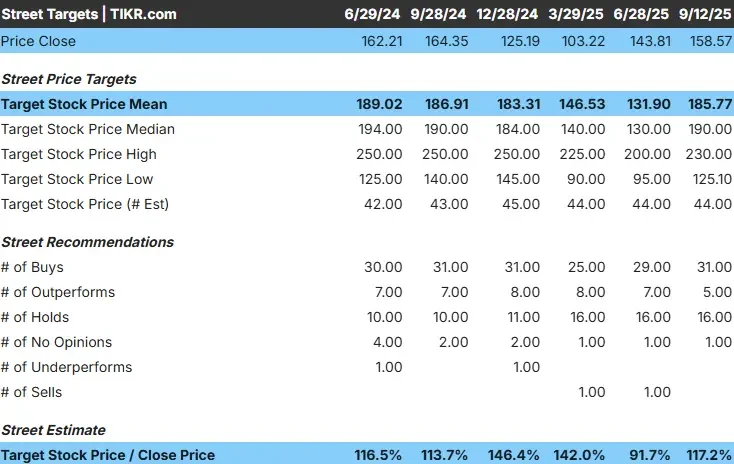

AMD trades at about $159/share today. The average 12-month analyst price target sits near $186, which points to roughly 17% upside. Forecasts cover a wide range and show how divided sentiment is among analysts:

- High estimate: ~$250/share

- Low estimate: ~$125/share

- Average target: ~$186/share

- Ratings: 31 buys, 7 outperforms, 16 holds, 2 sells

It looks like most analysts lean bullish, with optimistic views tied to AI-driven demand, while cautious analysts highlight competition and valuation risk.

The takeaway is that upside exists, but expectations vary sharply. AMD may need to consistently deliver on AI growth and margins to justify a move closer to the higher end of targets.

See analysts’ growth forecasts and price targets for AMD (It’s free!) >>>

AMD: Growth Outlook and Valuation

Fundamentals look strong on paper, with analysts modeling significant revenue growth and margin expansion over the next few years:

- Revenue forecast: ~22% annual growth through 2027

- Operating margins: expected to climb toward ~27% from ~8% today

- Current valuation: ~31x forward earnings

- Guided valuation model: Based on analysts’ average estimates, TIKR’s model using a 29x forward P/E suggests ~$244/share by 2027

- Implied upside: ~54% total, or ~20% annualized returns

These forecasts show AMD has the potential to be a strong compounder if execution is on track. But at a premium multiple, much of the optimism may already be baked in, leaving limited room for error.

The setup appears attractive for those willing to handle volatility, though upside depends heavily on hitting growth and margin targets.

Value stocks like AMD in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

AI chip demand in data centers and PCs is growing rapidly, and AMD is well-positioned to benefit from this secular trend. The company also appears to be expanding partnerships with hyperscalers, which could strengthen its role as a key alternative to NVIDIA in the AI compute market.

Gross margins remain around 51%, giving AMD flexibility to reinvest in research and development. The balance sheet also looks strong, with a net cash position of about $2B, allowing the company to keep investing in growth without being weighed down by debt.

Optimism stems from AMD’s chance to win meaningful market share in AI while maintaining a solid financial foundation. If these drivers hold up, the company could justify its valuation and potentially deliver upside surprises.

Bear Case: Risks to Watch

Competition from NVIDIA, Intel, and new chip entrants remains fierce, making it difficult for AMD to sustain growth without constant innovation. Valuation at ~31x earnings also looks demanding if revenue growth slows or if hyperscaler spending turns out weaker than expected.

The low-end analyst target of $125 shows that some see meaningful downside risk, particularly if execution falters. With a 5-year beta near 2.0, AMD’s stock is also far more volatile than the broader market, which could make it a bumpy ride for investors.

The bear case is that too much optimism is already priced in. If AI adoption cools or AMD fails to keep pace with competitors, the stock could fall quickly. High volatility means timing matters, and patient investors may need to withstand sharp drawdowns.

Outlook for 2027: What Could AMD Be Worth?

Based on analysts’ average estimates, AMD may reach about $244/share by 2027. That would represent ~54% total upside, translating into roughly 20% annual returns if growth and margin expansion play out as expected.

AMD looks like a high-reward but high-risk opportunity. Those confident in the AI story and AMD’s ability to execute may benefit from strong long-term gains. However, the stock carries meaningful downside if expectations prove too optimistic, making it best suited for investors comfortable with volatility.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.