Restaurant chains with strong unit economics can be some of the most resilient companies in the consumer sector. Restaurant franchises that generate high returns on capital, benefit from insurer coverage, and scale across markets attract both domestic and global investors.

In a thin-margin industry, these operators stand out for disciplined execution, growth via expansion and franchising, and steady cash flows. With global demand for branded dining concepts rising, top restaurant stocks with best-in-class economics are well-positioned to deliver lasting returns.

Here are 10 leading names with strong economics, institutional coverage, and national + global growth potential.

| Company Name (Ticker) | Analyst Upside | P/E Ratio |

| Chipotle (CMG) | 37.4% | 32.40 |

| McDonald’s (MCD) | 7.1% | 24.18 |

| Wingstop (WING) | 18.1% | 75.64 |

| Texas Roadhouse (TXRH) | 14.3% | 24.50 |

| Darden Restaurants (DRI) | 12.6% | 19.33 |

| Domino’s (DPZ) | 13.4% | 24.52 |

| CAVA (CAVA) | 35.2% | 113.38 |

| Yum! Brands, Inc. (YUM) | 9.0% | 23.43 |

| Restaurant Brands International (QSR) | 21.0% | 16.30 |

| Jack in the Box (JACK) | 23.0% | 4.23 |

Unlock our Free Report: 5 undervalued compounders with upside based on Wall Street’s growth estimates that could deliver market-beating returns (Sign up for TIKR, it’s free) >>>

Here are 3 restaurant stocks that might be worth a closer look today:

Chipotle (CMG)

Chipotle’s unit economics are powered by very high throughput per restaurant and its growing footprint of drive-thrus (Chipotlanes) plus strong digital sales. In late 2024, digital channels made up ~34.4% of Chipotle’s food & beverage revenue (Q4) and restaurant-level operating margin for FY 2024 was ~26.7%.

While average unit volumes (AUVs) have surpassed $3 million in many markets, management has publicly stated a goal of pushing AUVs toward $4 million through drive-thru expansion, loyalty, and marketing.

Chipotlane drive-thrus and kitchen automation raise per-store capacity at relatively modest incremental variable cost, so incremental sales flow very quickly to the operating line.

Management’s drive to push AUVs toward $4M (by expanding Chipotlanes and advertising/loyalty) is the natural next lever; if they hit those targets, it materially widens four-wall margins and shortens payback on new openings, which explains why investors treat unit economics as the core valuation argument.

Value any stock in under 30 seconds with TIKR’s new Valuation Model (it’s free) >>>

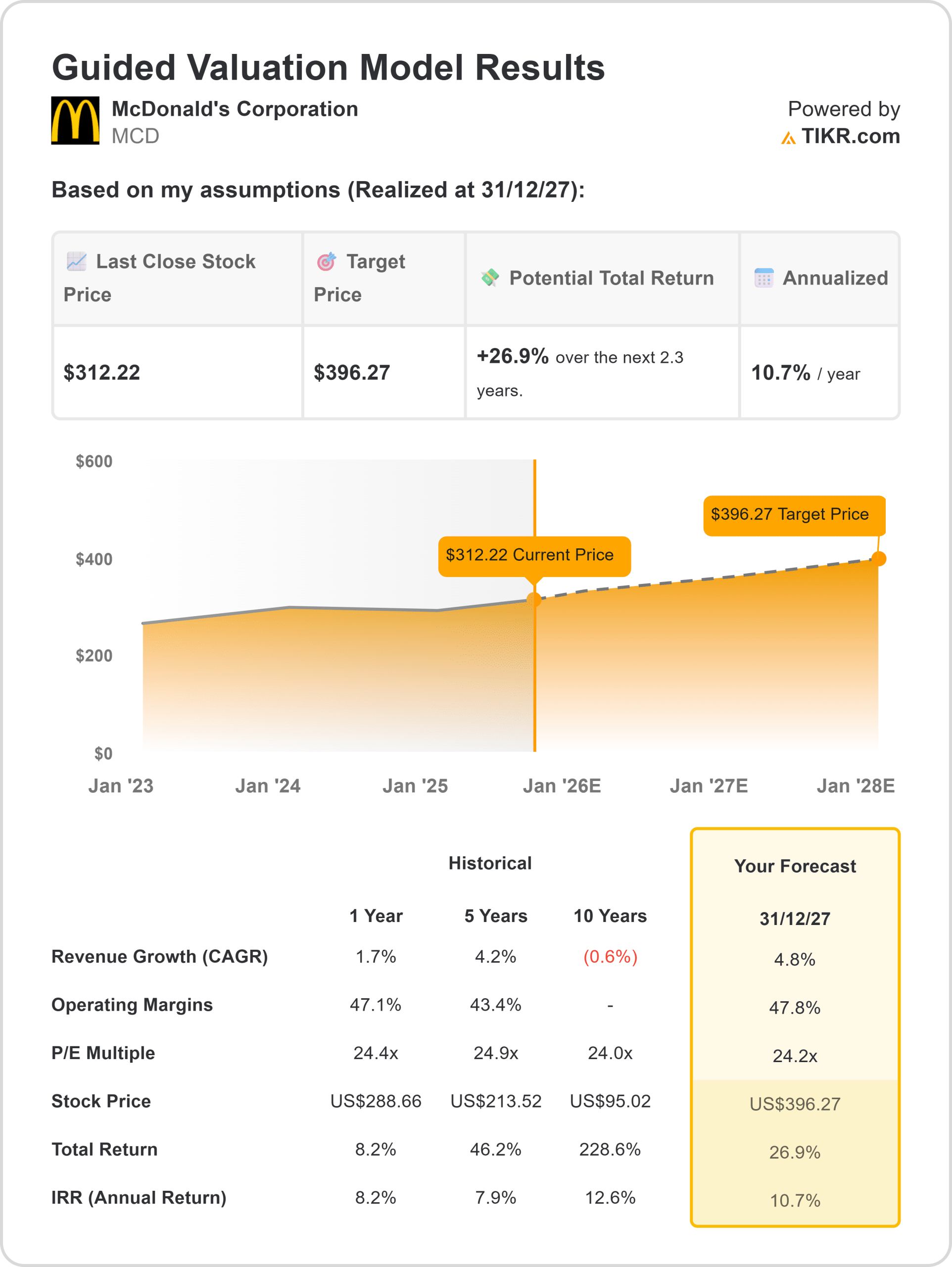

McDonald’s (MCD)

McDonald’s is an almost textbook example of durable, high-quality unit economics, primarily because the system is overwhelmingly franchised (95% of restaurants), and average unit volumes are well above most competitors (McDonald’s cites an AUV figure of roughly $5.5M as of year-end 2024).

That scale and franchise mix converts store sales into recurring rent/royalty cash flows for the company while leaving franchisees to capture real unit-level profits, which in turn sustains steady reinvestment in real estate, drive-thru re-images, and digital capabilities.

The company’s investor materials also highlight the operational levers (drive-thru penetration, loyalty, delivery integrations) that protect and grow AUV over time.

From an investor’s lens, McDonald’s unit economics are attractive for two independent reasons: the franchisee level AUVs, drive-thru productivity, menu engineering produces attractive cash-on-cash returns across most developed markets, and at the corporate level, the asset-light royalty/rent model delivers very high free-cash conversion and predictable margins that scale as system sales grow.

Put plainly, you get best-in-class per-store economics without the company shouldering all the capex, and that combination is rare in restaurant land.

Find stocks that we like even better than McDonald’s today with TIKR (It’s free) >>>

Texas Roadhouse (TXRH)

Texas Roadhouse is unusual among casual-dining chains because its per-unit sales look more like premium casual than legacy family dining in 2024, the company reported systemwide revenue near $5.4B and average unit volume that exceeded $8M for the first time.

Those very high AUVs translate into meaningful restaurant margin dollars. The company reported materially higher restaurant-margin dollars in 2024 and average weekly sales in the mid-$150k range for comparable restaurants, which gives each new build a large dollar cushion to cover fixed costs and deliver fast economic payback in healthy markets.

Texas Roadhouse combines consistently strong traffic and higher checks with relatively disciplined unit economics (their disclosed average capital investment for new restaurants is in the neighborhood of $8.6M), so the math at full occupancy is compelling and high AUVs × reasonable restaurant margins versus a known capex baseline creates attractive long-run returns per restaurant.

In short, Texas Roadhouse’s AUVs and restaurant margins are the structural reasons it sits comfortably in a “strong unit economics” list alongside the quick-service giants.

Value stocks like Texas Roadhouse quicker with TIKR >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!