Key Stats for Spx Technologies Stock

- 52-Week Range: $130 to $247

- Current Price: $223

- Street Mean Target: $258

- Street High Target: $280

- Analyst Consensus: 10 Buys, 1 Outperform, 1 Hold, 0 Sells

- TIKR Model Target (Dec. 2030): $263

What Happened?

SPX Technologies (SPXC) is a Charlotte-based industrial company that makes highly engineered heating, cooling, and detection systems for data centers, hospitals, airports, and defense customers worldwide.

The company closed out fiscal 2025 with revenue of $2.265 billion, up 14.2% year-over-year, and full-year adjusted EPS of $6.76, which came in near the upper end of its guidance range of $6.65 to $6.80.

Q4 alone told a sharper story: revenue hit $637.30 million, up 19.4% year-over-year and above the Street’s estimate of $625.98 million, while adjusted EPS of $1.88 narrowly beat the $1.87 consensus.

The quarter was driven by two segment engines firing together: HVAC revenue grew 16.4%, fueled by both organic volume growth of 10.3% and the contribution of the Sigma & Omega acquisition, while Detection & Measurement revenue surged 26.3%, with KTS accounting for 23.2% of that gain.

SPX Technologies stock’s next leg of the story is built on data centers.

CEO Gene Lowe said on the Q4 earnings call: “We have a winner here,” referring to OlympusMAX, the company’s new large-tonnage cooling tower designed for hyperscale data center deployments, which hit its $50 million bookings target in 2025 and is already converting to revenue in 2026.

Data center revenue ran at roughly 9% of total sales in 2025, translating to around $200 million, up from approximately 7% the prior year, and management guided that figure to reach around 12% of revenue in 2026, implying roughly 50% growth in that segment alone.

To support that demand, SPX is deploying approximately $100 million in capital expenditures across HVAC facilities in 2026, on top of $60 million invested in 2025, targeting roughly $700 million of incremental production capacity once its new Alabama and Tennessee plants reach full output.

Two acquisitions completed in Q1 2026 extend the platform further: Thermolec, a Canadian electric duct heating leader, and Air Enterprises plus Rahn Industries, the former air-handling segment of Crawford United, acquired for approximately $300 million.

Management guided 2026 revenue to a range of $2.535 billion to $2.605 billion and adjusted EBITDA to $590 million to $620 million, implying around 20% EBITDA growth at the midpoint and putting adjusted EPS in a range of $7.60 to $8.00.

Wall Street’s Take on SPXC Stock

The Q4 beat confirms that SPX Technologies stock’s HVAC backlog is not speculative — it is locked, growing organically at double digits, and about to get bigger.

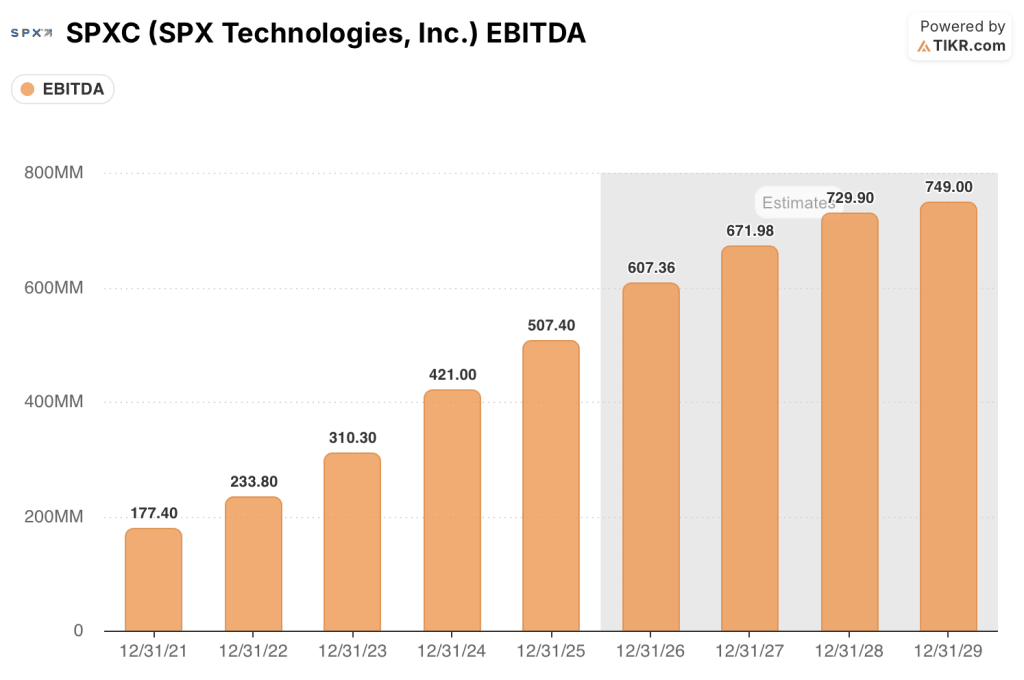

SPXC’s adjusted EBITDA grew 20.5% to $507.4 million in fiscal 2025, and consensus now projects that figure reaching $607 million in 2026 (around 20% growth) and around $670 million in 2027 (around 10% growth), reflecting the Street’s confidence in the first phase of the capacity ramp while pricing in a natural deceleration as the 2026 tailwinds from acquisitions and new capacity fade.

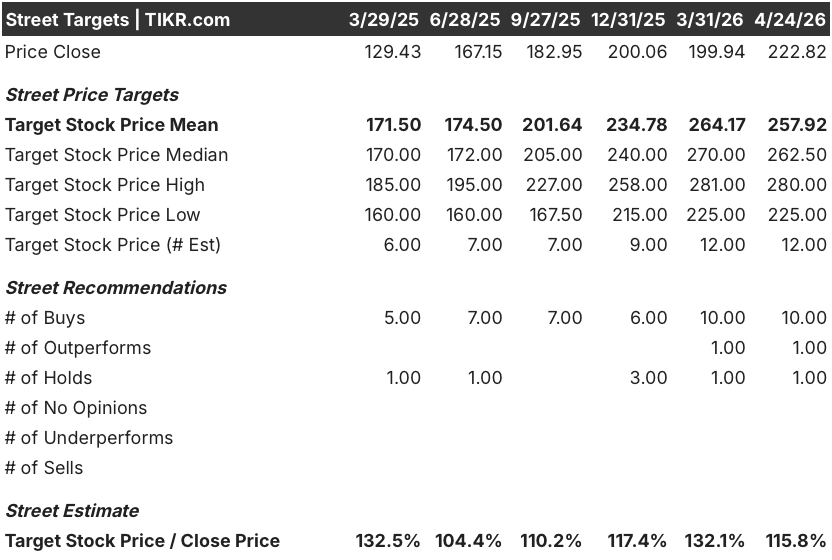

Ten of the 12 analysts covering SPX Technologies stock have buy-equivalent ratings, with a mean price target of $258 against a current price of $223, implying roughly 16% upside; what the Street is specifically waiting for is evidence that the Madison, Alabama facility begins assembly in the second half of 2026 on schedule, since that facility underpins management’s confidence in sustaining data center revenue growth into 2027 and 2028.

The target spread, from $225 on the low end to $280 at the high, maps almost exactly onto the two competing views on capacity execution: bears anchored near $225 are pricing in start-up friction and a softening non-data-center HVAC mix, while bulls at $280 are underwriting smooth ramp-up at both new facilities and continued hyperscaler demand lock-ins similar to the multi-year commitment Lowe described on the earnings call.

Trading at roughly 28x forward EBITDA against a 5-year historical average closer to 20x, SPX Technologies stock appears fairly valued at current levels given that the 2026 EBITDA growth catalyst is well-understood by the Street and much of the $700 million capacity expansion is already in guidance, leaving limited re-rating potential until the 2027 and 2028 revenue from those facilities becomes visible.

Management’s signal that one hyperscaler has already locked up multiple years of growing OlympusMAX demand confirms the backlog is durable, but it is now the market’s base case, not a surprise.

The risk is tariff-driven cost pressure on steel and aluminum, which CFO Mark Carano acknowledged as a watch item given that HVAC manufacturing is materials-intensive even with largely domestic sourcing.

The catalyst is Q1 2026 earnings on April 30, where investors will watch for data center bookings growth beyond the $50 million 2025 baseline and any update on the TAMCO Tennessee facility, which is expected to reach initial production by the end of Q1.

What Does the Valuation Model Say?

The TIKR model assigns a mid-case target price of $263 to SPX Technologies stock, anchored on a forward EPS CAGR of around 6% through 2030, a net income margin expanding to approximately 16%, and an annual P/E compression of around 1% as the multiple normalizes from its current elevated level.

That mid-case target implies 18% total return over roughly 4.7 years, or about 3.6% annualized — and at a growth rate already well-understood by the Street, SPX Technologies stock appears fairly valued near its current price, with the upside requiring patient compounding rather than a near-term re-rating catalyst.

The investment case for SPXC hinges on a single question: does the $700 million capacity expansion translate into sustained 15%+ EBITDA growth past 2026, or does growth decelerate faster than the market expects once the acquisition tailwinds and facility ramp roll off?

What Has to Go Right

- Data center revenue reaches around 12% of total sales in 2026 (roughly $312 million at guidance midpoint), confirming the 50% growth pace management outlined

- The Madison, Alabama facility achieves initial assembly in the second half of 2026 and enters production by early 2027, maintaining the $700 million incremental capacity timeline

- Adjusted EBITDA margins hold in the 23% to 24% range through 2026 despite approximately 50 basis points of temporary start-up costs from new plant ramp-ups

- Detection & Measurement segment delivers mid-single-digit organic growth ex the $20 million project pull-forward, supported by record year-end backlog of $350 million (up 43% organically year-over-year)

What Could Go Wrong

- HVAC margins compress further than the guided 50 basis points from start-up costs if facility ramp-ups in Alabama and Tennessee encounter equipment delivery delays or production friction

- Non-data center HVAC end markets (battery, automotive, semiconductor, commercial real estate) remain soft, leaving the segment exposed to a narrow set of growth drivers

- The TIKR model’s 1.3% annual P/E compression assumption accelerates if the broader industrial sector de-rates, squeezing the return profile even if earnings compound as expected

- Tariff pressure on steel and aluminum raises input costs across the HVAC segment, where configured-to-order manufacturing limits the company’s ability to pre-hedge materials exposure

Should You Invest in SPX Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SPXC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SPX Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SPXC stock on TIKR for Free →