Key Stats for SPX Technologies Stock

- 52-Week Range: $151 to $247

- Current Price: $217

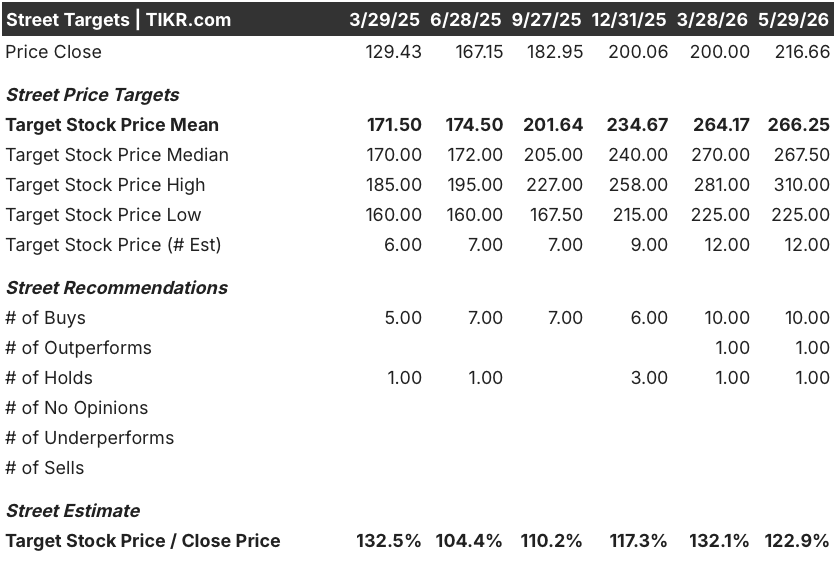

- Street Mean Target: $266

- Street High Target: $310

- Analyst Consensus: 10 Buys / 1 Outperform / 1 Hold

- TIKR Model Target (Dec. 2030): $285

SPX Technologies Stock Beats Q1 Estimates and Raises Guidance as Data Center Backlog Surges 38%

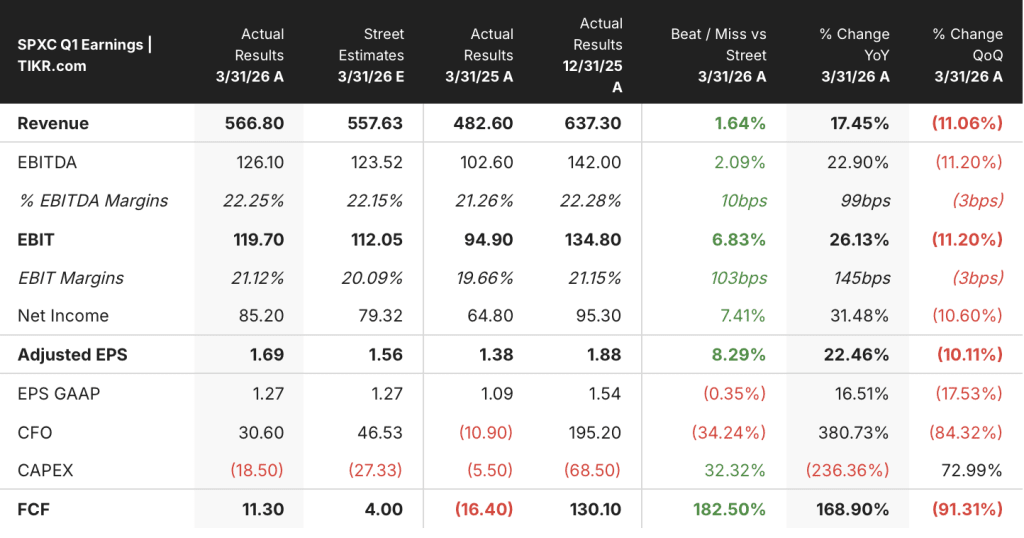

SPX Technologies (SPXC), an engineered infrastructure equipment company supplying cooling towers, custom air handlers, and detection systems across industrial and data center markets, reported Q1 2026 results on April 30 that beat estimates across every major metric and prompted a guidance raise for the full year.

Revenue of $566.8 million topped the $557.6 million consensus estimate by around 2% and grew 17.4% year over year.

Adjusted EBITDA of $126.1 million beat the $123.5 million estimate and expanded 22.9% year over year, with EBITDA margins of 22.25% running about 10 basis points ahead of the street’s 22.15% estimate.

Adjusted EPS of $1.69 beat the $1.56 consensus by $0.13, a beat of around 8%, and grew 22.5% year over year.

The HVAC segment, which generates roughly two-thirds of total company revenue through cooling towers, boilers, electric duct heating, and custom air handling products, grew revenue by 22% year over year to around $394 million, driven by both acquisition contributions and organic volume.

What makes the quarter notable is not the headline beat. It is the backlog.

HVAC segment backlog at quarter end was $755 million, up 38% organically year over year, with the acceleration driven almost entirely by data center demand.

CEO Gene Lowe provided the operational context on the Q1 2026 earnings call: “The demand is extremely strong. At our last quarterly update, we guided that to $350 million. We’re really focusing on expanding our capacity, and we’re making great progress there.”

The Detection and Measurement segment, which provides underground pipe locators, robotic inspection systems, transportation platforms, and drone detection and communications technology, grew revenue 8.3% year over year, with segment margin expanding 410 basis points, driven by favorable software mix in the transportation business.

Management raised full-year adjusted EPS guidance by $0.15 at the midpoint to a range of $7.80 to $8.10, citing Q1 outperformance and additional data center volume expected in the second half.

The company disclosed an approximately $10 million gross tariff headwind from Section 232 changes affecting Canadian manufacturing operations, expecting to offset around half through price and other levers, with the impact concentrated in Q2 and no carryover into 2027.

At the Bank of America Industrials conference, Lowe framed the data center positioning in concrete revenue terms: “If you look at data centers, it’s a very material portion of our business. In 2024 we had approximately $150 million of data center revenue. 2025, it was $200 million. This year, we guided for $300 million. Our demand is extremely strong. At our last quarterly update, we guided that to $350 million.”

Is SPX Technologies Stock Undervalued? What the Street Says After Q1

Wall Street’s reaction to the Q1 beat was broadly positive. After the results, multiple analysts raised price targets: JPMorgan moved to $270 from $260, Truist moved to $261 from $251, and B. Riley moved to $280 from $270.

The street mean target now stands at around $266 against a current price of around $217, implying upside of roughly 23% at consensus. The street high target sits at around $310, representing roughly 43% upside from current levels.

Coverage is heavily skewed toward Buy. Of 12 analysts with ratings, 10 have Buy recommendations, 1 has Outperform, and 1 has Hold, with no Sells or Underperforms.

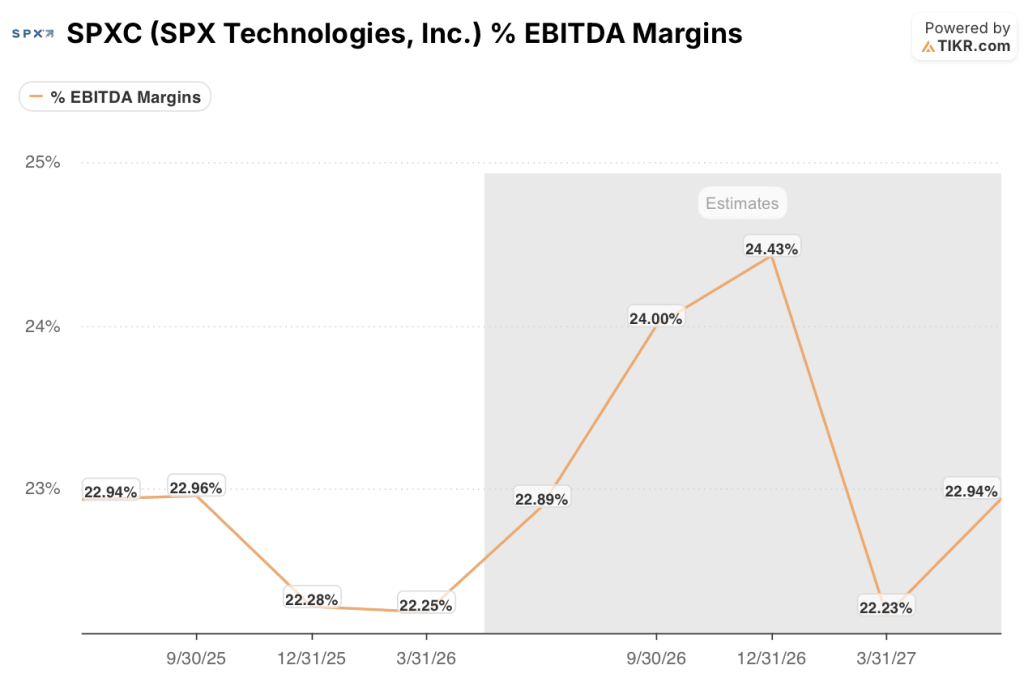

The forward estimate trajectory frames the size of the opportunity. Consensus sees full-year 2026 revenue at the midpoint of management’s guidance range, with EBITDA margins in the 22% to 24% range across the next several quarters.

That margin profile matters because the HVAC capacity build is the central tension in SPXC stock right now. Management acknowledged start-up costs of around $8 million to $9 million concentrated in H1, primarily suppressing HVAC segment margin by approximately 40 basis points in Q1 relative to what operating leverage alone would have produced. Those costs roll off. The capacity they fund does not.

The question on the street is not whether data center demand is real. At 70% year-over-year growth in Q1 and a backlog up 38% organically, that debate is closed. The question is how quickly the three-facility expansion program in Olathe, Kansas; Tennessee; and Madison, Alabama transitions from cost to contribution.

CFO Mark Carano even addressed this directly on the earnings call: “I’m very confident in our ability to deliver our traditional incremental margins in the HVAC business, particularly through the back half of the year and as we get into next year.”

Is SPXC Stock Undervalued in 2026? TIKR’s $285 Mid-Case Says Yes

TIKR’s base case values SPX Technologies at approximately $285 by December 2030, implying around 32% total return from the current price of around $217, or roughly 6% annualized over approximately 4 and a half years.

The low case, anchored to roughly 6% revenue CAGR and around 15% net income margins, produces a stock price of approximately $269 and around 2% annualized return, a scenario where growth slows but the business continues compounding at a modest rate.

The mid case assumes roughly 7% revenue CAGR and around 16% net income margins, with the price forecast chart showing approximately $342 at December 2034, with around 5% annualized return, consistent with the data center capacity expansion delivering on its stated trajectory without further acceleration.

The high case, built on roughly 8% revenue CAGR and around 17% net income margins, points to approximately $423 and around 8% annualized return, a scenario where hyperscaler demand continues accelerating beyond the current capacity ceiling and SPX continues deploying capital at the same discipline that has averaged around 9x EBITDA after synergies across 18 prior acquisitions.

SPXC appears to be undervalued at current levels.

The street mean target alone implies roughly 23% upside, and the TIKR model’s mid-case points to roughly 32% total return over the holding period. The market appears to be treating the capacity build as structural margin compression when the financial profile of those facilities, with management citing payback periods of under two years, says the opposite.

Is SPX Technologies Stock a Buy Right Now?

The current analyst consensus is strongly bullish: 10 of 12 analysts hold Buy ratings on SPXC, with a mean price target of around $266 against a current price of around $217, implying roughly 23% upside.

The TIKR model’s mid-case points to approximately $285 by December 2030, implying roughly 32% total return.

The key variable to watch is the pace at which the HVAC facility expansion in Kansas, Tennessee, and Alabama transitions from a cost headwind to a margin contributor as start-up costs roll off in the second half.

Should You Invest in SPX Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SPX Technologies, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SPX Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SPX stock on TIKR for Free →