Key Stats for Coinbase Stock

- 52-Week Range: $139 to $445

- Current Price: $189

- Street Mean Target: $232

- Street High Target: $400

- Analyst Consensus: 18 Buys / 3 Outperforms / 10 Holds

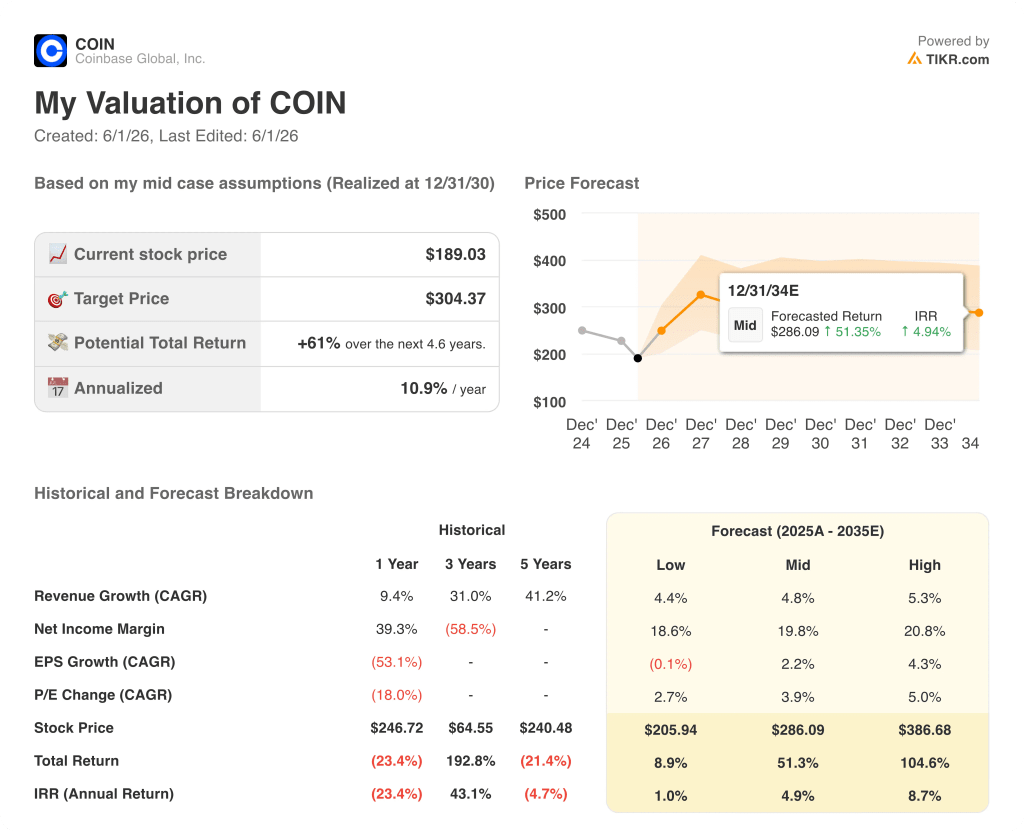

- TIKR Model Target (Dec. 2030): $304

Coinbase Stock Posts Two Consecutive Losses as Market Share Hits an All-Time High

Coinbase Global (COIN) reported a Q1 2026 net loss of $394.1 million, or $1.49 per share, following a second consecutive quarter of losses as crypto trading volumes fell more than 20% quarter-over-quarter alongside the broader digital asset market.

The headline loss is real. What it obscures is equally real.

Total crypto market cap and total spot trading volume both declined sharply in the quarter as macro uncertainty, rising Middle East tensions and fading post-October momentum drove investors into safe-haven assets. Coinbase’s transaction revenue fell to $756 million, down roughly 40% from the prior year. Total revenue came in at $1.43 billion, down 21% quarter-over-quarter.

But Coinbase gained global crypto trading market share during that same quarter and hit a new all-time high. The company has now posted 12 consecutive quarters of net native unit inflows, meaning customers kept adding assets even as prices dropped. When conditions deteriorate, customers consolidate to platforms they trust. That is a competitive moat expressing itself in the worst quarter for the industry this cycle.

CFO Alesia Haas framed the quarter directly on the Q1 2026 earnings call: “Total crypto market cap and total crypto trading volume were both down more than 20% quarter-over-quarter. And volatility in the long tail assets was at historic lows.”

While spot trading suffered, two newer businesses moved in the opposite direction. Retail derivatives reached an annualized revenue run rate exceeding $200 million in Q1. Prediction markets, launched just two months before the quarter ended, hit $100 million in annualized revenue in March alone. Non-crypto contracts including silver, gold, and oil grew more than 4x quarter-over-quarter in volume. These businesses were not material 12 months ago. They are now structurally embedded in the revenue mix.

Coinbase cut approximately 700 jobs, or about 14% of its global workforce, in early May, incurring an expected $50 million to $60 million in restructuring charges. CEO Brian Armstrong cited both the subdued trading environment and a deliberate transition to AI-native operations. The number of pull requests per engineer rose roughly 78% year-over-year. The company’s full-year 2026 adjusted expense outlook came in at $4.3 billion to $4.6 billion, approximately $500 million lower than the annualized Q4 2025 exit rate.

On the regulatory front, Chief Legal Officer Paul Grewal stated on the earnings call that the CLARITY Act is on track for markup this month with a floor vote in early summer, adding: “All that translates to our confidence that we’re going to see a signed piece of legislation by the end of the summer.” CLARITY is the market structure bill that would establish clear regulatory definitions for digital assets across the entire U.S. crypto industry. It is the catalyst that would unlock institutional product buildout Coinbase has been positioning for since 2021.

The company ended Q1 with over $10 billion in cash and equivalents and around $12 billion in total available resources. It repurchased approximately 6 million shares for around $1.1 billion during the quarter.

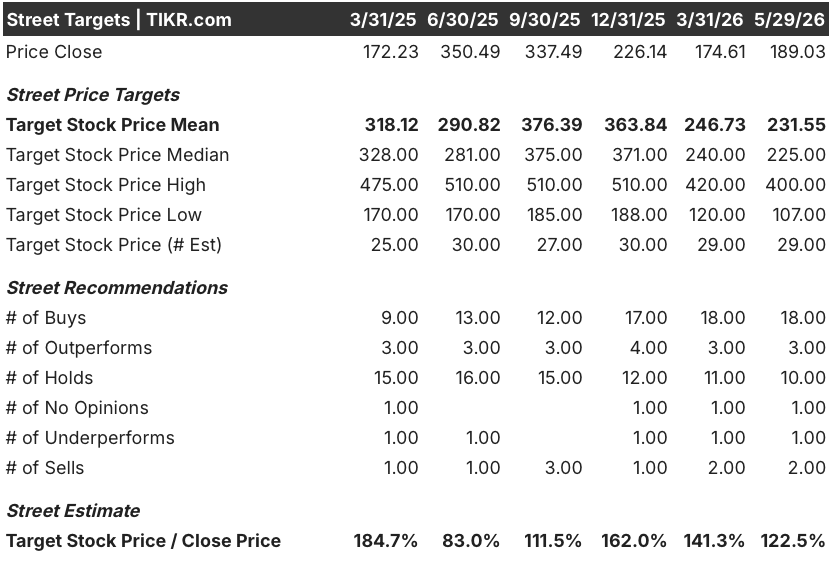

What Analysts Think About Coinbase Stock: Mean Target at $232, High at $400

Coinbase stock carries 18 Buy ratings, 3 Outperforms, and 10 Holds among the 31 analysts currently covering the name, with 3 Sell or equivalent ratings in the mix. The mean target is around $232 against a current price of $189, implying roughly 23% upside. The Street high sits at $400, more than double current levels.

The buy-side thesis is a cycle thesis with a platform twist. J.P. Morgan raised its price target to $290 following Q1 earnings, citing platform expansion and derivatives momentum. The base case does not require a crypto bull market to work; it requires the non-trading revenue base to hold and the new asset classes to continue gaining traction.

Subscription and services revenue, which includes stablecoin revenue, blockchain rewards, interest income, and Coinbase One subscriptions, came in at $584 million in Q1. That is now 44% of net revenue, up from a much smaller fraction two years ago. Average USDC held in Coinbase products reached a new all-time high of $19 billion during the quarter. Coinbase captures around 50% of all USDC economics. USDC supply has doubled over the past two years, and USDC’s share of total stablecoin supply is growing.

Coinbase One crossed 1 million paid subscribers during Q1. These are the highest-engagement customers on the platform, generating incrementally higher trading volume and revenue than standard retail users.

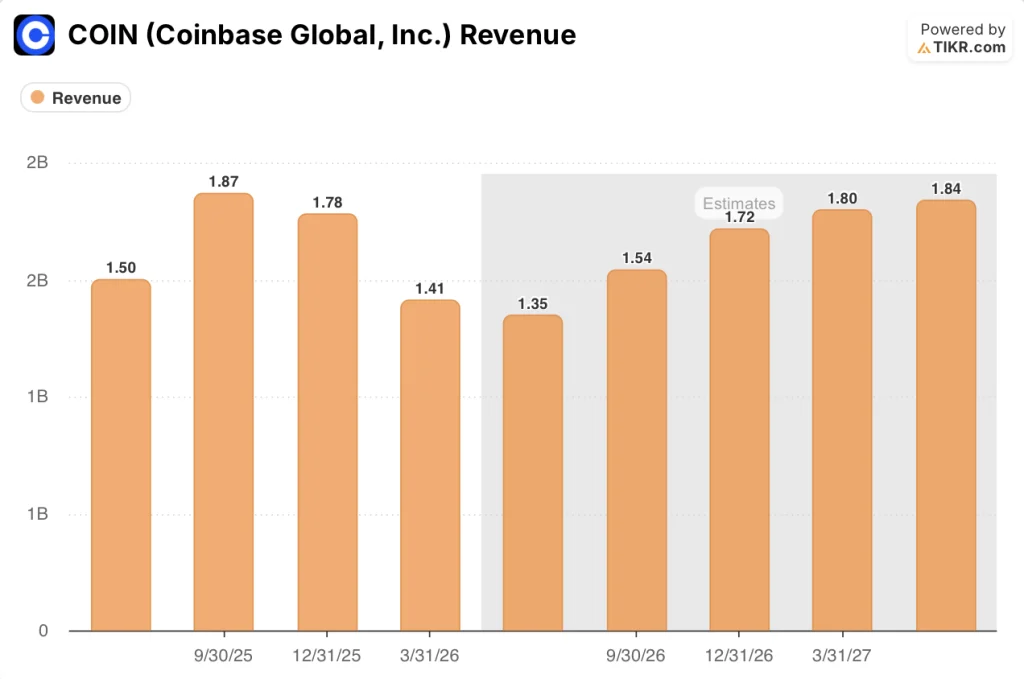

The risk is straightforward: Coinbase’s transaction revenue remains deeply tied to crypto market conditions. Q1 demonstrated how quickly the trading line can move when sentiment shifts. If crypto markets remain subdued through H2 2026, the Q2 guidance of $565 million to $645 million in subscription and services revenue, combined with early-quarter transaction revenue of $215 million through May 5, would pressure full-year adjusted EBITDA. Forward consensus estimates reflect that possibility, with revenue projected at around $1.35 billion for Q2 2026 before recovering to around $1.54 billion in Q3 and around $1.72 billion in Q4.

The structural picture behind the concern is where the disconnect with the stock price becomes visible. Coinbase has posted 13 consecutive quarters of positive adjusted EBITDA across bull markets, bear markets, and regulatory battles. The business did not break in Q1. It generated $303 million in adjusted EBITDA on revenue that was down 30% year-over-year. That is operational durability the current valuation is not fully pricing in.

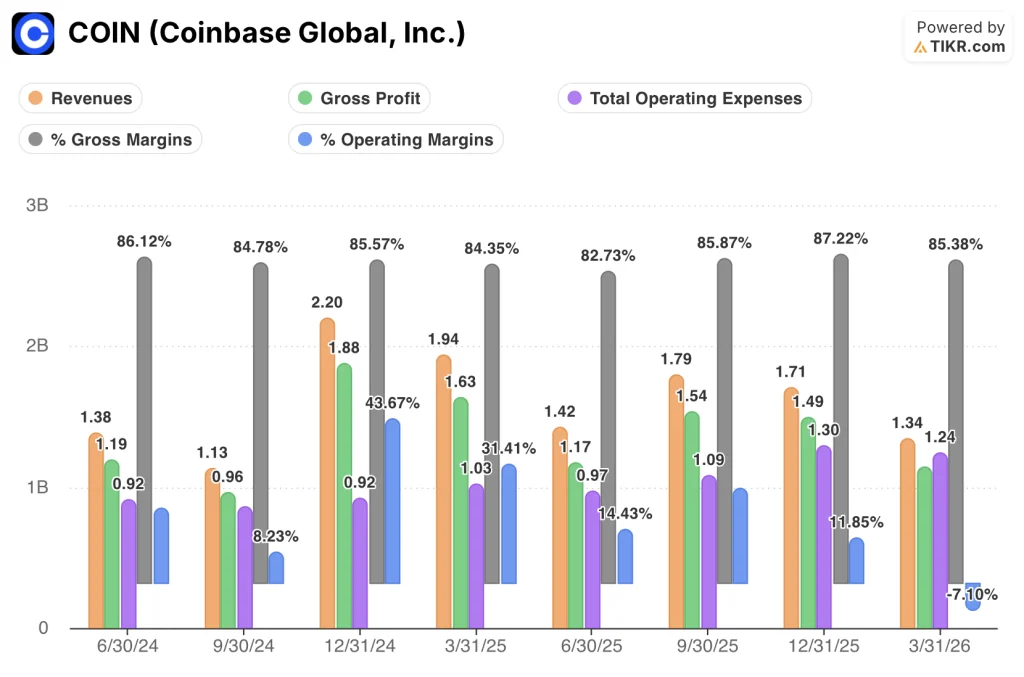

Coinbase Stock Financials: Revenue Down 31%, Gross Margins Hold at 85%

Coinbase’s Q1 2026 income statement shows a business absorbing a severe revenue cycle without structural margin deterioration, which is the most important thing the data reveals.

Revenue of $1.34 billion was down 30.8% year-over-year, extending the decline from 22.2% in Q3 2025 and accelerating as crypto markets sold off into 2026.

Gross profit of $1.14 billion came in at an 85.4% gross margin, down from 87.2% in Q4 2025 but within the 84% to 87% band that has held across eight consecutive quarters of widely varying revenue levels.

Total operating expenses of $1.24 billion drove an operating loss of $0.10 billion, pushing operating margins to negative 7.1%, the first negative operating margin quarter in this data set.

The operating margin contraction is the number to watch: eight quarters ago, when revenue was at a comparable $1.13 billion, operating income was $0.09 billion and operating margins were 8.2%. In Q1 2026 at $1.34 billion in revenue, those same margins went negative. The difference is the cost base. SG&A and R&D combined to $1.17 billion in Q1 2026, up from $0.88 billion in the September 2024 quarter when revenue was $1.13 billion. The restructuring announced in May is a direct response to that expansion.

Is Coinbase Stock Undervalued in 2026? TIKR’s $304 Model Says the Cycle Discount Is the Opportunity

TIKR’s base case values Coinbase at approximately $304 by December 2030, implying around 61% total return from the current price of $189, or roughly 11% annualized over approximately 4.6 years.

The low case produces a stock price of around $206 and a total return of around 9%, an annualized IRR of roughly 1%. This scenario reflects continued crypto market headwinds and revenue growth of around 4% annually, with net income margins recovering to around 19%.

The mid case targets around $286, implying roughly 51% total return and an annualized IRR of approximately 5%. Revenue growth of around 5% annually and expanding net income margins drive the outcome.

The high case values Coinbase stock at around $387, more than double the current price, representing around 105% total return and an annualized IRR of approximately 9%. This requires the full CLARITY unlock to convert into institutional product revenue, the derivatives platform to continue scaling, and the stablecoin and agentic commerce flywheel to compound.

COIN is undervalued at current levels. The stock is priced for a business where the trading downturn is permanent. The data — 13 straight quarters of positive adjusted EBITDA, $19 billion of USDC on platform, derivatives scaling to $200 million annualized, CLARITY approaching a floor vote — describes a business where the downturn is temporary and the platform expansion is not.

Is Coinbase stock a buy right now?

The analyst consensus is 18 Buys against 10 Holds and 3 Sells, with a mean price target of around $232, implying roughly 23% upside from the current price of $189.

The structural case centers on 13 consecutive quarters of positive adjusted EBITDA, $19 billion of USDC on platform, and derivatives revenue crossing $200 million annualized.

The key variable is timing: a CLARITY Act signature by end of summer would be the most significant near-term catalyst.

Should You Invest in Coinbase Global, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Coinbase Global stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Coinbase Global alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze COIN stock on TIKR for Free →