Key Takeaways:

- Strategic Pivot: Repsol (REP) is balancing its legacy oil business with a massive push into renewable energy, aiming for 9-10 gigawatts of low-carbon capacity by 2027.

- Price Projection: Despite the transformation, our model suggests the stock may only reach €16 per share by December 2027.

- Expected Returns: This target implies a meager 2.1% annualized return, suggesting the stock could be “dead money” for growth investors despite its high yield.

- The Income Play: While the dividend is set to rise to €1.05 per share, shrinking revenues and valuation compression could cap total returns.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Sacyr (SCYR) is no longer a construction company; it is an infrastructure machine.

The Spanish group has spent years rotating assets to focus on P3 (Public-Private Partnership) concessions. The results are showing up in the cash flow statement. Operating cash flow grew by 11% to €890 million in the first nine months of the year.

The company continues to replenish its portfolio with high-quality wins. Recent awards include the €525 million Novara City of Health project in Italy and a massive water reuse plant in Antofagasta, Chile, with an investment of €300 million.

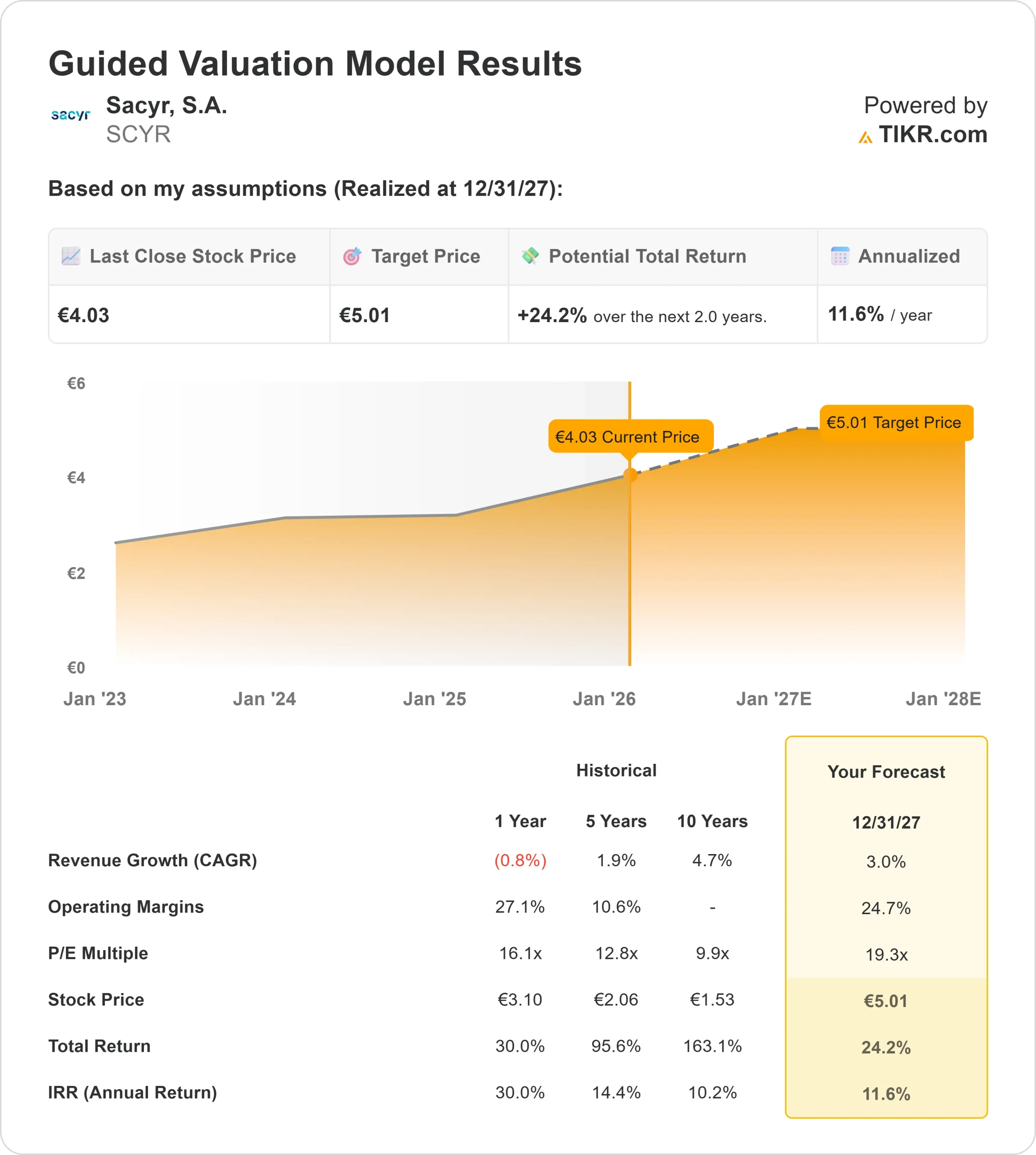

With the stock trading at €4.03, the market is valuing Sacyr at a discount to the intrinsic value of its assets. Management’s own valuation of the concession portfolio stands at almost €4 billion, suggesting the equity is undervalued.

See analysts’ full growth forecasts and estimates for Sacyr stock (It’s free) >>>

What the Model Says for SCYR Stock

We evaluated Sacyr’s potential through 2027, factoring in the stability of its concession cash flows and the continued execution of its asset rotation plan.

Our model signals a “Buy.” Using a forecast of 3.0% Revenue Growth (CAGR) and 24.7% Operating Margins, the model projects the stock could reach €5 by the end of 2027.

This implies an 11.6% annualized return over the next two years.

This return profile is attractive for a defensive stock. It suggests that as the market gets more comfortable with Sacyr’s debt profile and pure-play status, the valuation multiple will hold steady while earnings compound.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SCYR stock:

1. Revenue Growth: 3.0%

Selective bidding ensures quality over quantity.

Sacyr is not chasing revenue for revenue’s sake. The company recently divested its concession assets in Colombia, which impacted short-term comparisons but strengthened the balance sheet.

Growth is now driven by new assets coming online. The company brought 3 assets into operation this year, including the Rutas del Este in Paraguay and the Ferrocarril Central in Uruguay (not explicitly named in text but implied by the “4 new concession awards” context).

We forecast steady revenue growth of 3.0% CAGR through 2027. This reflects the inflation-linked nature of toll road tariffs and the ramp-up of new projects like the Buga-Buenaventura Highway in Colombia.

2. Operating Margins: 24.7%

Concessions drive high margins.

The shift in mix is dramatic. EBITDA margin rose in the period, driven by the operational efficiency of the concession division. Construction, while smaller, is also performing well, with margins standing stable at 4.8%.

We project operating margins (EBIT) to normalize at 24.7%, a very high figure typical of infrastructure operators where the bulk of costs are upfront capex rather than ongoing opex.

3. Exit P/E Multiple: 19.3x

Utility-like valuation.

Sacyr currently trades at roughly 16.1x earnings.

Our model assumes an exit multiple of 19.3x by 2027.

This expansion assumes that Sacyr will increasingly be viewed as a “bond proxy” or utility infrastructure company rather than a cyclical builder. With 92% of EBITDA coming from concessions, this re-rating is justified by the lower risk profile of the cash flows.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Investors should exercise caution regarding the longer-term horizon (these are estimates, not guaranteed returns):

- Low Case: If interest rates stay high or execution slips, the stock could face significant downside, with our advanced model showing a potential -4.4% annual return.

- Mid Case (Long Term): Notably, our 4-year advanced model is much more conservative than the 2-year guided model, projecting essentially 0% annual return (flat price) through 2029.

- High Case: If the market aggressively re-rates the stock to match the €4 billion asset valuation, returns could reach 3.6% annual return in the conservative advanced scenario, but likely higher if the full asset value is realized.

(Investor Note: There is a discrepancy between the bullish short-term view (11.6% IRR) and the flat long-term view (0% IRR). The investment thesis relies heavily on a near-term realization of value, perhaps through further asset sales or dividends.)

See what analysts forecast for the next 5 years for SCYR stock (Free with TIKR) >>>

How Much Upside Does Sacyr Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!