Key Stats for Pinterest Stock

- 52-Week Range: $14 to $40

- Current Price: $20

- Street Mean Target: $23

- Street High Target: $45

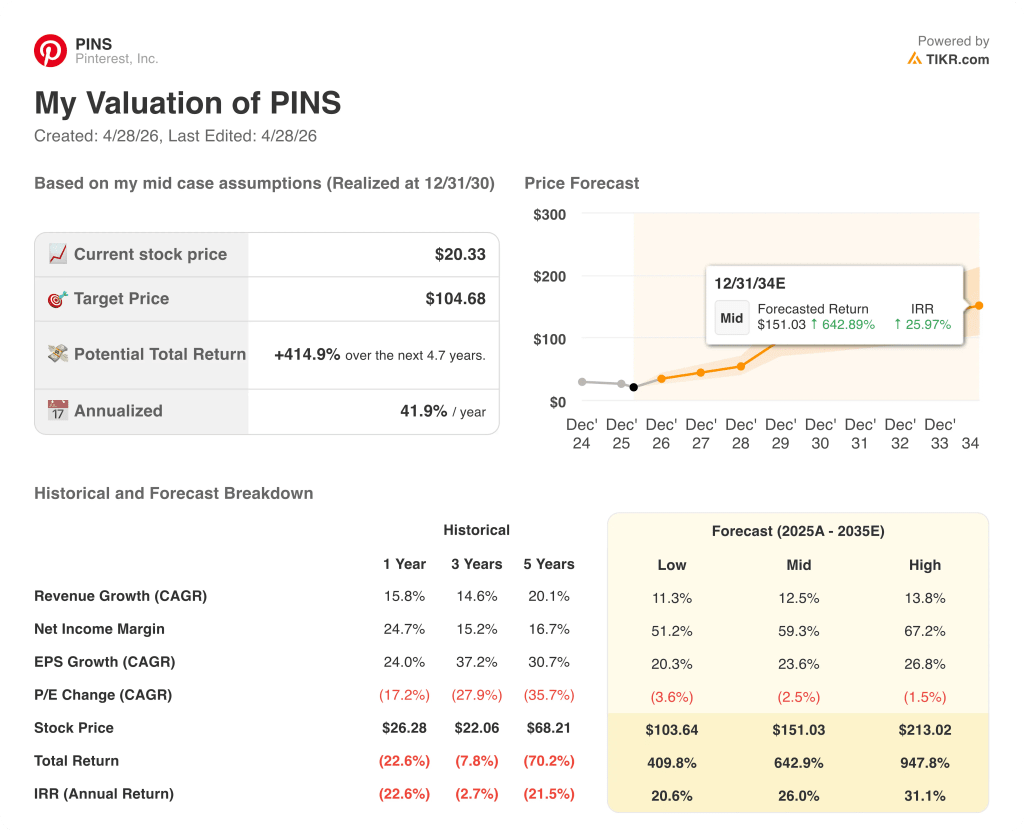

- TIKR Model Target (Dec. 2030): $105

What Happened?

Pinterest stock (PINS) is trading nearly 50% below its 52-week high after a year defined by one painful paradox: a platform generating 80 billion monthly searches and 10 consecutive quarters of record users that cannot convert that engagement into revenue growth fast enough to satisfy Wall Street.

The stock hit $14 in early 2026 before recovering to $20, still less than half its year-ago price, as investors absorbed a Q4 2025 earnings miss, a restructuring announcement, and guidance that signaled further near-term pressure.

The Q4 miss was specific and avoidable in hindsight: Pinterest’s outsized mix of large retail advertisers left it absorbing tariff-driven ad budget pullbacks more acutely than peers with broader revenue bases.

Revenue came in at $1.32 billion, growing 14% year over year but still short of the $1.33 billion consensus estimate, and the damage spread to Europe, where major global retailers rebalanced spend across geographies in the same move.

Elliott Investment Management responded to the selloff by converting a $1 billion convertible note placement into the company’s largest shareholder position, at an initial conversion price of $22.72, and Pinterest simultaneously authorized a $3.5 billion share repurchase program representing nearly a third of its market value.

The $3.5 billion buyback plus the Elliott capital injection is the structural backstop the stock needed, but the actual re-rating will come from execution: broadening revenue away from large retailers into mid-market, SMB, and international advertisers, and proving the tvScientific acquisition (a connected-TV performance platform purchased to extend Pinterest’s audience beyond its own surfaces) opens incremental budget pools.

Bill Ready, CEO, stated on the Q4 2025 earnings call that “our users and engagement are out in front of where our ad platform is, and the ad platform is out in front of where our sales and go-to-market capabilities are,” directly naming the gap that new Chief Business Officer Lee Brown, hired in late January, is now tasked with closing.

The 3- to 5-year case rests on three named drivers: accelerating managed SMB and mid-market revenue (currently just 15% of total versus meaningfully higher at competing platforms), the tvScientific CTV integration opening performance budgets beyond Pinterest’s owned-and-operated surfaces, and Pinterest Performance+ measurement integrations enabling tighter bid optimization with large advertisers that already proved out in one pilot where a single advertiser increased Pinterest bids by over 30%.

Wall Street’s Take on PINS Stock

Pinterest’s engagement flywheel, 619 million users and 80 billion monthly searches, is generating a monetization gap that a restructured go-to-market team is now racing to close before the next earnings cycle.

PINS consensus revenue is estimated at around $4.78 billion for 2026, up around 13% year over year, with EPS Normalized expected to reach around $1.80, up around 12% from $1.60 in 2025, as advertiser diversification gains traction and tvScientific contributes a partial-year top-line lift.

Of 38 analysts covering Pinterest stock, 17 rate it a buy, 1 an outperform, 20 a hold, and 1 an underperform, with a mean price target of $23.43 implying around 15% upside from the current $20.33 price; the consensus is waiting on Q1 2026 results (due May 4) to see whether tariff headwinds widened or stabilized in the first quarter.

The target range runs from $15.40 to $45, with the high-conviction bulls anchored to SMB acceleration and CTV monetization upside and the bears watching whether the sales transformation disrupts near-term revenue enough to break the mid-teens growth trajectory entirely.

The Elliott conversion price of $22.72 effectively sets a credible floor and signals that one of the world’s most rigorous activist investors sees a material gap between intrinsic value and current price.

If Q1 2026 revenue growth falls below 11% or management narrows full-year EBITDA guidance below the $163 to $183 million range cited in February, the execution narrative collapses and the bear case reasserts at current multiples.

The May 4 earnings report is the first real evidence checkpoint: Q1 revenue within or above the $958 to $978 million guidance range plus any commentary from Lee Brown on measurable SMB and mid-market progress would confirm the monetization inflection is tracking.

Pinterest Stock Financials

Pinterest’s operating income reached $320 million in 2025, up 49% year over year, extending a recovery from the ($130 million) operating loss in 2022 and marking the third consecutive year of meaningful profitability improvement.

The recovery is margin-led: gross margins expanded from 75.8% in 2022 to 80.1% in 2025 as infrastructure cost optimizations reduced cost of revenue relative to revenue, while $3.65 billion in 2024 revenue and $4.22 billion in 2025 allowed operating income to grow faster than the top line in both years.

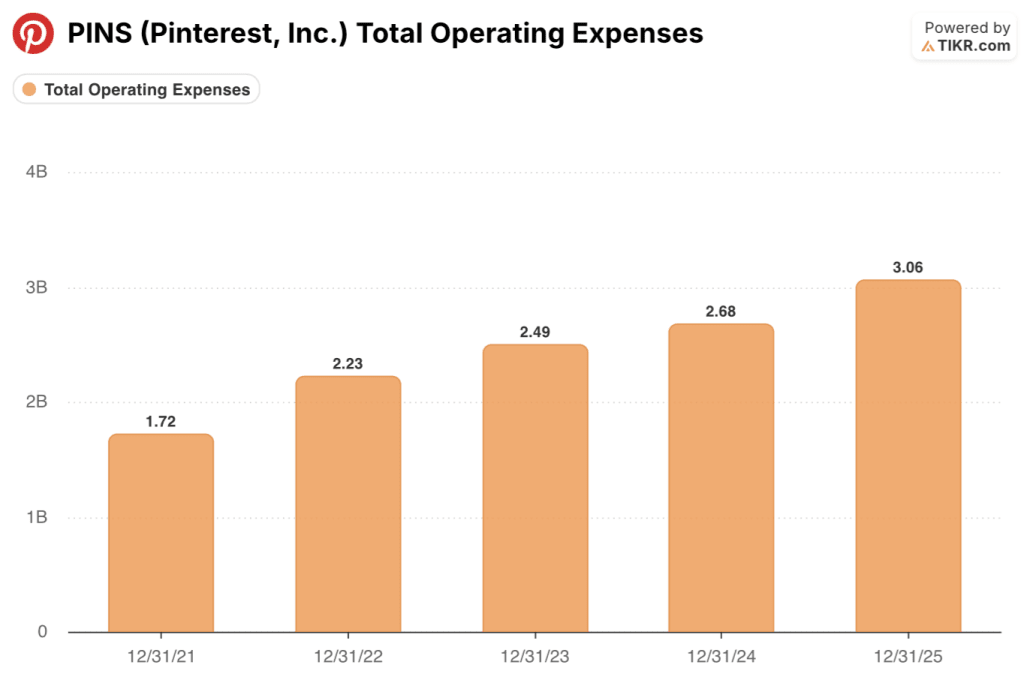

Total operating expenses grew from $2.49 billion in 2023 to $3.06 billion in 2025 as Pinterest invested in AI talent and sales force expansion, but the 15.8% revenue growth in 2025 outpaced that cost growth, sustaining the operating leverage story over a multi-year period.

The tension is whether Pinterest can hold that leverage through 2026: the company explicitly guided to gross margin headwinds of around 100 basis points from GPU infrastructure investments and flagged that restructuring savings of around $100 million annualized will be roughly half reinvested, leaving adjusted EBITDA margins roughly flat at around 29% on a combined basis with tvScientific.

What Does the Valuation Model Say?

The TIKR model puts Pinterest stock’s mid-case target price at around $105 by December 2030, built on a revenue CAGR assumption of around 13% and net income margins expanding toward around 59%, assumptions grounded in the platform’s already-demonstrated operating leverage and the incremental monetization upside from SMB advertiser scaling and tvScientific CTV revenues.

With EPS Normalized at $1.60 in 2025 and the forward multiple compressing to roughly 11x against a backdrop of accelerating EPS growth toward around $2.21 in 2027, Pinterest stock is undervalued: the multiple re-rating alone, even without earnings upside, closes a material portion of the gap to the TIKR model target.

What Has to Go Right / What Could Go Wrong

Pinterest stock is a monetization story, not a user story: the bull case is that 80 billion monthly searches and 619 million users are fundamentally undermonetized, and the new go-to-market team closes that gap over 2026 to 2027.

What Has to Go Right

- Lee Brown’s SMB and mid-market go-to-market overhaul accelerates managed SMB revenue, which doubled its growth rate in 2025 but still represents only around 15% of total revenue versus materially higher at competing platforms

- tvScientific CTV integration opens incremental performance budgets beyond Pinterest’s own surfaces; Q4 2025 management commentary indicated that CTV is one of the fastest-growing segments of the ad market and that tvScientific drove search-type performance metrics in TV

- Pinterest Performance+ measurement integrations deepen with large advertiser proprietary bid systems; one pilot already produced a 30%+ increase in advertiser bids, and the company plans to expand that program through the first half of 2026

- Large retail advertisers start to anniversary tariff headwinds in the second half of 2026 per management guidance, removing the single biggest drag that pushed Q4 2025 revenue below consensus

What Could Go Wrong

- The sales transformation creates more than a couple of quarters of disruption; management explicitly acknowledged that restructuring impacted frontline sellers and measurement staff in January, and Q1 2026 guidance factored in productivity loss from backfilling those roles

- SMB and mid-market acceleration takes longer than 2 to 4 quarters to show up in reported revenue, keeping growth stuck at 11% to 13% while the Street loses patience with the execution story

- Digital ad budget concentration accelerates toward Meta and Google per Stifel’s reduced 2026 industry growth forecast from 8.3% to around 7%; smaller platforms including Pinterest are explicitly named as most at risk of incremental cuts when advertisers tighten

- Elliott’s $22.72 conversion price creates a psychological ceiling near the current price, reducing near-term upside until execution evidence exceeds that threshold convincingly

Should You Invest in Pinterest, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PINS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Pinterest, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PINS stock on TIKR for Free →