Key Stats for Procter & Gamble Stock

- 52-Week Range: $137.62–$167.25

- Current Price: $151.98

- Street Mean Target: ~$163

- TIKR Target Price (Mid): ~$202

- Market Cap: ~$352 billion

- Dividend Yield: ~2.9%

- LTM Gross Margin: 51.0%

- LTM P/E: ~22x

- Consecutive Years of Dividend Growth: 70

Most investors never know if a stock is truly undervalued or overpriced. TIKR’s professional-grade valuation tools give you a clear, data-backed answer across 60,000+ stocks for free →

From Category Dominance to a 16% Drawdown: What’s Driving the Pressure on P&G Stock

Procter & Gamble (PG) is one of the most widely owned stocks in the world. Tide, Pampers, Gillette, Oral-B, and Head & Shoulders are not niche products. They are category leaders in dozens of countries, and their owner has compounded earnings through recessions, pandemics, and commodity cycles for more than a century. So when PG stock falls into a double-digit drawdown, investors pay attention.

That is exactly where the stock finds itself in mid-2026. PG hit a 16% drawdown on June 3 before partially recovering to around -10% from its highs. The slide began in late February and has been largely sustained since.

The causes are not hard to identify. P&G is absorbing roughly $400 million in after-tax tariff costs in fiscal 2026, alongside commodity headwinds and higher reinvestment spending. Core gross margin compressed 100 basis points last quarter.

The company also announced a restructuring program targeting up to 7,000 non-manufacturing job cuts, a move designed to reduce overhead but one that carries charges clouding near-term earnings. Bernstein initiated coverage with a Market Perform rating, citing private-label pressure in categories such as bathroom tissue and diapers.

P&G is mid-execution on a multi-category innovation rollout that will determine whether U.S. growth reaccelerates into fiscal 2027. Start tracking PG for free →

A Business Built on Brands That Do Not Lose

The near-term noise is real. But the financial history here is difficult to dismiss.

Normalized EPS grew from $5.66 in fiscal 2021 to $6.83 in fiscal 2025, a steady, unbroken climb. Consensus estimates carry that number to around $6.90 this fiscal year, essentially flat, as tariff and restructuring costs hit earnings in real time.

From fiscal 2027 onward, estimates reaccelerate toward around $8 by fiscal 2030. The compression looks temporary, but the long-term earnings engine looks intact.

That view rests on something most companies cannot claim: genuine pricing power across a portfolio of dominant brands. P&G occupies the premium tier in nearly every category it competes in. The evidence from the past five years shows it has consistently pushed pricing through, and volume has largely followed. Organic sales grew 3% last quarter, with broad participation across all five business segments and most major geographies.

The restructuring deserves a closer look, as cutting 7,000 non-manufacturing roles is not a distress signal. It is a margin lever. The company is simplifying its cost structure and pointing resources toward brand investment and innovation.

Tide evo, an ultraconcentrated laundry format, is a concrete example of the premium-product work P&G uses to defend shelf position against private label. “We’re increasing investments to accelerate momentum with consumers,” said CEO Shailesh Jejurikar in the most recent earnings release, “while still maintaining our guidance ranges for the fiscal year.”

The balance sheet adds weight to the argument. P&G returned $3.2 billion to shareholders in its fiscal third quarter alone via dividends and buybacks. The 70th consecutive annual dividend increase signals confidence in cash generation that few businesses can match.

See how PG performs against its peers in TIKR (It’s free!) >>>

What Does the Valuation Model Say?

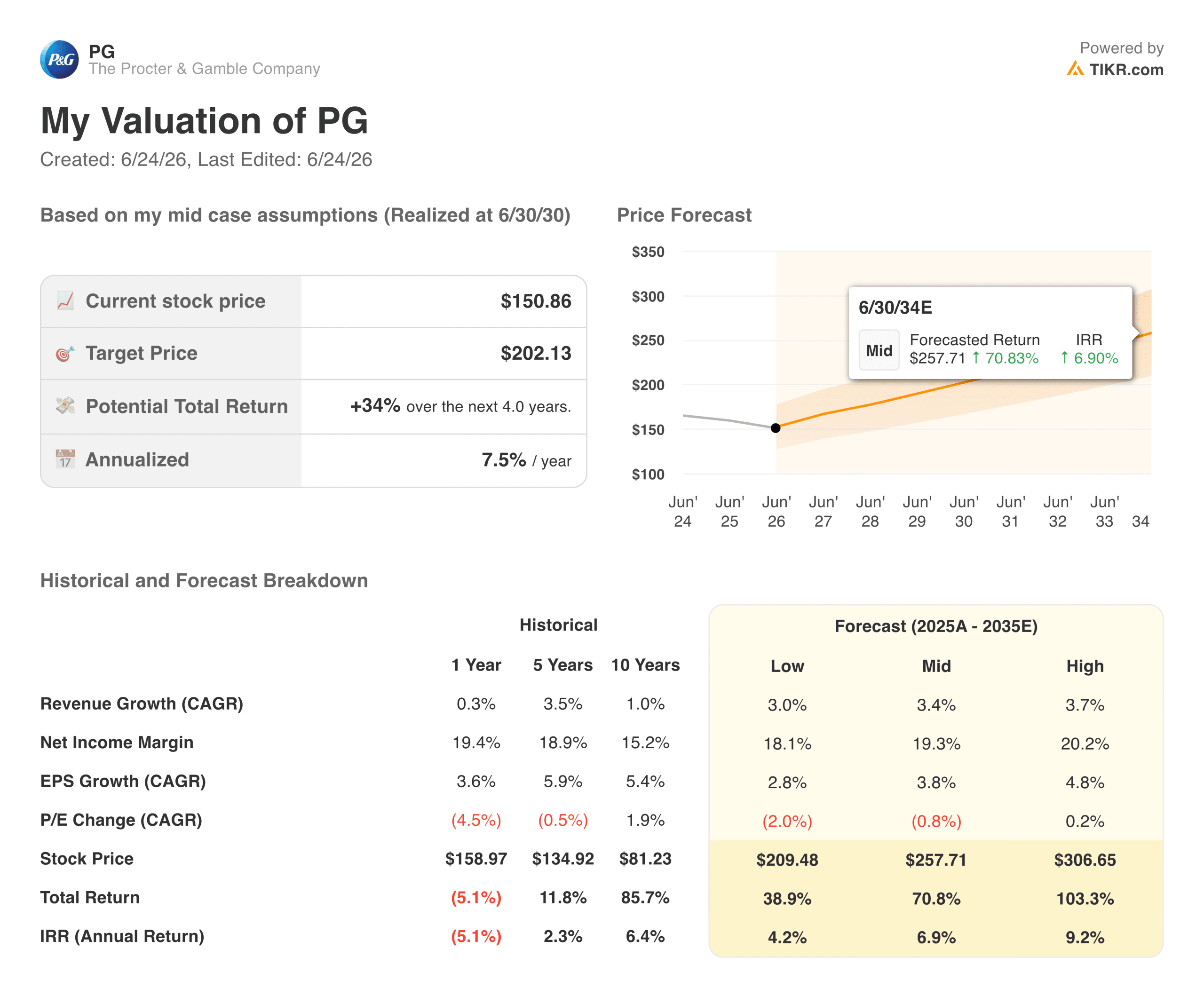

TIKR’s valuation model targets around $202 per share in its mid case, representing roughly 34% total return from current levels at about 7.5% annualized over the next four years. The high case reaches around $258 by 2034, assuming revenue growth in the low- to mid-single-digit range and net income margins near historical levels.

The current P/E of around 22x sits at a discount to where PG has historically traded when the business was performing at full strength. Near-term EPS compression from tariffs and restructuring explains most of that gap. If those headwinds ease as the cost structure improves, the multiple has room to recover.

The risks are real, and private label is gaining ground in diapers and household paper. FX headwinds are structural for a company operating in roughly 70 countries. And any restructuring introduces execution risk, particularly when paired with a CEO transition.

Should You Invest in Procter & Gamble?

PG is not a story about explosive upside. It never has been. It is a story about a business that compounds quietly over time, returns enormous amounts of cash, and holds its value better than most when markets get difficult. The current drawdown puts it at a more attractive entry point than investors have seen in some time.

The real question is not whether P&G is a good business. It clearly is. The question is whether the current headwinds are temporary noise or the beginning of a structural shift in how consumers relate to premium brands. If you believe the former, the stock looks interesting here. If private label momentum and tariff uncertainty feel more durable to you, patience may be warranted.

Access Professional Tools to Analyze PG stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!