Key Stats for PepsiCo Stock

- 52-Week Range: $128 to $171

- Current Price: $142

- Street Mean Target: $171

- Street High Target: $195

- Analyst Consensus: 4 Buys / 4 Outperforms / 14 Holds / 1 Sell

- TIKR Model Target (Dec. 2030): $199

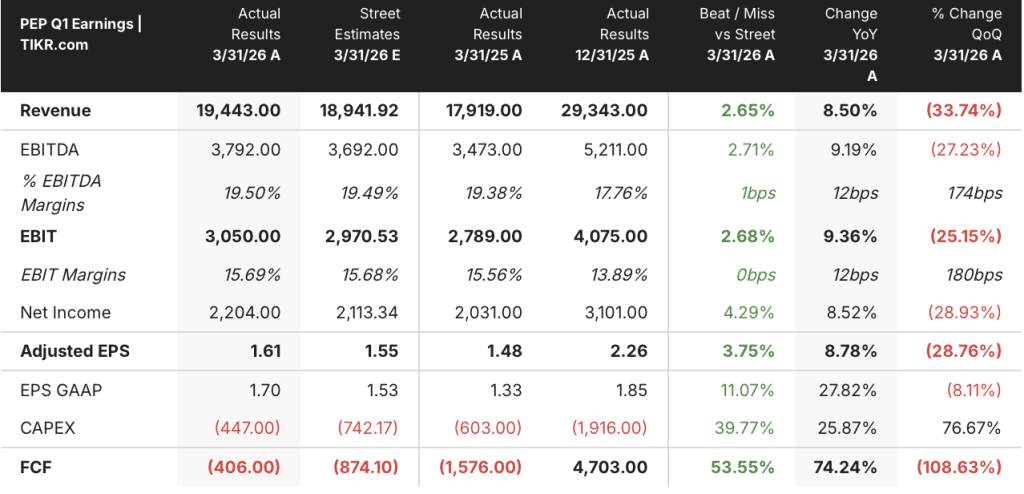

PepsiCo Stock Beats Q1 EPS by 9% as North America Foods Volume Finally Turns Positive

PepsiCo (PEP) delivered first-quarter 2026 EPS of $1.61, beating the Street estimate of $1.55 by around 4%, while net revenue grew 8.5% year over year to $19.4 billion, as the company’s long-awaited volume recovery in North America Foods arrived with tangible momentum.

PepsiCo is a global food and beverage conglomerate with leading positions in salty snacks through Frito-Lay, beverages through the Pepsi and Gatorade portfolios, and nutrition through Quaker Oats.

The North America Foods segment, known internally as PFNA, grew volume 2% in Q1 and unit volume 4%, adding 300 million new consumption occasions versus the same quarter last year.

Lays, Doritos, and Tostitos are being restaged globally, with shelf resets roughly 50% complete at the time of the earnings call.

Away From Home revenue within PFNA grew at roughly three times the segment average, and the permissible snack portfolio, including SunChips, Smartfood, and Siete, grew double digits.

On the beverage side, PepsiCo Beverages North America (PBNA) reported total revenue growth of 9%, combining 2% organic growth with 7 points from acquired platforms including poppi, the prebiotic soda brand acquired for around $1.95 billion.

CEO Ramon Laguarta described the quarter in the Q1 2026 earnings call as delivering “an acceleration in both net revenue and organic revenue growth, with a notable improvement in convenient foods organic volume,” and confirmed the company is “a little bit ahead of where we thought we would be by now” on the PFNA recovery.

The company reaffirmed full-year guidance for 2% to 4% organic revenue growth and 4% to 6% core constant currency EPS growth.

Wells Fargo cut its PepsiCo stock price target to $150 from $160 on June 5, 2026, a move that underscores lingering caution from parts of the Street even as the fundamental data begins to turn.

PepsiCo declared a quarterly dividend of $1.48 per share for June 2026, up 4% from the prior year, marking the company’s 54th consecutive annualized dividend increase.

Why PEP Analysts Are Holding Targets Despite the Wells Fargo Cut

PepsiCo stock trades at a 17% discount to the Street mean target of $171, with 21 analysts covering the name and a consensus that leans cautious but is not bearish.

The distribution of 4 Buys, 4 Outperforms, 14 Holds, and 1 Sell reflects a market that has not fully bought into the recovery narrative yet, which is precisely where the opportunity is priced.

Q1 adjusted EPS of $1.61 came in 3.75% above the Street estimate of $1.55, with core EPS up 9% year over year, the sharpest beat in recent quarters.

The forward EPS trajectory builds on that base: consensus estimates $2.23 for the June quarter (up around 5% year over year), $2.44 for September (up around 7%), and $2.41 for December (up around 7%), all on a normalized basis.

Full-year 2026 normalized EPS is estimated at around $8 on a summed basis across four quarters, with 2027 continuing that step-up.

Revenue consensus projects around $24 billion for the June quarter (up around 6% year over year) and around $25 billion for September (up around 5%), signaling that the top-line recovery is expected to broaden beyond the Q1 beat.

The EBITDA picture reinforces the earnings trajectory: Q1 EBITDA came in at $3.8 billion, beating the Street estimate of $3.7 billion, with EBITDA margins at 19.5%, up 12 basis points year over year, holding steady despite the volume investment in PFNA.

CFO Steve Schmitt pointed directly to productivity as the structural offset, noting reduced headcount, plant closures, and SKU rationalization are translating into improved cases-per-hour metrics and lower per-unit cost in North America Foods.

The company’s 6- to 12-month commodity hedging program provides near-term cost visibility, though Schmitt acknowledged that inflation from higher U.S. production, distribution, and retail costs is coming, with the magnitude still being worked through.

PEP stock is undervalued relative to the Street’s own price targets, with even the most cautious holders sitting at targets above the current price, and the high-conviction bull case sitting at $195.

The Q2 earnings release on July 9, 2026 is the next clean read on whether the PFNA shelf reset and innovation rollout is converting distribution gains into sustained organic revenue acceleration.

PepsiCo Stock Earns More Than Coca-Cola and Keurig Dr Pepper Combined Each Quarter

PepsiCo stock’s normalized EPS of $1.61 in Q1 dwarfs Coca-Cola’s (KO) $0.81 and Keurig Dr Pepper’s (KDP) $0.37 in the same period, a earnings gap that reflects PepsiCo’s diversified snack-and-beverage model versus peers whose earnings are almost entirely beverage-derived.

The gap holds through the forward estimates: consensus puts PepsiCo stock at $2.23 in the June quarter, versus $0.93 for Coca-Cola and $0.54 for Keurig Dr Pepper.

PepsiCo stock’s combined EPS lead over both peers expands further in the September quarter, where consensus projects $2.44 for PEP against $0.88 for KO and $0.63 for KDP, suggesting the earnings premium is not a one-quarter artifact but a structural feature of the business model.

The mispricing argument sharpens here: PepsiCo stock is trading near its 52-week low while producing more than twice Coca-Cola’s quarterly earnings power, a ratio that has held consistently across the last four reported periods.

Is PepsiCo Stock Undervalued in 2026? TIKR’s $199 Model Says Yes, with Conditions

TIKR’s base case values PepsiCo at approximately $199 by December 2030, implying around 40% total return from the current price of $142, or roughly 8% annualized over approximately 4.6 years.

The mid case assumes revenue growing at around 3% annually and net income margins expanding toward around 12%, consistent with PepsiCo’s own five-year historical margin profile of around 11%.

If PFNA completes its shelf reset and innovation cycle, organic revenue reaches the high end of the guided 4% to 6% long-term range, and net income margins approach around 13%, TIKR’s high case puts PepsiCo stock at approximately $284, implying around 100% total return, or roughly 8% annualized through 2035.

If the Iran war costs inflate faster than the hedge program absorbs, organic growth stays at the low end of guidance, and margin expansion stalls, TIKR’s low case of approximately $201 still implies around 41% total return from current levels, or roughly 4% annualized, anchored by dividend income.

The common thread across all three scenarios is that the current price of $142 already prices in a substantial discount to intrinsic value, and it takes a failure of both the top-line recovery and margin defense simultaneously to produce a poor outcome from here.

Is PepsiCo stock a buy right now?

PepsiCo stock trades at $142, a 17% discount to the Street mean target of $171 and a 27% discount to the Street high target of $195.

TIKR’s base case implies around 40% total return through December 2030. With Q1 EPS up 9% year over year and North America Foods volume turning positive for the first time in several quarters, the fundamental inflection is underway.

The key variable is whether the PFNA shelf reset drives durable organic growth through Q2 and Q3.

What do analysts say about PEP stock?

Twenty-one analysts cover PepsiCo, with 4 Buys, 4 Outperforms, 14 Holds, and 1 Sell. The Street mean target is $171, implying around 20% upside from current levels.

The cautious distribution reflects lingering skepticism about the pace of the North America Foods recovery, but no analyst has a target below the current price, and the high target of $195 implies around 37% upside.

Should You Invest in PepsiCo, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PepsiCo, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PepsiCo, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PEP stock on TIKR for Free →