Key Stats for Upstart Stock

- 52-Week Range: $24 to $87

- Current Price: $30

- Street Mean Target: $40

- Street High Target: $80

- Analyst Consensus: 6 Buy, 2 Outperform, 6 Hold, 1 Underperform

- TIKR Model Target (Dec. 2030): $179

Upstart Grew Originations 61% in Q1 — and the Market Sent the Stock Down Anyway

Upstart Holdings (UPST) delivered first-quarter 2026 results showing 61% origination growth and $308 million in total revenue, yet the stock continued its slide toward multi-year lows as investors fixated on a widening net loss and margins that came in below prior-quarter levels.

The AI lending marketplace originated around $3.4 billion in loans during Q1, up 77% in unit count to 425,356 loans — more than any pure fintech platform in the U.S., per CEO Paul Gu.

Revenue from fees reached $277 million, up 49% year over year, as higher origination volumes drove both platform fee income and a 52% jump in servicing revenue.

The net loss widened to $6.6 million, or -$0.07 per diluted share, compared with a $2.4 million loss in Q1 2025, reflecting front-loaded investment spending and seasonal operating cost patterns that management described as expected and temporary.

Adjusted EBITDA came in at around $40 million with a 13% margin, down from the prior quarter, as marketing spend increased and fixed costs stepped up in the typical Q1 cycle reset.

“Originations grew 61% year-over-year and revenue grew 44%, while profit declined marginally,” Gu said on the Q1 2026 earnings call. “These are strong results and put us comfortably on track to meet our full year guidance on both the top and bottom lines.”

Home originations grew more than 250% year over year and 16% sequentially, with more than a quarter of loans fully automated and an average time to close of 6 days versus an industry average of roughly 40 days.

Auto originations surged more than 300% year over year and 30% sequentially, with retail auto rising roughly 13x year over year as the dealer network expanded rapidly.

Upstart also announced Cash Line, its first revolving credit product, which Gu described as having “probably the best first day we’ve ever had for a new product launch.”

In March, the company applied for a national bank charter with the OCC — a move Gu framed as a path to lower origination costs, expanded addressable market across all 50 states, and a direct regulatory relationship as AI in lending draws increasing scrutiny.

The company reiterated full-year 2026 guidance of around $1.4 billion in total revenue and around $294 million in adjusted EBITDA, a 21% margin, with EBITDA growth weighted toward the second half of the year.

May origination volume came in at $1.45 billion across 25 origination days, or around $58 million per day, signaling Q2 momentum is intact.

Analysts See 35% Upside on Upstart Stock, but the EPS Recovery Has to Arrive on Schedule

At around $30, Upstart stock sits 35% below the Street mean target of around $40 and nearly 67% below the Street high of $80, a spread that reflects genuine analyst disagreement about how fast the platform scales and whether the margin trajectory is real.

The 6/5/26 consensus of 6 Buy, 2 Outperform, 6 Hold, and 1 Underperform positions Upstart as a moderately convicted buy — the buys outnumber the holds, but not by a wide margin, and the full-year outlook from most analysts hinges on whether Q1’s margin compression was truly seasonal or structural.

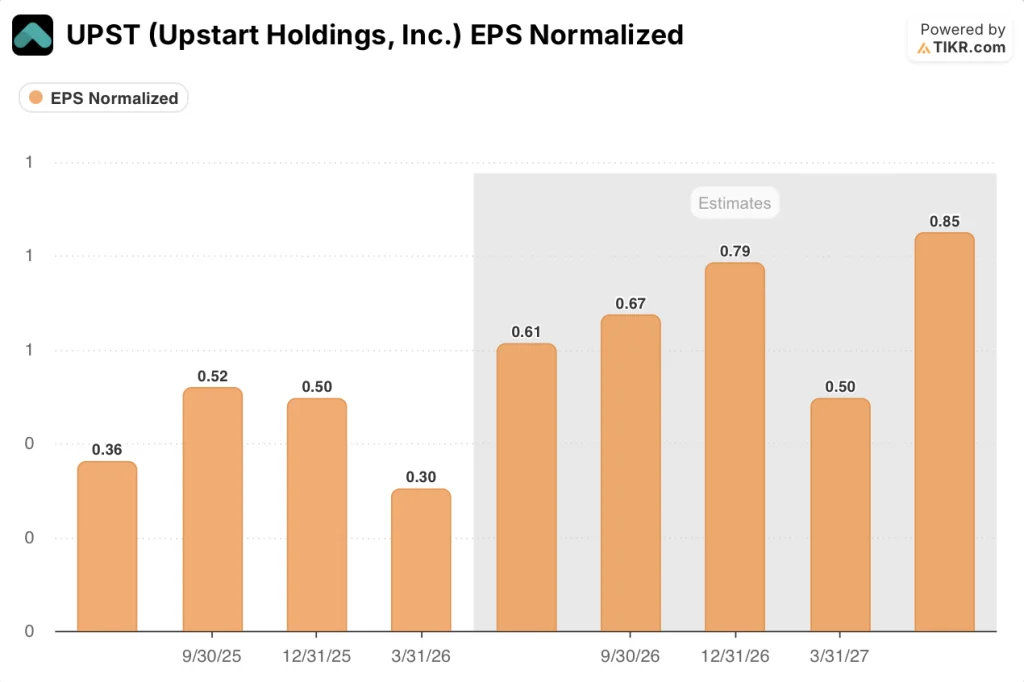

Upstart stock’s EPS is expected to recover sharply through the rest of 2026, with Q2 2026E at $0.61 versus $0.30 reported in Q1, followed by $0.67 in Q3 2026E and $0.79 in Q4 2026E, a progression that would validate Upstart’s claim that adjusted EBITDA is heavily back-half-weighted.

The catalyst that resolves this debate most cleanly is core personal loan origination growth: Q1 core personal loans were flat sequentially against a historical pattern of roughly 10% sequential declines in Q1, and CFO Andrea Blankmeyer explicitly flagged that contribution margin in Q1 was expected to be the low point for the year.

Is Upstart Stock Undervalued in 2026? TIKR’s $179 Model Says the Market Has It Wrong

TIKR’s mid-case model values Upstart at approximately $179 by December 2030, implying around 503% total return from the current price of around $30, or roughly 48% annualized over approximately 4.6 years.

The mid-case rests on a revenue CAGR of around 21% through 2035, net income margins expanding to around 38%, and EPS growth compounding at around 29% annually — assumptions that Upstart’s own three-year guidance of around 35% annualized revenue growth actually exceeds at the top end.

If revenue growth slows to around 19% annually and margins land near the low-case assumption of around 34% net income margin, the model produces a stock price near $180 by 2034, with an annualized return of around 23%.

If the bank charter accelerates addressable market expansion and origination costs fall as Gu has outlined, the high-case scenario of around $415 by 2034 and an IRR near 36% becomes plausible, anchored in the $200 million in annual frictional costs Upstart has identified as removable under a bank structure.

The funding base that underlies all three scenarios is already in place: Upstart signed more than $4 billion in committed capital year to date in 2026, including a 24-month Centerbridge commitment and a $1.25 billion Fortress forward-flow renewal, and has maintained a 100% partner renewal rate since 2022.

Upstart stock at around $30 is undervalued relative to what the TIKR model requires to justify the current price — which is a scenario where growth stalls materially below both company guidance and the current origination run rate.

Is Upstart stock a buy right now?

At around $30, Upstart stock trades at a 35% discount to the Street mean target of around $40 and far below TIKR’s mid-case intrinsic value of around $179 by December 2030.

The consensus leans Buy, with 8 Buys or Outperforms against 6 Holds and 1 Underperform.

The critical variable is whether adjusted EBITDA margin expansion materializes in Q2 and Q3 2026 as guided.

What happened to Upstart stock after Q1 2026 earnings?

Upstart stock fell after Q1 results despite 61% origination growth and a reaffirmed full-year outlook, as investors focused on a widening net loss of $6.6 million and an adjusted EBITDA margin of 13% that came in below Q4 2025 levels.

Management attributed the margin compression to front-loaded annual compensation costs, a seasonal dip in borrower demand, and deliberate marketing investment, and reiterated that Q1 contribution margin was the low point for the year.

Should You Invest in Upstart Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Upstart Holdings, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Upstart Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UPST stock on TIKR for Free →