Key Stats for Procter & Gamble Stock

- 52-Week Range: $138 to $167

- Current Price: $147

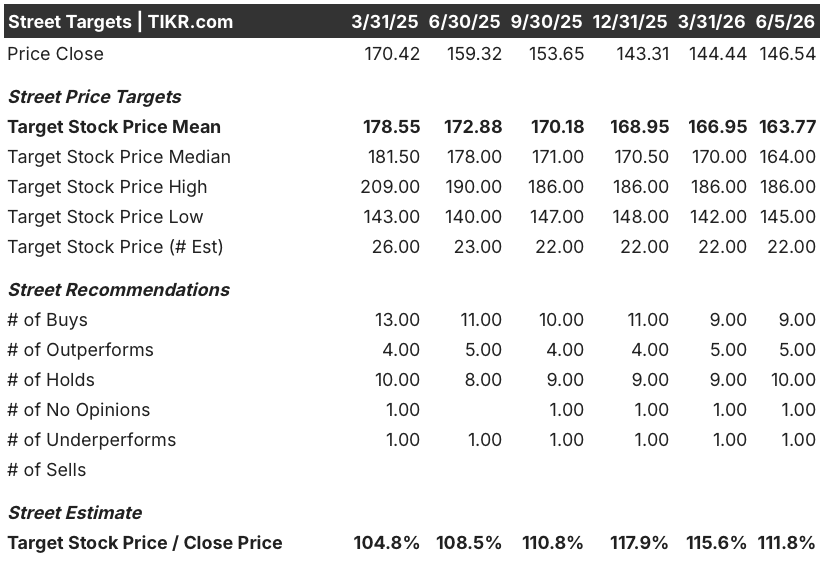

- Street Mean Target: $164

- Street High Target: $186

- Analyst Consensus: 9 Buys, 5 Outperforms, 10 Holds, 1 Underperform

- TIKR Model Target (Jun. 2030): $201

P&G Stock Beat Q3 Estimates on Beauty Demand, Then Warned of a $1 Billion FY2027 Oil Hit

Procter & Gamble (PG) jumped around 4% on April 24 after posting fiscal Q3 2026 net sales of $21.24 billion, a 7% year-over-year increase that cleared the consensus estimate of around $20.5 billion.

Organic sales grew 3% in the quarter, driven by 2 points of volume and 1 point of pricing, with all 10 product categories and all 7 geographic regions posting growth.

The beauty segment led, with organic sales up 7%, powered by Pantene and SK-II, as wealthier consumers continued trading up even as lower-income households pulled back.

The same quarter that produced the beat also delivered the forward warning: CFO Andre Schulten said the surge in Brent crude from around $60 per barrel before the Iran conflict to around $100 today would produce a roughly $1 billion after-tax profit hit in fiscal 2027, the year beginning July 2026.

“The noise, I would call it, from the commodity exposure is significant, as a billion dollars after tax is nothing to sneeze at from a headwind standpoint,” Schulten said on the Q3 earnings call.

P&G also flagged a $150 million after-tax Q4 FY2026 headwind from commodity-linked cost inflation, feedstock exposure, and logistics disruption from the Middle East conflict, with almost all of that cost landing in the fiscal fourth quarter.

The company maintained its FY2026 guidance of 0% to 4% organic sales growth and core EPS of $6.83 to $7.09 per share, while guiding that results would land toward the lower end of the EPS range.

At the June 3 Deutsche Bank conference, Schulten went further on the restructuring already underway: P&G is on track to reduce its non-manufacturing workforce by up to 7,000 roles, or roughly 15%, over two years, with slightly more than half of those reductions already executed.

The restructuring program, announced in June 2025, is expected to cost between $1 billion and $1.6 billion before tax and is already delivering benefits in supply chain efficiency and organizational speed.

Separately, P&G raised its quarterly dividend 3% to $1.0885 per share in April 2026, extending the company’s consecutive annual dividend growth streak to 70 years.

Why PG Analysts Hold Targets Above $160 Even With a $1 Billion Cost Headwind on the Horizon

The investment debate around Procter & Gamble stock is not whether the $1 billion oil headwind is real. It is whether the market has overpriced it in.

P&G stock’s Q3 normalized EPS came in at $1.59, up 3.2% from $1.54 a year earlier, beating the consensus estimate of $1.56.

The forward picture is where the Street has grown more cautious. The Q1 FY2027 (quarter ending September 2026) consensus estimate sits at $1.97 normalized EPS, down about 1% from the year-ago quarter, reflecting early absorption of the oil headwind.

The following quarter, December 2026, consensus EPS is estimated at $1.90, roughly flat year over year, suggesting Wall Street models the cost pressure stabilizing rather than compounding.

By the March 2027 quarter, the consensus returns to modest growth, with normalized EPS estimated at $1.62, up about 2% year over year.

Revenue expectations are similarly measured. Consensus puts Q1 FY2027 quarterly revenue at around $23 billion, up about 3% from the prior year quarter, with Q2 FY2027 at around $23 billion as well.

The 22 analysts with coverage set a mean price target of $164 and a high of $186, implying roughly 12% upside to the mean and roughly 27% to the high from the current $147 level.

The consensus is 9 Buys, 5 Outperforms, 10 Holds, and 1 Underperform, a distribution that tilts constructive but reflects real uncertainty: the Holds cluster acknowledges the oil headwind is quantified but not yet offset.

Jefferies (Buy, $177 target) argued that with the commodity headwind now quantified, estimates can reset to a more realistic base, while P&G retains enough profit flexibility to support EPS growth and continue brand investment.

J.P. Morgan (Overweight, $164 target) noted the $1 billion figure represents a worst-case scenario if Brent stays near $100 per barrel and that P&G can partly offset pressure through productivity savings, innovation-led pricing, and selective price hikes.

Morgan Stanley (Overweight, $166 target) flagged that Q4 FY2026 margins will face direct pressure from the after-tax cost headwind, arriving too fast for near-term offsets, even as P&G continues to invest in innovation and demand generation.

Piper Sandler (Neutral, $145 target) acknowledged short-term productivity savings as a partial buffer but expects P&G will still need to absorb some cost pressure.

The structural argument for Procter & Gamble stock is that P&G sits in daily-use categories where consumers have no easy substitute, generates around $2 billion in annual productivity savings, and is executing the deepest organizational restructuring in over a decade, all of which gives it more levers to absorb the oil shock than most consumer staples peers.

How PG and Colgate-Palmolive Stock EPS Compare as Oil Costs Hit Both Companies

Procter & Gamble stock’s normalized EPS of $1.59 in the March 2026 quarter runs nearly 70% above Colgate-Palmolive’s (PL) $0.94 in the same period, a gap that reflects the scale difference between the two businesses but also P&G’s deeper earnings base to absorb the oil shock.

The forward estimates show P&G stock’s earnings pressure is more pronounced: consensus puts PG normalized EPS at $1.42 for the June 2026 quarter, down about 4% from $1.48 a year earlier, while Colgate is estimated at $0.95, up about 1% from $0.89 — meaning Colgate enters the headwind period with modest EPS growth while P&G absorbs a year-over-year decline.

By March 2027, the trajectories converge toward recovery on both sides, with PG consensus EPS estimated at $1.62 and Colgate at $0.98, each returning to modest year-over-year growth as the worst of the oil cost absorption moves through the P&L.

The compression is temporary on P&G’s numbers but more visible given the absolute scale, and investors willing to look past the FY2027 trough are buying a business with more than twice the per-share earnings power of its nearest peer at a price that already reflects the bad news.

Is P&G Stock Undervalued in 2026? TIKR’s $201 Target Frames the Oil Shock as Temporary

TIKR’s base case values Procter & Gamble at approximately $201 by June 2030, implying around 37% total return from the current price of approximately $147, or roughly 8% annualized over the next four years.

The mid case assumes revenue growth around 4% annually, a net income margin of roughly 20%, and EPS growth around 4% per year, with P/E change modestly negative at around (1)% annually, reflecting a slight de-rating as cost pressures gradually ease and normalized earnings re-emerge.

The bear case, anchored to around 3% revenue growth and net income margins near 18%, still produces a stock price around $205 and total return around 40%, suggesting the downside floor is supported by P&G’s cash generation and the 70-year dividend growth streak.

The upside case, assuming around 4% revenue growth and net income margins near 21%, puts Procter & Gamble stock at approximately $299 by June 2030, implying around 104% total return and roughly 9% annualized.

The risk is duration: the $1 billion FY2027 headwind arrives before any material restructuring savings offset is visible in earnings, which means the next two quarters are likely to show the highest year-over-year EPS pressure before the trajectory improves.

Is Procter & Gamble stock a buy right now?

At $147, Procter & Gamble stock trades around 12% below the Street mean target of $164 and roughly 37% below TIKR’s base case target of about $201 by June 2030.

With 14 of 25 analysts at Buy or Outperform, and a 70-year dividend growth streak intact, the stock offers defensible total return potential for investors who can absorb the near-term FY2027 oil headwind.

The key risk is the timeline: cost pressure peaks in Q4 FY2026 and Q1 FY2027 before productivity offsets take hold.

What do analysts say about P&G stock?

The current consensus on Procter & Gamble stock is 9 Buys, 5 Outperforms, 10 Holds, and 1 Underperform, with a mean 12-month price target of $164.

Jefferies and J.P. Morgan maintain positive ratings, with Jefferies citing a realistic reset for estimates after the oil headwind is quantified.

Morgan Stanley holds an Overweight but flags margin pressure in Q4 FY2026. The primary disagreement is not on the long-term model, but on how quickly productivity savings and innovation-led pricing can offset the $1 billion FY2027 after-tax cost impact.

Should You Invest in The Procter & Gamble Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Procter & Gamble Company stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Procter & Gamble Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PG stock on TIKR for Free →