Key Stats for Synopsys Stock

- 52-Week Range: $376 to $652

- Current Price: $465

- Street Mean Target: $560

- Street High Target: $650

- Analyst Consensus: 15 Buys / 2 Outperforms / 7 Holds / 1 Underperform / 1 Sell

- TIKR Model Target (Oct. 2030): $840

Synopsys Beat Q2 Estimates and Raised Guidance, Then the Stock Fell Anyway

Synopsys (SNPS), the dominant provider of electronic design automation software and semiconductor IP used by virtually every advanced chipmaker on the planet, reported its fiscal Q2 2026 results on May 27, beating analyst estimates on both revenue and adjusted EPS and lifting its full-year outlook.

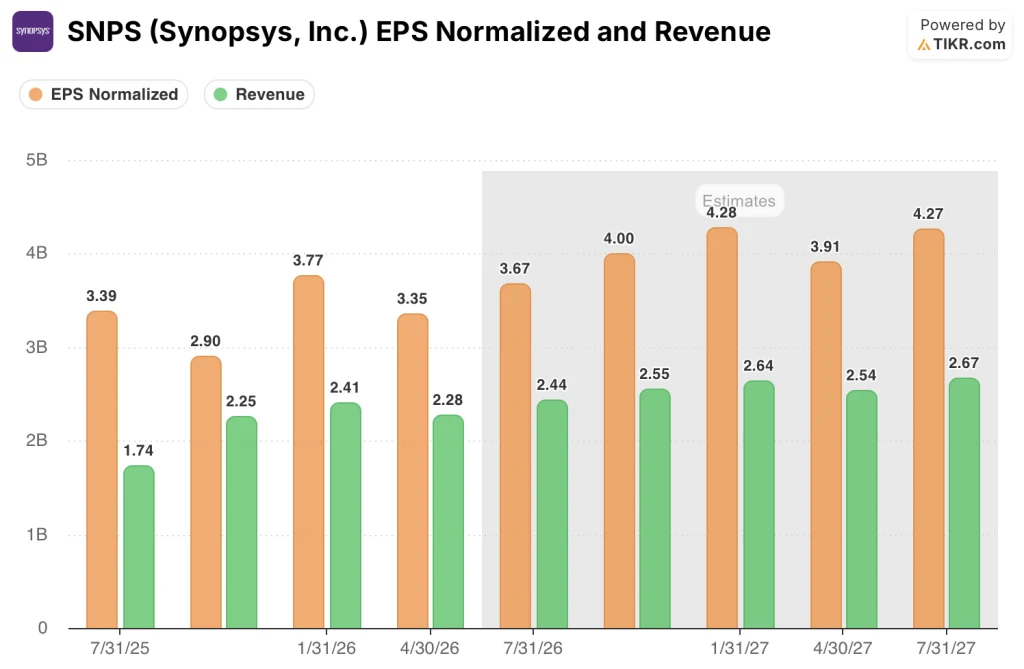

Total revenue came in at $2.276 billion for the quarter, above the $2.251 billion consensus estimate.

Adjusted EPS reached $3.35, a $0.20 beat against the $3.15 estimate, with non-GAAP operating margin at 39.5%, ahead of guidance.

Synopsys raised its full-year revenue guidance to a range of $9.625 billion to $9.705 billion, with a midpoint above the prior analyst consensus of $9.63 billion, and lifted full-year adjusted EPS guidance to $14.72 to $14.80 per share, well above the $14.45 estimate.

JPMorgan analysts called the raised outlook “conservative,” flagging meaningful room for further upside as AI-driven chip design demand continues to build.

The stock fell roughly 8.7% in the days following the report, a reaction that looks disconnected from the operating reality.

CEO Sassine Ghazi described the quarter as an “exceptional moment” for EDA as the go-to engineering solutions provider, and said in Q2 2026 earnings call that “AI is scaling semiconductor demand, architectural diversity and complexity of both chips and the systems they power, driving increased demand across our portfolio.”

Elliott Investment Management, which had built a multi-billion-dollar stake in Synopsys and publicly pushed for margin improvement and better financial execution, reached a cooperation agreement with the company on the same day, bringing Elliott managing partner Jesse Cohn onto the board as an independent director.

Synopsys stock has gained roughly 20% since Elliott’s involvement became public in March, but still trades below where the operating fundamentals suggest it should be.

The Design Automation segment, which includes EDA software and Ansys multiphysics simulation, generated around $1.822 billion in revenue for the quarter, with hardware-assisted verification emerging as the key growth driver across hyperscaler and leading semiconductor customers.

The Design IP segment reported $454 million in quarterly revenue, up 12% sequentially, confirming management’s long-standing call that Q1 represented the trough and that sequential improvement would follow through the back half of the fiscal year.

Backlog ended the quarter at $11 billion, and free cash flow came in at around $575 million for the period.

Why 25 Analysts Still Hold Buy Ratings on SNPS After the Post-Earnings Drop

Synopsys stock’s fiscal Q2 adjusted EPS of $3.35 beat the $3.15 estimate by 6.3%, and the forward picture only strengthens from there.

Consensus estimates call for quarterly EPS of around $3.67 in the July quarter and around $4.00 in the October quarter, putting the back half of fiscal 2026 well above the first half’s run rate.

Fiscal 2026 full-year EPS consensus sits at approximately $14.76 at the midpoint of company guidance, a figure management described as conservative given the pace of AI-related design activity.

The IP segment bottomed in Q1 2026 at $454 million and is expected to deliver sequential quarterly improvement through the remainder of the fiscal year, with the recovery anchored in hyperscaler demand for custom AI silicon and the early stages of a new royalty-based monetization model.

Revenue consensus for the July quarter stands at around $2.44 billion, a roughly 40% year-over-year increase that reflects the full consolidation of Ansys, and the Street is projecting around $2.55 billion for the October quarter.

The monetization inflection management is building toward, specifically the shift from subscription-only EDA licenses to a subscription-plus-consumption model as “agent engineers” begin operating Synopsys tools alongside human engineers, is expected to begin driving incremental revenue in fiscal 2027.

Of 26 analysts covering Synopsys stock, 15 rate it Buy and 2 rate it Outperform, with 7 Holds, 1 Underperform, and 1 Sell, reflecting overwhelming conviction on the AI-driven demand thesis with a minority cautious on valuation and near-term IP recovery pace.

The Street mean target is $560, implying roughly 20% upside from current levels, and the Street high target is $650, about 40% above where Synopsys stock trades today.

The verdict is straightforward: at $465, SNPS appears to be undervalued relative to what its own raised guidance, a recovering IP segment, and an Elliott-backed efficiency drive are pointing to.

SNPS Leads Cadence and Arm on Quarterly EPS, Yet Trades at a Discount to Its Own History

Synopsys stock generated quarterly EPS of $3.35 in the April quarter, more than 77% above Cadence Design Systems’ (CDNS) $1.89 for the same period and nearly six times Arm Holdings’ (ARM) $0.58.

Looking forward, the gap holds: consensus estimates put SNPS quarterly EPS at $3.67 for the July quarter and $4.00 for the October quarter, against Cadence estimates of $2.05 and $1.94 respectively and Arm estimates of $0.40 and $0.43.

Synopsys stock’s EPS lead over its two closest comparables is not narrowing — it is the most profitable company in the EDA and chip IP software complex on a per-share basis, and the selloff that followed its beat-and-raise quarter has only widened the gap between that earnings reality and the stock’s current pricing.

Is Synopsys Stock Undervalued in 2026? TIKR’s $840 Base Case Makes the Argument

TIKR’s base case values Synopsys at approximately $840 by October 2030, implying around 81% total return from the current price of $465, or roughly 14% annualized over approximately 4.4 years.

The model builds on revenue growth assumptions of around 11% annually and net income margins expanding to approximately 32% over the forecast period, both grounded in what management has guided and what analyst consensus supports for fiscal 2026 and beyond.

If revenue growth comes in at the low end of around 10% per year and margins stabilize at roughly 30%, the model produces a price of approximately $734 by the end of the decade, a total return of around 58% and an IRR of around 6% annualized. That is the scenario where IP monetization stalls and agentic EDA revenue takes longer than expected to materialize.

If the Elliott engagement drives margins toward the mid-40s as management has targeted and hyperscaler chip design activity continues accelerating, the high-end scenario points to approximately $1,253, a total return of around 170% and an IRR of around 13%.

The mid case rests on execution the company has already demonstrated: two consecutive quarters of margin beats, a raised full-year EPS guide that management called conservative, and an IP trough that is already behind it.

What Is the Price Target for Synopsys Stock?

The Street mean price target for Synopsys stock is $560, based on 26 analysts, implying roughly 20% upside from the current price of $465.

The Street high target is $650. TIKR’s base case model puts the long-term target at around $840 by October 2030, assuming around 11% annual revenue growth and expanding margins.

The key variable to watch is the pace of IP royalty monetization and agentic EDA contract uptake in fiscal 2027.

Is Synopsys Stock a Buy Right Now?

Synopsys stock looks undervalued at $465 relative to what the Q2 results demonstrated: a $0.20 EPS beat, a raised full-year adjusted EPS guide of $14.72 to $14.80, and an IP segment that management confirmed bottomed in Q1. Of 26 analysts covering SNPS, 17 rate it Buy or Outperform.

The near-term risk is that IP recovery takes longer than guided, but the Elliott cooperation agreement adds pressure to accelerate margin improvement and value capture.

Should You Invest in Synopsys, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Synopsys, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Synopsys, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SNPS stock on TIKR for Free →