Key Stats for UBER Stock

- 52-Week Range: $68 to $102

- Current Price: $71

- Street Mean Target: $104

- Street High Target: $150

- Analyst Consensus: 36 Buys / 9 Outperforms / 5 Holds / 0 Underperforms / 1 Sell

- TIKR Model Target (Dec. 2030): $155

Uber Stock Falls 30% From Its Peak Despite Q1 Results at the High End of Guidance

Uber Technologies (UBER) dropped to around $71 following its Q1 2026 earnings release, pulling the stock to within striking distance of its 52-week low despite reporting gross bookings of $53.7 billion, a 21% year-over-year increase that came in above the high end of management’s guidance range.

The selloff concentrated in Q1 revenue, which came in at $13.2 billion against a consensus estimate of roughly $13.3 billion, a miss of less than 1%.

That miss was structural, not operational: a UK business model change that Uber flagged in its prepared remarks reduced reported Q1 revenue growth by approximately 8 percentage points and is expected to continue dragging Mobility revenue margin by around 400 basis points through the remainder of 2026.

CEO Dara Khosrowshahi addressed the operational picture directly on the Q1 call: “Despite a complex backdrop marked by war and weather, we delivered top line and profitability at or above the high end of our guidance.”

The profitability story was not ambiguous: non-GAAP EPS reached $0.72, a 44% year-over-year increase, against a consensus estimate of $0.70, and trailing twelve-month free cash flow hit around $9.8 billion.

Uber’s Mobility segment, which covers ride-hailing globally, accelerated to 20% gross bookings growth with record segment operating margins.

Delivery, which includes Uber Eats across food, grocery, and retail, grew gross bookings 23% and maintained expanding margins, while Freight returned to growth for the first time in nearly two years.

The company also repurchased a record $3 billion in stock during Q1 alone, cutting its diluted share count 2% year over year.

Uber One, the company’s paid membership program, surpassed 50 million members and now accounts for over half of gross bookings across both Mobility and Delivery.

New partnership announcements layered on top: a robotaxi pilot in Madrid with WeRide and AVOMO, a Munich program with Autobrains and Nvidia, a commitment of close to $500 million to self-driving startup Nuro, and a $1 billion fleet financing facility with Banco Santander.

Autonomous vehicle trips on Uber’s platform grew more than 10 times year over year, and management reiterated a target to be live in up to 15 cities globally by the end of 2026.

UBER stock’s 30% decline from its 52-week high of around $102 happened while the underlying business was delivering, which is the tension the data does not support.

Why 45 of 51 Analysts Still Rate Uber Stock a Buy or Outperform After the Pullback

The consensus on Uber stock is not split: 36 analysts rate it a Buy, 9 rate it Outperform, 5 Hold, and 1 carries a Sell, for a combined 45 bullish ratings out of 51 covering analysts.

The mean price target of around $104 implies nearly 48% upside from the current price of around $71, and the Street high of $150 implies more than double from here.

That conviction is grounded in the EBITDA trajectory.

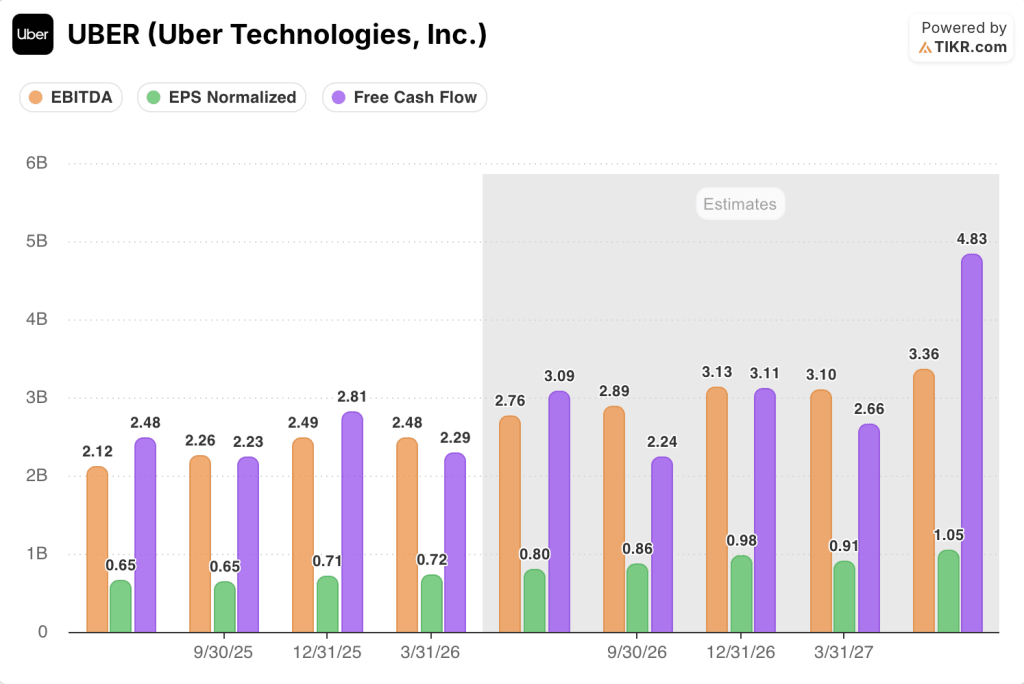

Uber stock’s Q1 EBITDA came in at $2.48 billion, a 32.8% year-over-year increase, with EBITDA margin expanding to 18.8% from around 17.3% in the prior quarter.

The Street projects Q2 EBITDA of around $2.76 billion, a 30% year-over-year increase, with margin expanding to roughly 19%.

The forward curve does not flatten: consensus estimates call for EBITDA of approximately $2.89 billion in Q3 and around $3.13 billion in Q4, with full-year 2026 EBITDA margin exiting the year near 20%.

Uber stock’s EPS Normalized came in at $0.72 for Q1, and the Street is modeling roughly $0.80 for Q2, a 22% year-over-year increase, rising to approximately $0.86 in Q3 and around $0.98 in Q4.

The forward free cash flow picture supports the buyback math: Q2 FCF is projected at around $3.09 billion, and the annual total is expected to approach around $11 billion across the four 2026 quarters.

At the Bernstein Strategic Decisions Conference, CFO Balaji Krishnamurthy framed the capital allocation hierarchy plainly: reinvest in organic growth first, fund the autonomous vehicle ecosystem second, pursue selective M&A third, and return excess capital to shareholders through buybacks fourth.

The Delivery Hero situation adds a wildcard: Uber has built an economic exposure of roughly 37% in the German food delivery company and is evaluating a full acquisition at a cost basis in the low 30s euros per share.

If a deal closes, it would add scale across Middle East and Korean Delivery markets where Uber currently has no Delivery presence, potentially lifting gross bookings from over $100 billion to over $160 billion annually.

The insurance cost tailwind is also running ahead of schedule: management guided for hundreds of millions in U.S. insurance savings in 2026, annual rate renewals came in at low single-digit increases in March, and trip growth in Los Angeles, the market with the steepest prior insurance headwinds, has reaccelerated meaningfully.

With 45 out of 51 analysts bullish, a mean target implying nearly 48% upside, and an EBITDA margin trajectory heading toward 20%, Uber stock is undervalued relative to what the fundamentals are actually delivering.

Is Uber Stock Undervalued in 2026? TIKR’s $155 Target Suggests Significant Upside

TIKR’s base case values Uber stock at approximately $155 by December 2030, implying around 119% total return from the current price of around $71, or roughly 19% annualized over approximately 4.6 years.

If Uber sustains revenue growth at around 11% per year and net income margins expand toward roughly 16%, the TIKR model projects a stock price near $214 by December 2034, implying around 203% total return and an IRR of roughly 14%.

If revenue growth falls closer to around 10% and margins come in nearer to roughly 15%, the low-case scenario still produces a stock near $161 by 2034, a total return of around 127% and an IRR of around 10%.

The high case, which assumes roughly 12% revenue growth and net income margins approaching 16%, projects around $278 per share by December 2034, implying around 293% total return and an IRR of roughly 17%.

The insurance savings flowing through U.S. Mobility margins, the Uber One membership flywheel growing 50% year over year, and AV trip volume scaling at 10x are the three operational mechanisms that could push execution toward the mid or high case.

The Delivery Hero acquisition, if completed at a reasonable price, adds a TAM expansion lever the current model does not fully incorporate.

Is Uber Stock a Buy Right Now?

With 45 of 51 analysts rating Uber stock a Buy or Outperform, a mean price target of around $104 implying nearly 48% upside, and TIKR’s base case pointing to roughly 119% total return by December 2030, the data tilts bullish.

The key variable to watch is U.S. Mobility margin expansion as insurance savings flow through and whether the Delivery Hero acquisition proceeds at a disciplined price.

What Is the Price Target for UBER Stock?

The Street mean target on Uber stock is around $104 per share, with the high end at $150. TIKR’s mid-case model extends the view to approximately $155 by December 2030.

All 51 covering analysts, with 36 Buys and 9 Outperforms, are pricing in meaningful upside from the current level of around $71.

Should You Invest in Uber Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Uber Technologies, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Uber Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UBER stock on TIKR for Free →