Key Fundamental Metrics for DIS Stock

- 52-Week Range: $92.19 to $124.69

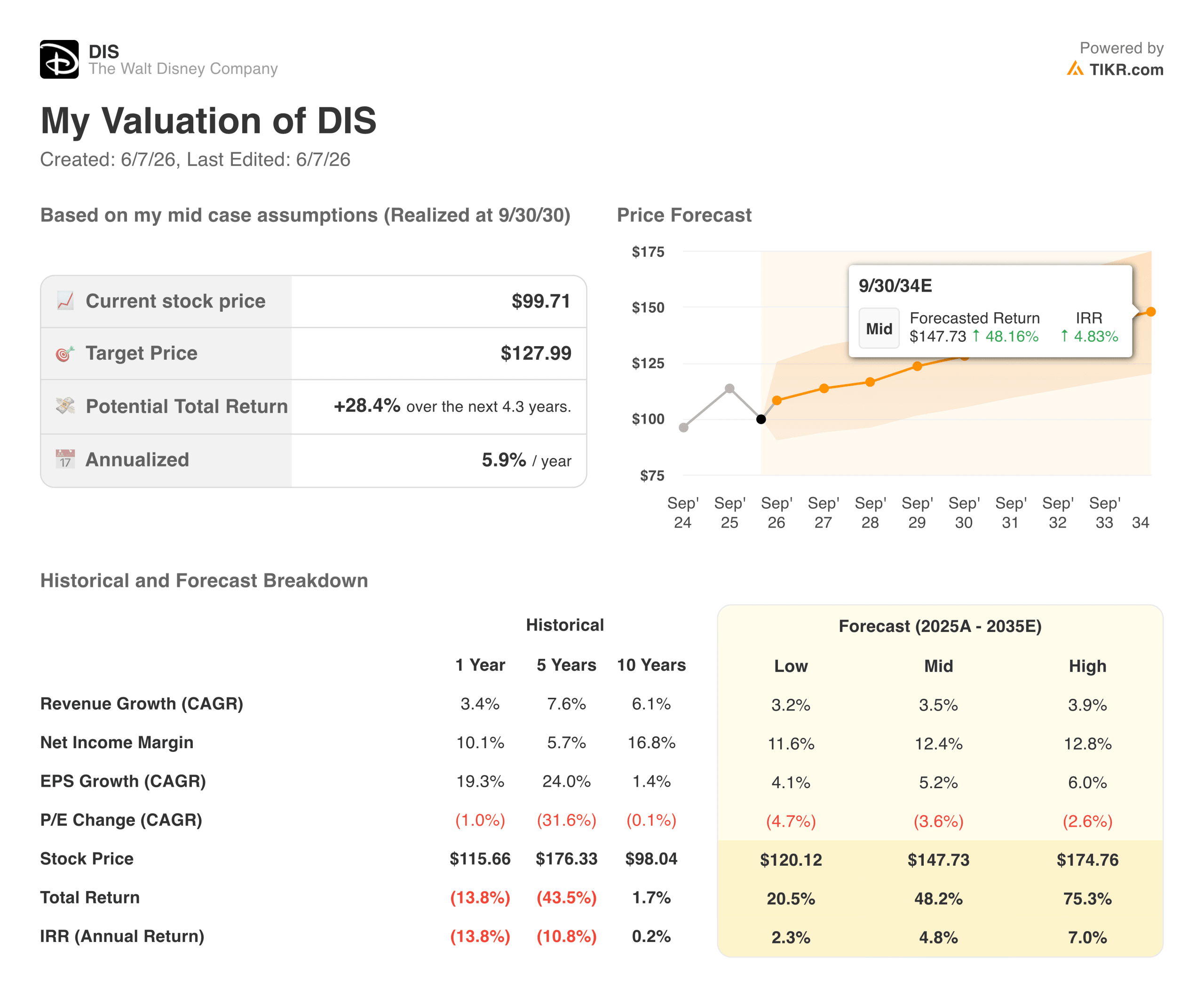

- Current Stock Price: $99.71

- Street Consensus Target Price: ~$130

- Q2 FY2026 Revenue: $25.2B (+7% YoY)

- Q2 FY2026 Adjusted EPS: $1.57 (+8% YoY)

- Q2 FY2026 Entertainment SVOD Operating Income: $582M (+88% YoY)

- FY2026 Adjusted EPS Guidance: ~+12% to +16%

- LTM Net Debt: $41.7B

- Mid-Case 10-Year Forward Stock Price Target: ~$148

Value your favorite stocks like DIS with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Three Businesses, One Transformation: What Disney Actually Looks Like in 2026

The Walt Disney Company (DIS) operates three distinct segments on different timelines, and understanding how they interact is the only way to evaluate the stock honestly.

Experiences, including theme parks, cruise lines, and consumer products, are the engine driving the business. Q2 revenue hit a record $9.5 billion, up 7%, with operating income up 5% to $2.6 billion. Per capita spending at domestic parks was up 5%. The Disney Adventure cruise ship launched in Singapore in March, and the World of Frozen opened at Disneyland Paris to a strong guest response.

Entertainment, which covers Disney+, Hulu, ABC, FX, and theatrical, is where the skepticism has lived. That skepticism is becoming harder to sustain. SVOD operating income reached $582 million in Q2, nearly doubling year over year, and Disney delivered its first double-digit Entertainment SVOD margin in the quarter. The content pipeline through fiscal 2027 includes The Mandalorian & Grogu, Toy Story 5, live-action Moana, and Avengers: Doomsday.

Sports, anchored by ESPN, is furthest along in its own structural transition. ESPN acquired NFL Network and NFL RedZone in January in exchange for a 10% noncontrolling interest, and digital subscriber revenue in Q2 more than offset secular declines in the linear subscriber base.

Total operating income grew from $3.7 billion in fiscal 2021 to $13.8 billion in fiscal 2025, while operating margins expanded from around 5% to nearly 15%. That is not the profile of a struggling media conglomerate.

It is the profile of a business that absorbed enormous streaming losses, digested the Fox acquisition, navigated a pandemic, and emerged with structurally higher margins than before any of it began.

See analysts’ growth forecasts and price targets for DIS stock (It’s free!) >>>

$18 Billion in Operating Cash Flow and an $8 Billion Buyback

Disney generated $5.6 billion in operating cash flow in fiscal 2021. By fiscal 2025, that number had reached $18.1 billion, more than tripling in four years. That trajectory is what makes the capital return commitments credible.

Management is targeting at least $8 billion in share repurchases in fiscal 2026 and has already deployed $5.5 billion in buybacks in the first half of the year alone. Disney carries $41.7 billion in net debt, which deserves honest acknowledgment, but at roughly 2x LTM EBITDA, it is a manageable load for a business generating cash at this scale.

See historical and forward estimates for Disney stock (It’s free!) >>>

What the TIKR Valuation Model Says About DIS at $100

TIKR’s mid-case valuation model targets around $148 for DIS over a roughly eight-year horizon, implying a total return of around 48% or about 5% annualized. The model assumes revenue growing at around 4% annually and net income margins expanding to around 12%. Those are conservative assumptions for a business guiding for 12% to 16% adjusted EPS growth in fiscal 2026 alone.

The low case is around $120, and the high case is around $175. The Street consensus of around $130 implies about 30% upside from current levels, which is considerably more constructive than the TIKR mid-case. That gap reflects what analysts expect from the streaming and ESPN DTC transitions as they mature over the next several years.

Worth noting: the mid-case assumes Disney delivers less than half the EPS growth it is currently guiding for. If the streaming profitability trajectory holds and ESPN’s DTC subscriber base builds meaningfully, the high case of around $175 becomes the more relevant reference point.

What the Bulls Are Betting On

- Streaming profitability is no longer a promise. SVOD operating income up 88% year over year, with a double-digit margin, is the milestone Disney investors have been waiting years for.

- Experiences has room to grow globally. A planned resort in Abu Dhabi, a new cruise ship for Japan, and the Disney Adventure in Singapore extend Disney’s physical footprint into markets with hundreds of millions of potential first-time guests.

- ESPN owns the most valuable live sports rights in the U.S. The NFL Network acquisition and Super Bowl LXI in February 2027 give ESPN an unmatched content offering at exactly the moment live sports consumption is migrating to streaming.

- The valuation is modest for the asset base. At roughly 13x NTM P/E on a business with $94 billion in annual revenue and $18 billion in operating cash flow, DIS is not priced for a successful transformation.

What the Bears Are Watching

- Revenue growth is modest. A forward two-year revenue CAGR of around 6% is not the profile that typically drives multiple expansion, even alongside margin improvement.

- $41.7 billion in net debt limits flexibility. The load is manageable but not invisible, and higher-for-longer rates increase carrying costs while reducing deployment speed.

- Domestic park attendance is soft. Attendance declined 1% in Q2, and management explicitly flagged macroeconomic uncertainty as a live headwind for the Experiences segment.

- ESPN DTC is early and expensive. The Unlimited plan launched only last August. Building a direct-to-consumer sports bundle while paying escalating rights fees is a multi-year investment with uncertain subscriber economics.

Access Professional Tools to Analyze TT stock on TIKR for Free →

Should You Invest in The Walt Disney Company?

Disney is one of those stocks where the gap between what the business is doing and what the market is pricing creates a genuinely interesting setup. Operating income has nearly quadrupled since fiscal 2021, cash from operations has tripled, and streaming has turned profitable. The stock trades nearly 20% below its 52-week high with a Street consensus implying around 30% upside.

The honest constraints are real: modest revenue growth, meaningful debt, and a softer domestic parks consumer. The TIKR mid-case of around $148 reflects patient compounding rather than dramatic upside.

For investors who believe the streaming inflection is durable and that ESPN’s DTC transition will eventually justify a higher multiple, the current price is a reasonable entry point into one of the most recognized businesses on earth.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!