Key Stats for Thermo Fisher Stock

- 52-Week Range: $385 to $644

- Current Price: $473

- Street Mean Target: $603

- Street High Target: $750

- Analyst Consensus: 18 Buy, 5 Outperform, 4 Hold

- TIKR Model Target (Dec. 2030): $725

Thermo Fisher Stock Beats Q1 Estimates, Raises Guidance, but Still Down 11% YTD

Thermo Fisher Scientific (TMO) delivered first-quarter 2026 revenue of $11.01 billion, beating the Street estimate of $10.85 billion, while raising its full-year adjusted EPS guidance to $24.64 to $25.12, up from its prior range of $24.22 to $24.80.

Adjusted EPS came in at $5.44, topping consensus of $5.24 by $0.20.

The company’s largest segment, Laboratory Products and Biopharma Services, grew approximately 7% to around $6.04 billion, with clinical research posting strong revenue and authorizations growth for another consecutive quarter.

The bioproduction business delivered what CEO Marc Casper described as a “phenomenal quarter,” with organic growth exceeding what most peers had reported.

Casper gave the sharpest characterization in Q1 2026 earnings call of why the stock’s setup looks different from the headline: “What I do know is our team is fully focused on offsetting it with all the levers. I believe that if it’s relatively modest, we will offset it all, and that will all flow through the bottom line.”

The company also completed the acquisition of Clario, a clinical trial endpoint data platform acquired for approximately $9 billion, which contributed $30 million of revenue and $0.01 of adjusted EPS in its first week of ownership; management described it as immediately accretive and on track for $0.32 of adjusted EPS contribution for the full year.

Thermo Fisher agreed to sell its microbiology business to private equity firm Astorg for approximately $1.08 billion, reflecting active portfolio management rather than distress.

The stock fell around 8% on earnings day despite the beat, driven by management’s acknowledgment that U.S. academic and government demand will not recover to normalized levels in 2026, combined with inflation risk tied to the Middle East conflict.

Thermo Fisher’s 2026 Investor Day in May reinforced the long-range case: management targets 7% organic revenue CAGR long-term, with a near-term path of 3% to 6% organic growth through 2027 before returning to that normalized rate in 2028 and beyond.

Why 25 Analysts Still Have a Buy on TMO Stock Despite the Academic Headwind

Thermo Fisher stock’s Q1 adjusted EPS of $5.44 came in $0.14 ahead of management’s own prior guidance, with $0.13 from operational outperformance and $0.01 from Clario.

The forward EPS trajectory is where the conviction is anchored: consensus estimates Q2 2026 adjusted EPS of around $5.72, up roughly 7% year over year, then around $6.37 in Q3 and around $7.34 in Q4, with the implied full-year exit rate pointing to a meaningful back-half acceleration.

That steepening curve is not speculative. It reflects contracted pharma services capacity coming online in the second half, a clinical research backlog that management described as ahead of organic growth, and a one-less-selling-day headwind in Q1 that reverses in Q4.

Meanwhile, TMO’s Q2 consensus revenue estimates around $12 billion, up roughly 8% year over year, with EBITDA margins expected to expand from 24.6% in Q1 to around 25% in Q2 as the selling-day headwind clears and pharma services mix begins to improve.

The Street’s concern has been whether the 3% to 4% organic growth guidance range is achievable given academic headwinds, and Jefferies articulated it plainly: “sluggish underlying demand growth and no clear signs yet of inflection in end-market conditions.”

JPMorgan holds the same “overweight” with a price target of around $600, but conceded end-market improvement “seems more gradual than initially hoped” before adding that TMO is “well positioned to gain share during recovery.”

Morgan Stanley, also overweight with a target around $670, noted the stock’s results offered little reassurance on the ability to meet guidance with increasing dependence on a stronger second-half performance.

HSBC moved in the other direction, cutting to hold and reducing its target to around $540, the only significant downgrade in recent weeks.

Against a current price around $473, the Street mean of approximately $603 implies around 27% upside; the Street high sits at $750, implying around 58% upside if the recovery thesis plays out ahead of expectations.

With 18 Buys, 5 Outperforms, and 4 Holds across 25 analysts who have submitted targets, the distribution reflects a consensus that the headwinds are real but priced, and the 8% post-earnings sell-off overshot the fundamental shift in the story.

Thermo Fisher looks stock is undervalued on the Street’s own math: a stock trading 27% below the average analyst target, with an EPS curve accelerating into the second half, in a company that just beat estimates and raised guidance, represents a pricing gap that the data does not support.

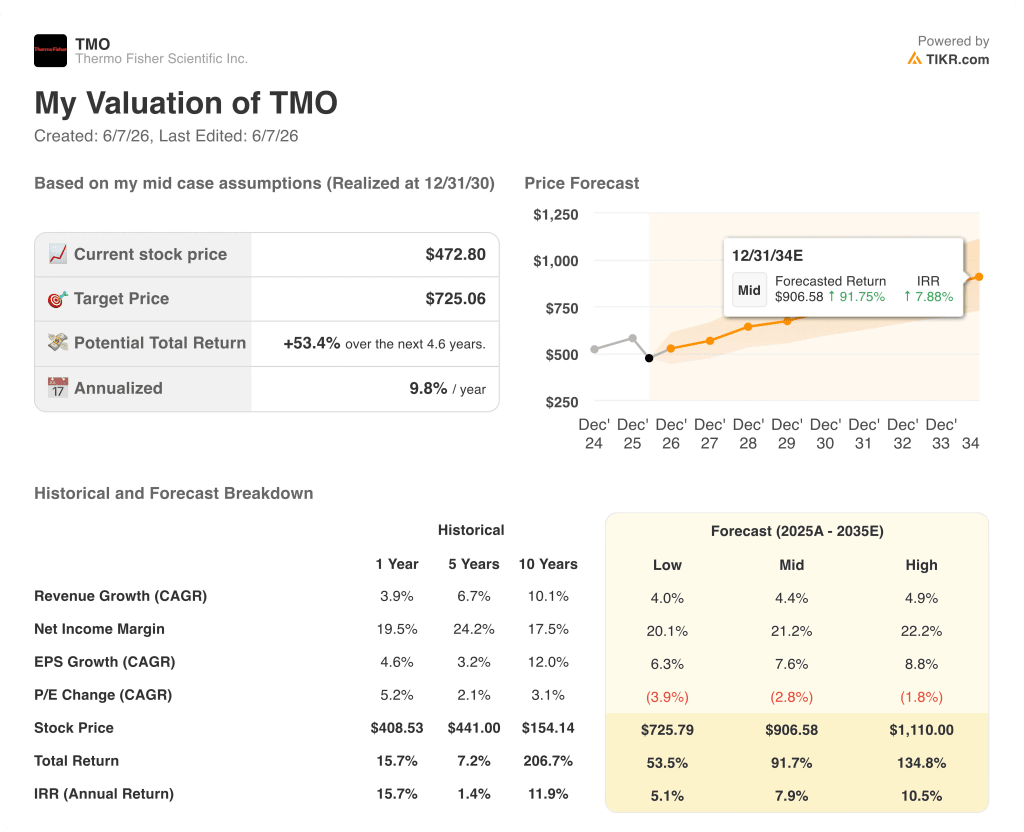

Is Thermo Fisher Stock Undervalued in 2026? TIKR’s $725 Mid-Case Says Yes

TIKR’s base case values Thermo Fisher Scientific at approximately $725 by December 2030, implying around 53% total return from the current price of approximately $473, or roughly 10% annualized over 4.6 years.

The model’s mid-case assumes approximately 4.4% revenue CAGR, net income margins around 21%, and EPS growth of approximately 8% per year, reflecting a gradual but durable recovery consistent with management’s own long-range guidance of 7% organic growth beyond 2027.

The low case, built on around 4% revenue CAGR and net income margins around 20%, prices TMO at approximately $726 by the same date with around 53% total return and roughly 5% annualized, implying very limited downside differentiation from the mid-case at current entry levels.

The high case, assuming approximately 5% revenue CAGR and net income margins around 22%, implies a stock price near $1,110, around 135% total return and roughly 11% annualized, driven by end-market normalization in academic and government, China pharma/biotech acceleration, and U.S. reshoring contracts converting to bioproduction revenue in 2027 and 2028.

The key condition in any scenario is pharma/biotech holding above 57% of revenue and delivering the contracted second-half pharma services acceleration management has already sold. If that capacity comes online and clinical research authorizations convert to revenue at the pace the backlog implies, the mid-case path requires no recovery in academic or government demand at all.

What is the price target for TMO stock?

The Street mean target for Thermo Fisher Scientific stock currently sits at approximately $603, with the high target at $750. Across 25 analysts, 18 have Buy ratings, 5 Outperform, and 4 Hold. TIKR’s mid-case valuation model places a December 2030 target at around $725.

Is Thermo Fisher Scientific stock a buy right now?

The majority of Wall Street analysts rate Thermo Fisher stock as a buy, pointing to an accelerating EPS trajectory in the second half of 2026, a strong clinical research backlog, and a bioproduction business growing ahead of peers. The primary risk is whether end markets improve gradually enough to meet the back-half organic growth ramp embedded in management’s full-year guidance.

Should You Invest in Thermo Fisher Scientific Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Thermo Fisher Scientific stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Thermo Fisher Scientific alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TMO stock on TIKR for Free →