Key Fundamental Metrics for MNST Stock

- 52-Week Range: $58.09 to $90.44

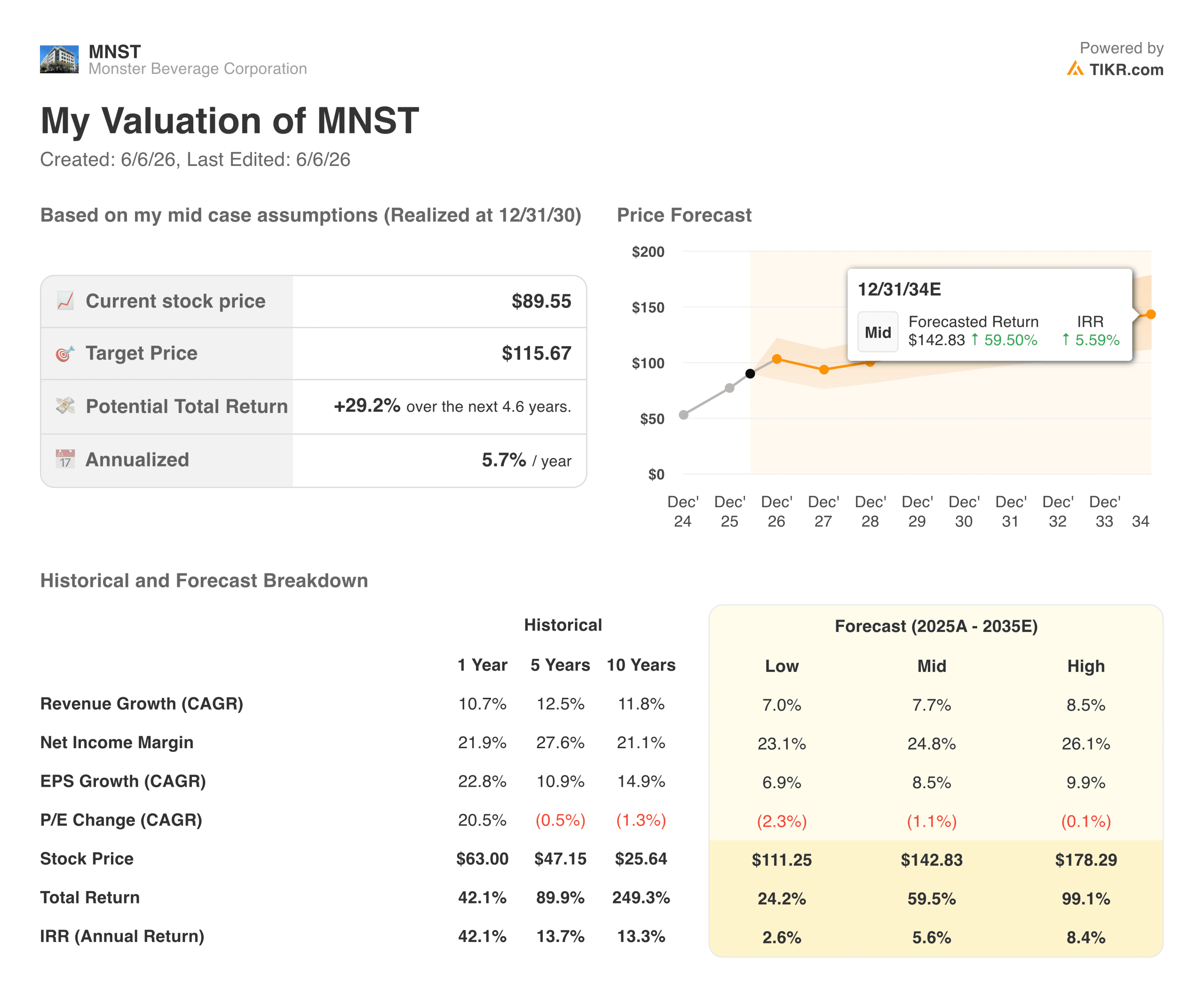

- Current Stock Price: $89.55

- Street Consensus Target Price: ~$89

- Q1 2026 Revenue: $2.35B (+27% YoY)

- Q1 2026 International Net Sales: $1.06B (+45% YoY)

- Q1 2026 Gross Margin: 55.0%

- Q1 2026 EPS: $0.58 (+27% YoY)

- Net Cash Position: $2.9B

- Mid-Case 10-Year Forward Stock Price Target: ~$143

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

$2 Billion in a Single Quarter: Monster’s International Engine Just Hit a New Gear

Monster Beverage (MNST) makes energy drinks. That description undersells what the business actually is: one of the most capital-efficient consumer brands ever built.

Monster doesn’t own manufacturing facilities or run a distribution network. It licenses its brand, contracts out production, and relies on Coca-Cola’s global bottling system spanning more than 150 countries to move product from factory to shelf. The result is a business that generates over 55% gross margins selling cans of energy drink, with $2.9 billion in net cash and no debt.

The Q1 2026 results captured a business that is accelerating rather than maturing. Net sales grew 27% year over year to $2.35 billion, the first time Monster has ever crossed $2 billion in a fiscal first quarter. International sales grew 45% to $1.06 billion, now representing 45% of total net sales, up from roughly 38% a year earlier.

China and India were called out specifically as high-growth markets where the Coca-Cola partnership is opening doors that smaller competitors simply cannot access.

The gross profit chart tells the margin story directly. Gross margins compressed sharply in 2022 to around 50% as aluminum can costs and freight surged in the post-pandemic supply chain environment. Since then, margins have recovered steadily to nearly 56% in 2025 as input costs have normalized and pricing initiatives have taken hold.

The Q1 2026 gross margin of 55.0% came in slightly below the prior year’s 56.5%, reflecting the growing weight of international markets in the revenue mix, where margins are structurally lower than domestic. That is the central tension, bulls and bears are working through right now.

Analyze your favorite stocks like Monster Beverage with TIKR (It’s free) >>>

The International Opportunity Is Real, but It Comes With a Margin Trade-Off

International markets are growing faster than domestic markets, driving revenue acceleration. But they also carry lower margins due to higher freight costs, local pricing dynamics, and the economics of building distribution in emerging markets. As international revenue grows as a share of total revenue, gross margin faces structural pressure even as gross profit dollars compound.

Monster has been navigating this through pricing. The company implemented increases across multiple markets over the past two years, and the recovery from the 2022 trough to nearly 56% in 2025 demonstrates real pricing power. Whether that holds as the business scales deeper into India and China, where competitive dynamics differ from those in the U.S., will be answered over the next several quarters.

On the capital return side, Monster repurchased approximately 1.4 million shares for around $101 million in Q1 and retains around $400 million under its existing authorization. The $2.9 billion net cash position gives management flexibility to continue returning capital while funding international expansion.

Normalized EPS dipped from $1.29 in 2021 to $1.12 in 2022 during the margin compression period, then recovered steadily to $1.99 in 2025. Street estimates project acceleration from here, reaching around $2.29 in 2026 and climbing toward $2.59 in 2027 and $2.93 in 2028.

That trajectory reflects revenue growth, recovering margins, and a declining share count from ongoing buybacks. The Q1 EPS of $0.58 puts the full-year 2026 estimate well within reach after just one quarter.

See the exact moment Wall Street upgrades a stock before the rest of the market piles in — track analyst rating changes in real time with TIKR for free →

What the TIKR Valuation Model Says About MNST at $90

TIKR’s mid-case valuation model targets around $143 for MNST over a roughly nine-year horizon, implying a total return of around 60% or about 6% annualized. The model assumes revenue growing at around 8% annually, net income margins expanding to around 25%, and EPS growing at roughly 9% per year.

The low case is around $111, and the high case is around $178. The Street consensus of around $89 sits almost exactly at the current price, meaning the average analyst sees MNST as fairly valued today. The TIKR mid-case is more constructive because it runs out a full decade, allowing the international compounding to accumulate over time.

What the Bulls Are Betting On

- The international runway is genuinely long. Monster is in the early innings of markets like India, Southeast Asia, and parts of Africa, where young demographics and rising incomes support decades of energy drink adoption.

- The Coca-Cola partnership is unduplicable. No competitor can replicate instant access to Coca-Cola’s global cold-chain bottling infrastructure, and that advantage compounds as international growth.

- The balance sheet funds optionality. $2.9 billion in net cash with no debt means Monster can sustain buybacks, pursue acquisitions, or absorb input cost cycles without financial stress.

- Margins have shown they can recover. The move from 50% in 2022 back to nearly 56% in 2025 demonstrates durable pricing power even through significant commodity headwinds.

What the Bears Are Watching

- Aluminum and freight remain live risks. Input costs normalized from their 2022 peak but haven’t disappeared. Any renewed commodity cycle would hit margins before pricing adjustments could catch up.

- The Street sees no upside at current levels. A consensus target at the stock price means most analysts believe the Q1 beat is fully priced in, limiting near-term catalyst potential.

- International mix will continue to pressure gross margins. The fastest-growing revenue stream carries structurally lower margins, making the path back to 56%+ harder even if domestic pricing holds.

- The valuation is not cheap for a beverage company. At around 38x NTM P/E, Monster is priced for sustained double-digit earnings growth, with limited tolerance for any international slowdown.

Should You Invest in Monster Beverage?

Monster is one of the most elegantly constructed consumer businesses in the public markets. The asset-light model, the Coca-Cola distribution moat, the $2.9 billion cash position, and a brand gaining global market share make the quality case nearly self-evident.

The honest constraint is that the market knows all of this. A consensus target at the current price means investors are paying fair value, not a discount, for a business growing at 27%. The TIKR mid-case of around $143 reflects what patient compounding over a decade produces, and for long-term investors who believe international expansion will continue without meaningful margin deterioration, that is a compelling destination.

For those who prefer to buy quality at a discount, waiting for a pullback would be the more disciplined approach.

Value Monster Beverage instantly (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!