Key Stats for Paypal Stock

- 52-Week Range: $38 to $80

- Current Price: $41

- Street Mean Target: $51

- Street High Target: $147

- Analyst Consensus: 5 Buys, 3 Outperforms, 32 Holds, 1 No Opinion, 4 Sells

- TIKR Model Target (Dec. 2030): $66

PayPal Brings In a New CEO, Restructures Around Three Businesses, and Commits to $1.5 Billion in Cost Cuts

PayPal Holdings (PYPL) closed at around $41 on June 5, 2026, near its 52-week low of around $38, after a first quarter that beat guidance while a new chief executive simultaneously reset the company’s entire operating model.

The stock has been cut nearly in half from its 52-week high of near $80.

Enrique Lores, the former HP CEO who joined PayPal’s board in 2021, took the CEO seat in early 2026 and spent his first 90 days on a structured diagnostic: two trips to the U.K., one to Germany, listening sessions with top merchants, and a review that concluded PayPal had spent years over-indexing on the merchant side of its two-sided network at the expense of the consumer side.

His diagnosis translated directly into action.

On April 29, PayPal announced a three-business operating model: Checkout Solutions and PayPal, Consumer Financial Services and Venmo, and Payment Services and Crypto — each with a single accountable leader replacing the four-dimensional matrix structure that Lores described as ungovernable.

The reorganization targets at least $1.5 billion in gross run-rate cost savings over two to three years, split between structural delayering in the first wave and AI-driven automation in the second, with AI accounting for roughly 40% of the total.

Q1 results, reported on May 5, gave the new plan a credible foundation to build on: total payment volume of around $464 billion, up around 11% year-over-year on a spot basis; revenue of around $8.35 billion, up around 7%; non-GAAP EPS of $1.34; and adjusted free cash flow of around $1.7 billion for the quarter, putting the trailing 12-month total at nearly $6.8 billion.

Venmo posted its sixth consecutive quarter of double-digit TPV growth at around 14%, and buy now, pay later volume grew around 23% year-over-year.

Lores framed the consumer underinvestment in plain terms on the Q1 call: “PayPal is a consumer company that has distribution through merchants. The way we were managing the business until now, it was like if Procter and Gamble were only concerned about having their products in the stores and there was zero effort to drive demand from a consumer perspective.”

The comparison is pointed, and it implies a specific fix: PayPal already has the merchant distribution. The missing investment is in pulling consumers through it.

That investment is now underway, with a loyalty program launched in the U.K. and a technology modernization program that PayPal’s CTO Srini Venkatesan detailed at the Evercore Global TMT Conference on June 3.

Why Analysts Hold PYPL Stock Despite a 24% Implied Upside to the Street Mean

The analyst consensus on PayPal stock reflects exactly what you would expect for a large-cap turnaround in the middle of its first chapter: 32 Holds dominating, with only 5 Buys and 3 Outperforms against 4 Sells.

The Street mean target sits at around $51, implying roughly 24% upside from the current price of around $41, with the high target reaching around $147.

The Hold cluster is not a verdict on the business — it is a verdict on timing.

Analysts are watching branded checkout TPV growth, currently running at the low end of the company’s slightly positive to low single-digit full-year guide, and waiting to see whether Lores can reaccelerate it before upgrading their rating.

The Q2 guide gave them additional reason for patience: non-GAAP EPS is expected to decline by roughly 9% year-over-year, with transaction margin dollars down around 3%, as the prior year’s second quarter carried a 1.5-point benefit from a key payment partner renewal that does not recur.

The EPS trajectory for the second half looks more supportive, with consensus estimates at $1.33 for Q3 2026 and $1.35 for Q4, both above Q2’s $1.28 estimate.

The year-over-year EPS comparison understates the compounding at work: PayPal retired 28 million shares in Q1 alone, cutting the count from 920 million to 892 million, and the full-year buyback commitment is around $6 billion, meaning EPS growth will run ahead of operating growth regardless of how branded checkout trends in the near term.

The risk the bears hold is real: Lores has committed to a multi-year transformation, the technology migration from Oracle to cloud-native infrastructure will take at least two years by Venkatesan’s own estimate, and Europe is showing macro softness in travel that pressured Q1 branded checkout trends into May.

The catalyst the bulls are watching is the second half of 2026, when year-over-year comparisons ease, the first wave of cost savings begins flowing through, and Lores presents the full scope of the transformation roadmap with new KPIs per business line.

PayPal Stock Earns More Per Share Than Block and Less Than Mastercard — the Gap to MA Is the Story

PayPal’s normalized EPS of $1.34 in Q1 2026 sits well above Block’s $0.68 for the same period, confirming that the two companies are at different stages of their earnings maturity curves despite occupying overlapping digital payments territory.

Block’s forward EPS estimates show faster percentage growth, reaching around $1.21 by Q1 2027 from a $0.68 base, but PayPal stock generates that figure from a standing start at nearly double Block’s current per-share earnings.

Mastercard’s trajectory is the relevant contrast for valuation purposes: MA printed $4.41 in Q1 2026 and consensus has it reaching around $5.60 by Q1 2027, a scale of per-share earnings that reflects the network-economics premium the market assigns to a pure payment network versus PayPal’s more operationally complex two-sided model.

PayPal’s EPS estimate of around $1.45 for Q1 2027 shows the buyback compression and cost savings beginning to accumulate — but the gap to Mastercard’s earnings trajectory is the reason PayPal stock trades where it does, and closing that gap on a per-share basis is precisely what the $6 billion annual repurchase program and $1.5 billion cost reduction are designed to do.

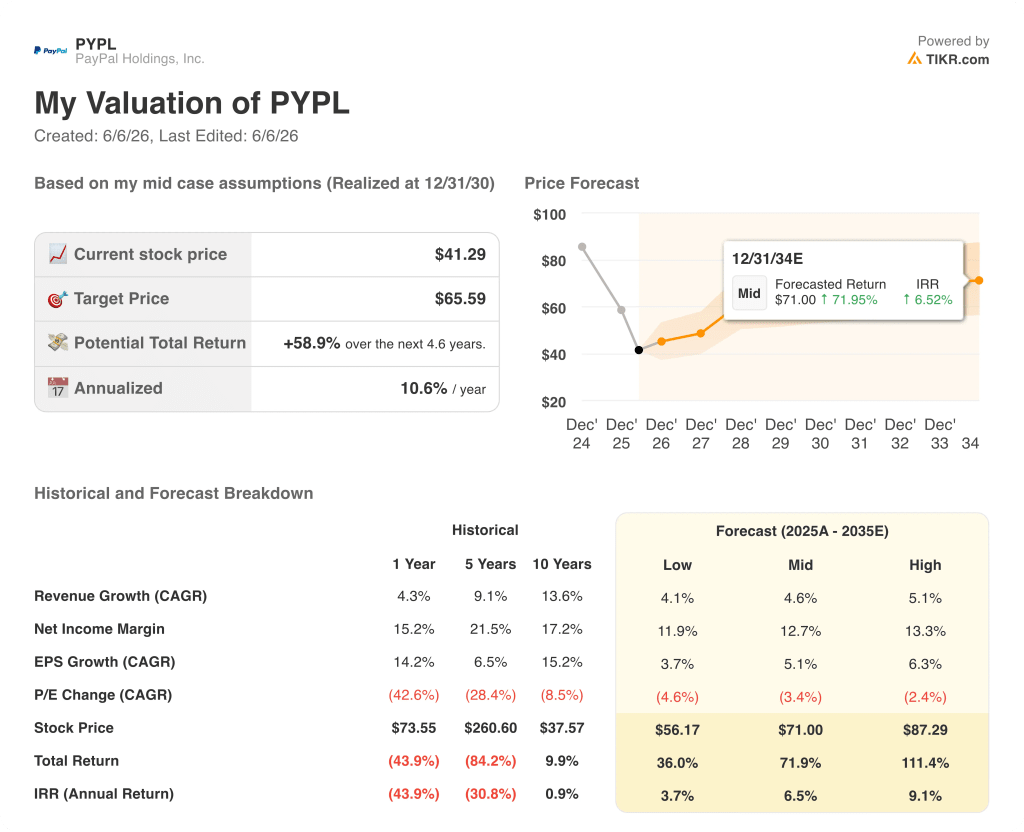

Is PayPal Stock Undervalued in 2026? TIKR’s $66 Model Points to a 59% Return by 2030

TIKR’s base case values PayPal at approximately $66 by December 2030, implying around 59% total return from the current price of around $41, or roughly 11% annualized.

If Lores’s transformation delivers the mid-case assumptions — around 4.6% revenue CAGR through 2035 with net income margins stabilizing near 13% — the TIKR model reaches around $66, and PYPL stock is undervalued at current prices by that measure.

The low case, producing around $56 and roughly 36% total return at around 4% annualized, reflects a scenario where branded checkout stagnation persists, Europe does not recover, and the cost savings program runs behind schedule.

The high case, reaching around $87 and roughly 111% total return at around 9% annualized, requires roughly 5% revenue CAGR with net income margins expanding toward 13%, a scenario that becomes available if the AI automation program and Venmo monetization both accelerate faster than the base assumptions.

The condition separating mid from high is not speculative: it is the attach rate of value-added services to Braintree’s enterprise processing volume, which Venkatesan flagged at Evercore as the single biggest near-term commercial lever PayPal has full operational control over.

Is PayPal stock a buy right now?

PayPal stock trades at around $41, roughly 24% below the Street mean target of around $51 and around 38% below TIKR’s base-case model target of approximately $66.

The analyst consensus is dominated by 32 Holds, with 5 Buys and 3 Outperforms, reflecting execution uncertainty under a new CEO rather than a negative view of the underlying FCF business.

The TIKR model implies roughly 11% annualized return on the mid case through 2030, which makes PYPL stock potentially attractive for investors willing to wait through the transformation cycle.

What do analysts say about PayPal stock?

As of June 5, 2026, 34 analysts cover PYPL with a mean price target of around $51 and a high target of around $147.

The consensus is 5 Buys, 3 Outperforms, 32 Holds, 1 No Opinion, and 4 Sells.

The Hold majority reflects a wait-and-see posture on branded checkout reacceleration and new CEO Enrique Lores’s $1.5 billion cost transformation rather than bearish conviction on the business fundamentals.

Should You Invest in PayPal Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PayPal Holdings, Inc. stock and you will see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PayPal Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PYPL stock on TIKR for Free →