Key Stats for Booking Holdings Stock

- 52-Week Range: $150 to $234

- Current Price: $166

- Street Mean Target: $224

- Street High Target: $298

- Analysts Consensus: 24 Buy, 6 Outperform, 7 Hold

- TIKR Model Target (Dec. 2030): $335

Booking Holdings Stock Falls 25% From Peak as Middle East War Clouds a Business Still Compounding Underneath

Booking Holdings (BKNG), the world’s largest online travel platform with over 1.3 billion room nights booked annually across Booking.com, Priceline, Agoda, KAYAK, and OpenTable, is now trading near a 52-week low after the U.S.-Israel attack on Iran in late February triggered a cascade of travel disruptions that has weighed on the stock through June.

The Middle East conflict, which erupted at the end of February, directly cut Q1 room night growth by roughly 2 percentage points, pulling the quarterly figure to 6% year-over-year on 338 million room nights booked.

Q1 revenue still rose 16% year-over-year to $5.53 billion, slightly above the consensus estimate of $5.52 billion, and adjusted EBITDA grew 19% to approximately $1.3 billion, exceeding the high end of guidance.

Adjusted EPS came in at $1.14, beating the Street’s $1.08 estimate and rising 14% from the prior year’s $0.99.

The quarter also included a record $3.6 billion in share repurchases, the largest single-quarter buyback in Booking Holdings’ history, funded partly by approximately $3.1 billion in free cash flow generated during the period.

But the stock’s decline is about the forward picture, not the Q1 beat: management lowered its full-year revenue growth outlook from low double-digits to high single-digits, assuming the conflict’s direct and indirect impact persists through the end of June before a recovery in the second half.

For Q2, the company guided room night growth to 2% to 4%, with revenue, gross bookings, and EBITDA each in the 4% to 6% growth range, assuming approximately 3 percentage points of headwind from the conflict.

CFO Ewout Steenbergen was explicit about what the company is not pricing in and stated on Q1 2026 earnings call: “We are mindful that a sustained disruption could introduce broader inflationary pressures, including fluctuations in jet fuel prices, airline capacity reductions, as well as weigh on traveler sentiment more broadly.”

Away from the conflict zones, the underlying demand picture looks entirely different: intra-European travel was up high single-digits, intra-Asia travel was up low double-digits, and U.S. room night growth accelerated to the low-teens for the fourth consecutive quarter.

That U.S. acceleration is being driven by direct bookings, with Booking.com’s U.S. direct channel posting double-digit growth and total B2C direct mix holding steady in the mid-60% range globally.

Beyond accommodations, flights grew 28% year-over-year in Q1, attractions grew approximately 25%, and Connected Trip transactions, bookings that span more than one travel vertical, grew in the high-teens, roughly three times faster than Booking.com’s total transaction growth.

Priceline also launched the next generation of its Penny AI assistant in early June, integrating Anthropic’s Claude into Priceline’s proprietary AI stack, with early tests showing higher engagement and conversion among Penny users and fewer customer support contacts.

On the regulatory side, Booking.com’s Preferred Partner program is under investigation by Italy’s antitrust regulator, which alleges that better search placement is tied to commission rates rather than quality, and the company confirmed it is cooperating with the inquiry.

BKNG also priced EUR 1.9 billion in senior notes across three tranches in May, alongside a separate $750 million senior notes offering, raising capital while maintaining its stated target leverage ratio of approximately 2x through the cycle.

The FIFA World Cup, running from June 11 through July 19 across the U.S., Canada, and Mexico, adds a near-term demand catalyst: B. Riley estimates 13.1 million visitors and 21.3 million room nights generated through online travel platforms, with Booking Holdings among the named direct beneficiaries.

BKNG Has 30 Buy-Equivalent Ratings. The War Cut Targets. The EBITDA Trajectory Did Not Move.

Booking Holdings stock entered 2026 as one of the most widely covered compounders in consumer internet, and the Middle East conflict produced something the stock rarely sees: a widespread round of target cuts from nearly every major bank, executed on the same day, with almost no rating downgrades underneath them.

Following the Q1 print on April 28, price target reductions came from Deutsche Bank, BMO, Citi, Evercore, HSBC, JPMorgan, Mizuho, Piper Sandler, RBC, TD Cowen, UBS, Barclays, Oppenheimer, and Wells Fargo, while only Wells Fargo actually raised its target (to $215, from $214).

Not a single firm downgraded to Sell. Piper Sandler, with the lowest target on the Street at $195, maintained its neutral rating while acknowledging BKNG is “a great business and long-term EPS compounder of 15%+.”

BTIG, with a buy rating and a $250 target, put the consensus view plainly: “We don’t see any impairment to the business here with solid traction on strategic initiatives, strength in the U.S. and healthy RoW trends ex-Middle East.”

The EBITDA estimates table shows why: for Q2 2026, consensus estimates EBITDA of approximately $2.55 billion, up around 5% year-over-year, and the trajectory recovers meaningfully through the back half, with Q3 consensus at approximately $4.61 billion (up around 9%) and Q4 at approximately $2.45 billion (up around 12%).

Booking Holdings stock’s full-year 2026 EBITDA consensus implies a business that absorbs a 4-month conflict and still expands earnings through margin discipline and scale benefits.

The long-term compounder framing held at every conference, too: at the Barclays Americas Select in May, Steenbergen reiterated the 8-8-15 framework: at least 8% constant currency gross bookings growth, at least 8% revenue growth, and at least 15% adjusted EPS growth for future years.

Revenue consensus for Q2 stands at approximately $7.17 billion (up around 6%), recovering to approximately $9.74 billion in Q3 (up around 8%) and approximately $6.89 billion in Q4 (up around 9%).

With 24 Buys, 6 Outperforms, and 7 Holds against zero Sells, and a Street mean target of around $224 against a current price of $166, the analyst community is pricing BKNG stock as deeply undervalued relative to its medium-term earnings trajectory, with the war representing a headwind that pulls 2026 estimates down rather than an impairment that changes the structure of the business.

The one variable with no clean answer is duration: management has assumed 4 months of conflict impact, but Fogel acknowledged on the earnings call that “we don’t know when, but it will end” and noted the business has absorbed 9/11, the financial crisis, COVID, and the Russia-Ukraine war without lasting damage to the long-term demand trajectory.

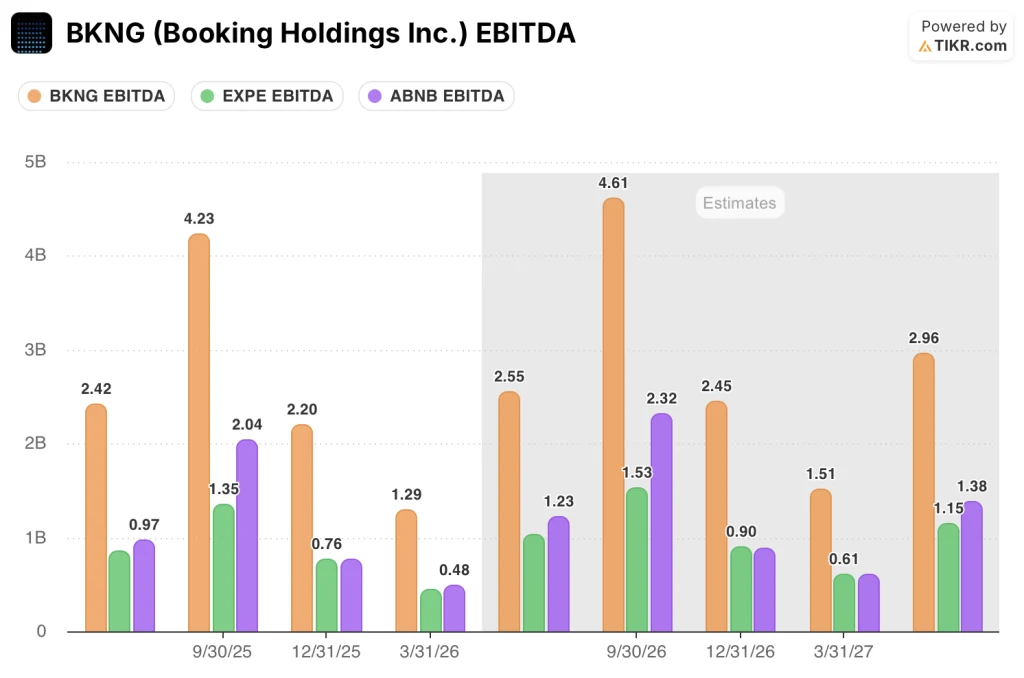

BKNG Generates More EBITDA in One Quarter Than Expedia and Airbnb Combined

Booking Holdings stock’s EBITDA advantage over its two closest peers is not a rounding error, it is a structural gap that the current discount does not reflect.

In Q3 2025, the most recent comparable peak-season quarter, BKNG produced $4.23 billion in EBITDA against Airbnb’s (ABNB) $2.04 billion and Expedia’s (EXPE) $1.35 billion, meaning Booking Holdings generated more earnings than both peers combined in the same period.

The gap persists into the trough: in Q1 2026, BKNG delivered $1.29 billion in EBITDA while Airbnb came in at $0.48 billion and Expedia at $0.27 billion, a ratio that holds roughly consistent across the cycle and signals that BKNG’s scale advantage is not seasonal.

Looking forward, the distance does not compress: consensus estimates BKNG’s Q3 2026 EBITDA at approximately $4.61 billion against Airbnb’s approximately $2.32 billion and Expedia’s approximately $1.53 billion, suggesting the market expects Booking Holdings to widen its absolute EBITDA lead even through a year with a 4-month conflict headwind.

Is Booking Holdings Stock Undervalued in 2026? TIKR’s $335 Target Answers Directly.

TIKR’s base case values Booking Holdings at approximately $335 by December 2030, implying around 102% total return from the current price of $166, or roughly 17% annualized over 4.6 years.

The scenario breakdown tells the rest of the story. If revenue grows at around 8% annually through 2030 with net income margins near 31% and EPS compounding at around 14% per year (the mid case), BKNG stock reaches approximately $548 by December 2034 for a total return of around 231% and an IRR near 15%.

If growth comes in lighter, around 7% revenue CAGR with margins near 29%, the low case produces a stock price of approximately $415 and an IRR of around 11%.

If execution accelerates with an 8.5% revenue CAGR and margins expanding toward 32%, the high case produces approximately $708 and an IRR near 18%.

All three scenarios share the same starting assumption: the Middle East conflict is temporary, which management has modeled, the analyst community has accepted, and which the acceleration in U.S. room night growth, intra-European bookings, and Connected Trip adoption all corroborate in the underlying data.

The risk is not that the thesis is wrong. It is that the conflict extends into the second half or that jet fuel prices and airline capacity reductions create secondary demand destruction that management has explicitly not modeled into guidance.

Is Booking Holdings stock a buy right now?

With 30 buy-equivalent ratings out of 37 analysts and a Street mean target around $224 against a current price of $166, the consensus view is that BKNG stock is a buy.

TIKR’s base case adds a longer-horizon data point: approximately $335 by December 2030, implying around 17% annualized return. The risk is conflict duration, not business quality.

What is the price target for BKNG stock?

The Street mean target for BKNG stock is approximately $224, around 35% above the current price of $166. The Street high target is $298.

Individual targets range from $195 at the low end (Piper Sandler) to $298 at the high end (HSBC), with the bulk of coverage clustered between $210 and $250 following the round of post-Q1 target reductions.

Should You Invest in Booking Holdings Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Booking Holdings Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Booking Holdings Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BKNG stock on TIKR for Free →