Key Stats for Vistra Stock

- 52-Week Range: $133 to $220

- Current Price: $149

- Street Mean Target: $225

- Street High Target: $320

- Analyst Consensus: 14 Buys, 4 Outperforms, 1 Underperform, 1 Sell

- TIKR Model Target (Dec. 2030): $156

Vistra Stock Posts Record Q1 EBITDA as the AI Demand Story Moves from Thesis to Actuals

Vistra Corp (VST), the largest competitive power generator in the United States, delivered approximately $1.49 billion in adjusted EBITDA for Q1 2026, a record for any calendar first quarter in the company’s history, driven by higher realized energy and capacity prices and the contribution from assets acquired through the Lotus deal in late 2025.

Revenue came in at $5.64 billion, up roughly 43% year over year from $3.93 billion in the same quarter a year earlier, even as mild weather in Texas pulled against retail results.

The Texas segment, which captures ERCOT generation, posted adjusted EBITDA of around $586 million for the quarter, up more than 19% year over year.

The East segment, covering PJM and New England, rose roughly 56% year over year and contributed around $801 million.

Vistra stock climbed after the print, with Reuters noting the shares gained more than 5% in premarket trading on the day of the earnings release.

CEO Jim Burke framed the result in a statement in Q1 2026 earnings call as proof of concept for the integrated model: “Despite those conditions, our generation team performed very well during Fern with our natural gas fleet performing at 97% commercial availability and our nuclear fleet at 100%.”

The company reaffirmed its 2026 adjusted EBITDA guidance range of $6.8 billion to $7.6 billion and its adjusted free cash flow before growth guidance of $3.93 billion to $4.73 billion.

That guidance excludes any contribution from the pending acquisition of the 5,500-megawatt Cogentrix natural gas portfolio, which targets a second-half 2026 close, and any uplift from the 20-year power purchase agreements with Meta at Vistra’s PJM nuclear sites.

With approximately $525 million deployed in share repurchases through the first four months of 2026 and around $75 million in common dividends, the company has already returned approximately $600 million to shareholders this year.

Both Fitch and S&P now rate Vistra’s corporate credit at investment grade, a milestone that triggered the release of liens under its senior secured debt agreements.

Load growth projections remain conservative by design: management targets 5% to 6% annual growth in ERCOT through 2030 and 2% to 3% in PJM, figures Burke described as “below many third-party forecasts and ISO projections” but consistent with the physical pace of development.

Why 18 of 20 Analysts Are Bullish on Vistra Stock Despite the Pullback from Highs

The analyst community has not flinched despite Vistra stock sitting roughly 32% below its 52-week high of $220.

The current consensus is 14 Buys and 4 Outperforms against 1 Underperform and 1 Sell, with a mean price target of approximately $225, implying roughly 51% upside from the current price.

The Street high target sits at $320, and even the mean target represents a substantial premium to where Vistra stock trades today.

The bull case rests on EBITDA compounding through a structurally improved power demand environment anchored by AI data centers, electrification, and a conservative hedging posture that has locked in a significant portion of expected generation through year-end 2027.

Forward EBITDA estimates show consistent expansion: consensus projects approximately $1.76 billion for Q2 2026, roughly $2.06 billion in each of Q3 and Q4 2026, and approximately $1.73 billion in Q1 2027, putting the full-year 2026 EBITDA trajectory well within the reaffirmed guidance range.

That trajectory carries a year-over-year growth rate of approximately 32% for Q2 2026 and roughly 32% for Q3 2026, reflecting the contribution from Lotus assets and accelerating capacity revenue in PJM.

Revenue estimates follow the same path, with consensus modeling approximately $5.77 billion in Q2 2026 and roughly $7.10 billion in Q3 2026, representing approximately 36% and roughly 43% year-over-year growth, respectively.

What the Street is watching most closely is not whether the base business can hit guidance, which the hedging program largely secures, but whether Cogentrix and the Meta PPA adds to the growth algorithm above the reaffirmed range.

Management signaled line of sight to more than $10 billion of cash generation over 2026 and 2027 combined, with approximately $3 billion earmarked for equity returns, around $4 billion for growth investments, and a remaining approximately $3 billion available for further capital allocation through year-end 2027.

The bears’ argument is simpler: ERCOT forward curves have softened, batteries have increased supply in the near term, and the pace of large load hook-ups remains slower than consensus had priced.

But with investment-grade ratings from two agencies, a fully hedged 2026 book, and PPAs and acquisitions excluded from guidance that could move the mid-point higher at closing, the weight of the evidence keeps the majority on the buy side.

The Street verdict on Vistra stock is that the market has not yet priced the upward guidance revision that Cogentrix is likely to deliver.

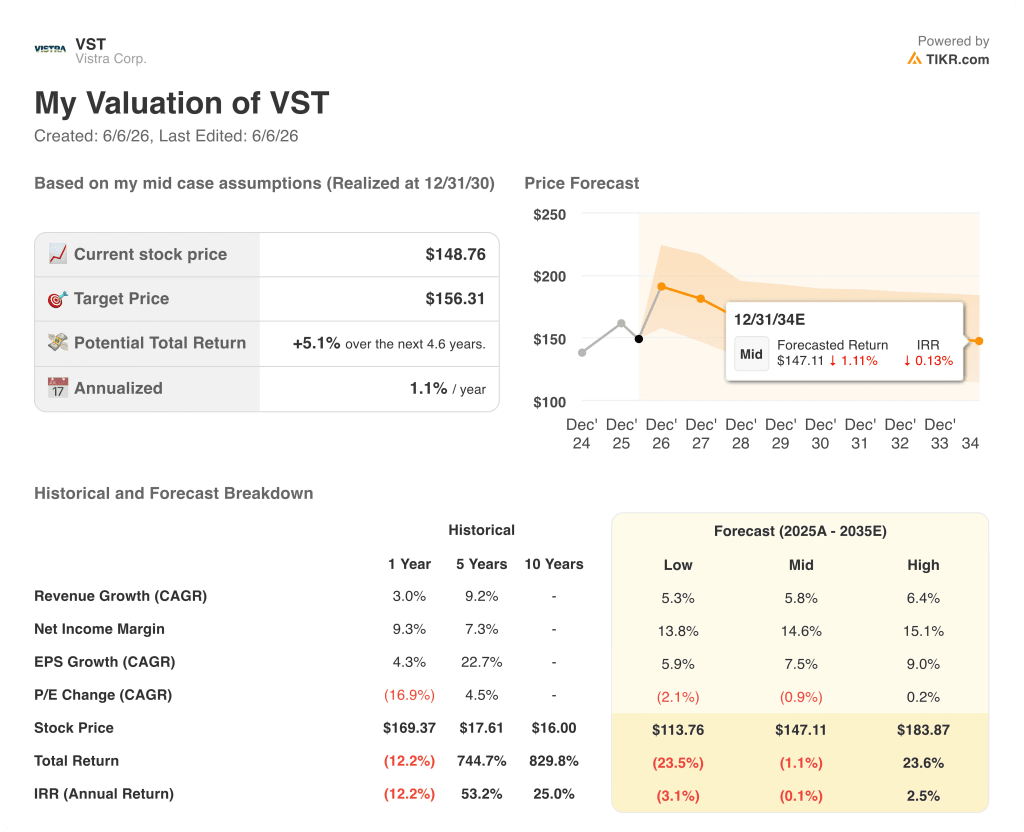

Is Vistra Stock Undervalued in 2026? What the TIKR Model Shows

TIKR’s base case values Vistra at approximately $156 by December 2030, implying roughly 5% total return from the current price of around $149, or approximately 1% annualized over the next 4.6 years.

That is the honest picture the model delivers at current assumptions: Vistra stock is roughly fairly valued on TIKR’s mid-case inputs, which embed around 5.8% revenue CAGR and a 14.6% net income margin through the forecast period.

The asymmetry lives in the scenario tails. If revenue growth comes in toward the high end at roughly 6.4% and margins expand closer to 15%, the model produces a price of approximately $184 by December 2030, representing roughly 24% total return, or around 3% annualized. That is the scenario where Cogentrix closes cleanly, Meta PPAs contribute to 2027 and beyond, and ERCOT load growth tracks management’s 5% to 6% target.

If revenue growth slows closer to 5.3% and margins compress toward 13.8%, the model prices Vistra at approximately $114 by December 2030, a roughly 24% decline from today, representing an IRR of approximately negative 3% annualized.

The scenario framework makes the investment case specific: Vistra stock is a reasonable hold at current prices on TIKR’s base case, and the Street’s far more bullish $225 mean hinges on PPA and acquisition upside that TIKR’s model has not yet incorporated. The bear case requires margin compression that the hedging program makes unlikely through 2027 but cannot rule out beyond it.

What is the price target for VST?

The Street mean price target for Vistra Corp stock is approximately $225, based on 17 analyst estimates as of early June 2026. The high target is $320 and the low is $99.

TIKR’s base case model targets approximately $156 by December 2030, reflecting a more conservative revenue growth and margin assumption than the current sell-side consensus embeds.

Is Vistra a good investment in 2026?

Vistra posted a record Q1 2026 adjusted EBITDA of approximately $1.49 billion and reaffirmed full-year guidance of $6.8 billion to $7.6 billion.

The company has achieved investment-grade ratings from both Fitch and S&P, has a heavily hedged 2026 and 2027 book, and holds approximately $1.475 billion of share repurchase authorization.

The pending Cogentrix acquisition and Meta PPAs are excluded from current guidance, representing potential upside at closing.

Should You Invest in Vistra Corp?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Vistra Corp stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vistra Corp alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VST stock on TIKR for Free →