Key Stats for Pfizer Stock

- 52-Week Range: $23 to $29

- Current Price: $26

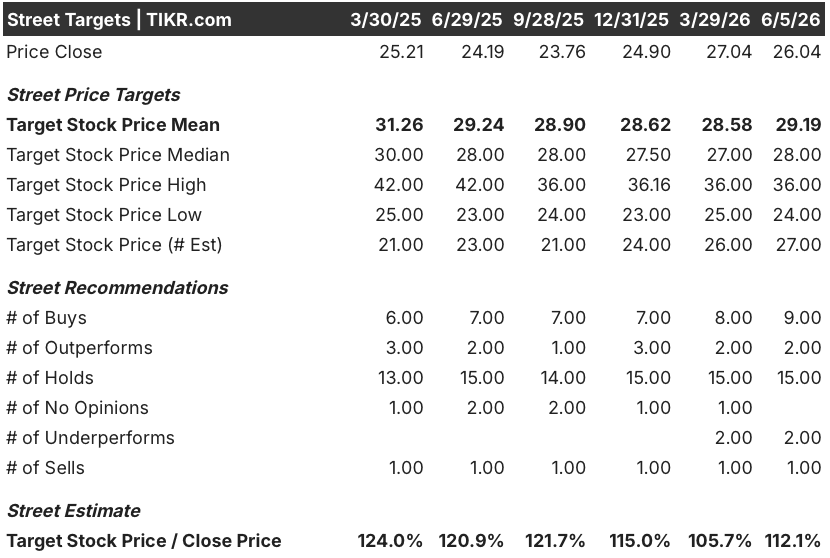

- Street Mean Target: $29

- Street High Target: $36

- Analyst Consensus: 9 Buys, 2 Outperforms, 15 Holds, 2 Underperforms, 1 Sell

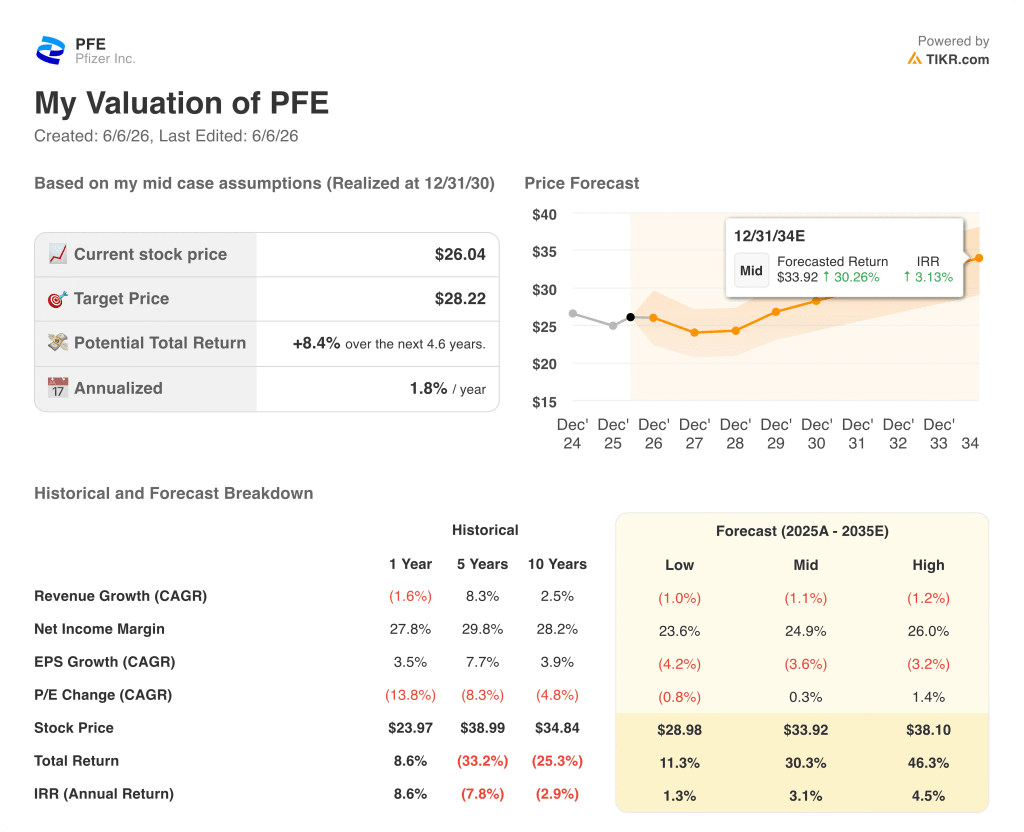

- TIKR Model Target (Dec. 2030): $28

Pfizer Stock Beats Q1 Estimates, but the Vyndamax Settlement Is the Bigger Story

Pfizer Inc. (PFE) delivered a stronger-than-expected first quarter to open 2026, reporting revenue of $14.45 billion against consensus expectations of around $13.79 billion, and CEO Albert Bourla arrived at the Jefferies Global Healthcare Conference days later with a clearer long-term growth roadmap than the company has had in years.

The headline beat was real.

Eliquis, Pfizer’s blood thinner co-marketed with Bristol Myers Squibb, generated around $2.17 billion in the quarter, well ahead of the approximately $1.76 billion analysts expected.

Adjusted EPS came in at $0.75 for the quarter, topping consensus of $0.72.

But the development that matters most for Pfizer stock over the next several years did not appear in the income statement at all.

Pfizer settled patent infringement disputes with three generic manufacturers over Vyndamax, its blockbuster heart drug, effectively blocking cheaper competition from entering the market through mid-2031 — roughly two and a half years later than the market had been modeling.

Bourla said the settlement has “the potential to change the growth profile of the company significantly post-2028,” and laid out a specific target: starting in 2029, Pfizer expects to enter a five-year period of high-single-digit revenue CAGR.

Vyndamax generated around $1.6 billion in the first quarter alone, and with that exclusivity runway now secured, the cash flow picture beyond the LOE trough is meaningfully different than it was before April.

A separate legal win followed shortly after: a Belgian court ruled that Poland and Romania must accept around 1.9 billion euros worth of Comirnaty contracts, a decision management called a positive for future EPS and cash flow.

On the oncology front, Pfizer’s Seagen acquisition continued to deliver, with Seagen products posting around 20% operational revenue growth in Q1, led by Padcev, the bladder cancer therapy that Bourla described at Jefferies as changing lives by “more than doubling” survival.

Pfizer also licensed exclusive global rights to 12 early-stage cancer programs from China’s Innovent Biologics in a deal worth up to around $10.5 billion, deepening its ADC and multispecific antibody pipeline in a move consistent with the strategy Bourla laid out at the Jeffries Global Healthcare conference: “I want to convert most of the cancers into chronic disease.”

A key binary event is approaching mid-year: Phase III data from SV, Pfizer’s integrin beta-6 targeting ADC, in second-line non-squamous lung cancer against docetaxel — the biggest oncology market in the world, with over 250,000 new U.S. cases diagnosed annually.

Why Analysts Hold Pfizer Stock at a Discount and What It Would Take to Change That

The analyst community is split, and the split is structural.

Of 29 analysts covering Pfizer stock, 9 rate it Buy, 2 Outperform, 15 Hold, 2 Underperform, and 1 Sell, with a Street mean target of around $29 and a Street high target of around $36.

That Hold-heavy distribution reflects a genuine thesis tension: the LOE headwinds from now through 2028 are visible, but the recovery runway from 2029 onward depends on pipeline binary events that have not yet resolved.

As RBC Capital analyst Trung Huynh said after the Q1 print: “The beat buys credibility and should drive near-term support… but Pfizer remains a catalyst story, not an earnings story.”

The current estimate trajectory reflects that caution directly.

Q1 2026 EBITDA came in at around $7.17 billion, but consensus projects a trough in Q2 2026 at around $5.96 billion before recovering to around $7.20 billion in Q3 2026, with EBITDA margins oscillating between around 41% and around 45% across those quarters.

Looking a year further out, Q1 2027 EBITDA is projected at around $5.33 billion, reflecting continued LOE pressure as older franchises step down — a clear illustration of why the Hold-heavy consensus exists.

The near-term revenue picture reinforces the same narrative: Q1 2026 actuals of $14.45 billion are followed by an estimated decline to around $14.41 billion in Q2 2026, with a seasonal pickup to around $16.15 billion in Q3 2026 before fading again to around $13.30 billion in Q1 2027.

The bulls — Jefferies, with a $35 target, leads the constructive case — argue the market is overpaying for the known negative (LOE) while underpricing the post-2028 pipeline optionality that the Vyndamax settlement has now partially de-risked.

The bears point to COVID franchise decay: Q1 2026 Comirnaty sales were $232 million, down around 59% year over year, below expectations of around $434 million.

What would change the consensus distribution? Positive SV Phase III data in lung cancer mid-year would be the clearest catalyst, giving Wall Street concrete evidence that the Seagen ADC pipeline extends beyond Padcev into the world’s largest oncology market.

The Vyndamax settlement has already reduced the LOE exposure management had previously characterized as roughly $17 billion through 2030 down to roughly $14 to $15 billion, a meaningful narrowing of the cliff.

At around $26, Pfizer stock trades at a meaningful discount to the Street mean of around $29 and the Street high of around $36. Given the Vyndamax settlement extension, the Seagen commercial momentum, and the concrete CAGR framework management has now committed to publicly, PFE is priced for the trough it is navigating rather than the recovery it is building toward — making this stock undervalued at current levels relative to the visibility the company now has on post-2028 growth.

Is Pfizer Stock Undervalued? TIKR’s $28 Base Case and What Each Scenario Requires

TIKR’s mid-case model prices Pfizer stock at around $28, representing a total return of around 30% from current levels through December 2030, or an annualized IRR of around 3%.

The mid case is not a recovery story; it is a stabilization story.

TIKR’s model projects revenue declining at around 1% CAGR through 2035, with net income margins held in the mid-20s range, and EPS declining at roughly 4% CAGR as the LOE years compress earnings.

The scenario breakdown reveals where the real asymmetry sits.

In the low case, TIKR prices Pfizer stock at around $29 by December 2030 — a total return of around 11%, or roughly 1% per year, essentially a dividend-plus-stability scenario with the pipeline delivering little incremental value.

In the mid case, the target moves to around $34 by December 2030, with total return of around 30% — implying that a stabilized commercial portfolio, continued Seagen growth, and partial pipeline execution are enough to re-rate the stock modestly even without a blockbuster SV outcome.

In the high case, TIKR prices Pfizer stock at around $38 by December 2030, total return around 46%, or roughly 5% annualized — a scenario that likely requires SV to deliver a positive second-line lung cancer result, continued Padcev penetration into muscle-invasive bladder cancer beyond the current high-50s market share in metastatic disease, and meaningful early obesity revenue from the Metsera platform before the first 2028 approval.

The mid-to-high spread is approximately $4 per share in target price by 2030 — not a dramatic re-rating, but meaningful given the starting valuation.

What the scenarios do not capture fully is the Vyndamax tail: a $6 billion-plus annual revenue drug that now runs through mid-2031 instead of early-to-mid 2029 compounds the cash generation window in a way that directly supports the dividend, deleveraging from the current roughly 2.8x leverage ratio, and future business development capacity (currently around $7 billion).

The annual dividend of around $0.43 per quarter — around $1.72 annualized — yields roughly 7% on the current price, a floor that constrains downside for income-oriented holders even in the low case.

The central question the scenarios frame is timing: the LOE years through 2028 are the known negative. The model’s mid case asks only that Pfizer executes on what it has already acquired, settled, and guided to. If SV adds to that, the high case becomes accessible from a conservative starting point.

Is Pfizer stock a buy in 2026?

Of 29 analysts covering PFE, 9 rate it Buy or equivalent, while 15 Hold. The Street mean target is around $29, implying roughly 12% upside from the current price of around $26.

The bull case rests on the Vyndamax settlement extending exclusivity through mid-2031, Seagen oncology momentum, and mid-year Phase III data from the SV lung cancer program.

The bear case points to LOE headwinds through 2028 and COVID franchise decay.

The stock is best characterized as a catalyst-gated value play rather than a near-term growth story.

What is the price target for Pfizer stock?

The Street mean target is around $29, with a high target of around $36.

TIKR’s mid-case model prices Pfizer stock at around $28 through December 2030, reflecting roughly 30% total return over the period. The TIKR high case reaches around $38, contingent on pipeline execution including the SV lung cancer readout.

Should You Invest in Pfizer Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Pfizer Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Pfizer Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PFE stock on TIKR for Free →