Key Stats for NXP Semiconductors Stock

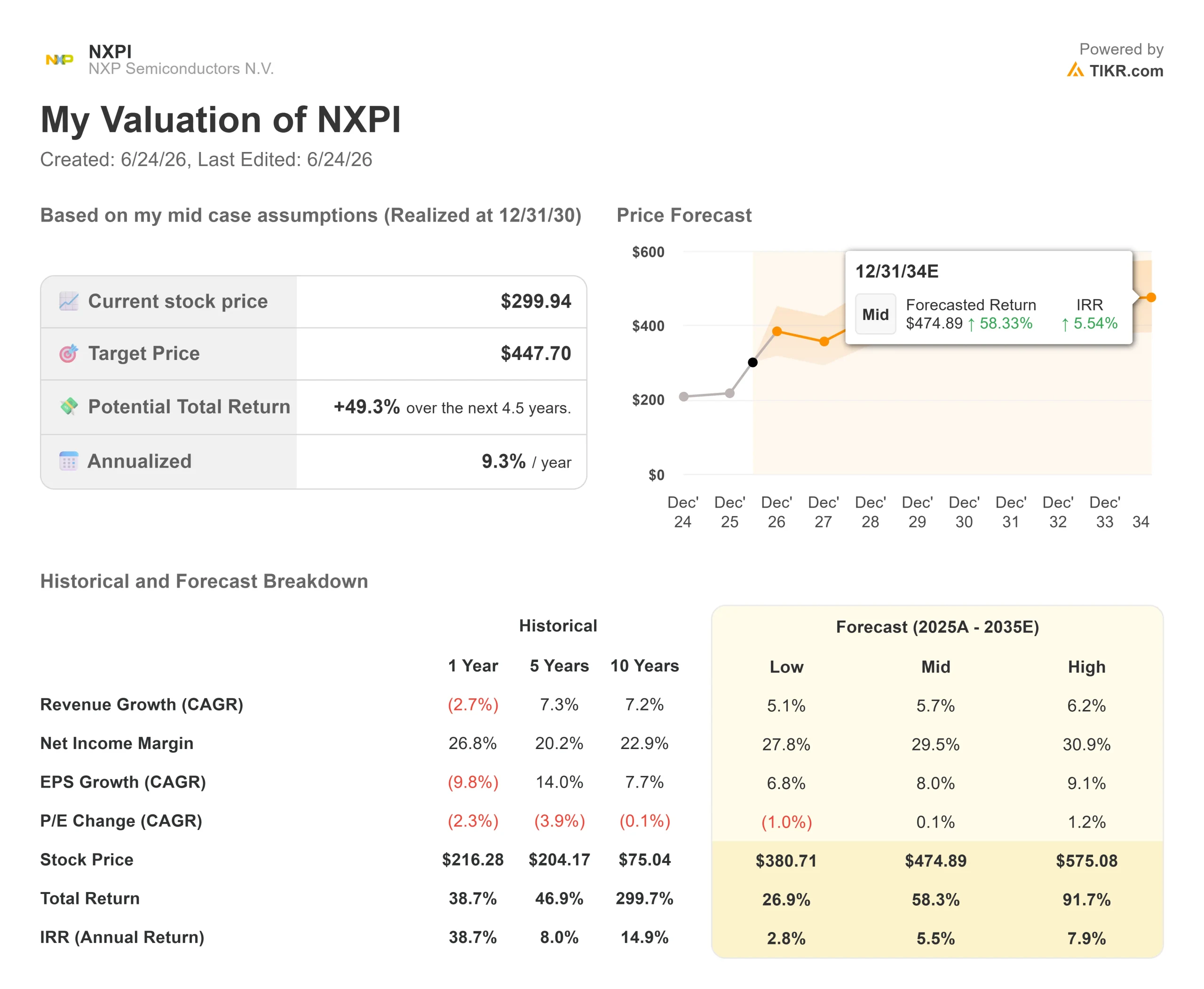

- Current Price: $299.94

- Target Price (Mid): ~$450

- Street Target: ~$307

- Potential Total Return: ~49%

- Annualized IRR: ~9% / year

- Earnings Reaction: +25.55% (April 28, 2026)

- Max Drawdown: -24.97% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

NXP Semiconductors (NXPI) lost $23.30 on June 23, 2026, closing down 7.21% at $299.94. The selling was heavy and almost entirely borrowed. NXP reported no bad news that day. It got dragged into a sector-wide chip selloff sparked by a memory-market scare, the kind of panic that treats every semiconductor ticker as interchangeable.

That is the disconnect worth sitting with. Memory fears do not touch NXP directly, because NXP does not make memory chips. It makes the analog, processing, and connectivity silicon inside cars, factories, and network racks. The market sold the company for a problem it does not have.

Earlier that same morning, Citi raised its target on NXPI to $370 from $270 and kept a Buy, citing NXP’s June analog price increases. That target sits well above the $307 Street consensus, so it is one desk’s outlier call, not the average view. Still, it framed the day’s real question: was June 23 a crack in the thesis, or a gift?

A memory scare hit a company that does not make memory

NXP’s largest exposure is automotive, roughly 58% of revenue, followed by industrial and IoT, mobile, and communications infrastructure. None of it is memory. And the fundamentals are moving the opposite way from the selloff.

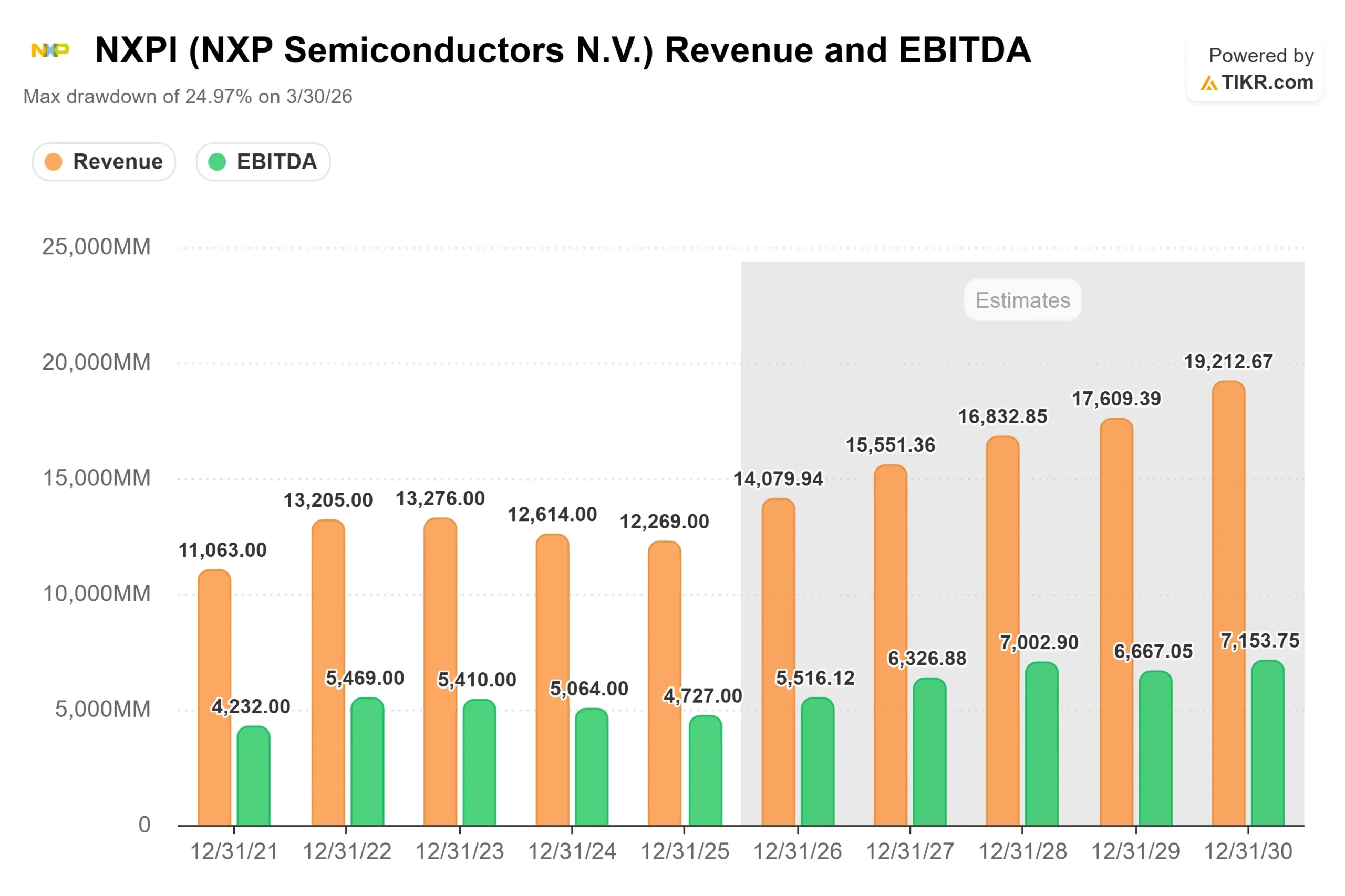

NXP posted Q1 2026 revenue of $3.18 billion, up 12% year over year and above its guidance midpoint, with broad-based improvement across its focus markets. The market cheered it at the time: NXPI jumped 25.55% on April 28, 2026, its biggest single-day gain in years. June 23 was that day’s mirror image, except only the April move was driven by NXP’s actual results.

Pricing is the cleanest tell. NXP is raising prices into the recovery, not discounting to chase volume. Jeff Palmer, EVP of Investor Relations, put it directly at TD Cowen’s conference on May 27: “We are not trying to pat our margins. All we’re looking to do is maintain our gross margins.” The hikes Citi flagged pass through real cost inflation, not soft demand. A company facing a glut does not raise prices twice in one year.

NXP’s capital moves say the same. It redeemed $750 million of senior notes in April and approved a $1.014 Q2 dividend on June 11. CFO Bill Betz called the debt move “an example of NXP’s consistent commitment to an effective capital allocation strategy, which we believe benefits all our shareholders.”

The growth story the selloff ignored

NXP’s automotive business is a content-per-vehicle story, not a car-volume story. Palmer noted the unit has compounded at 9% over three years and 13% over five, even as global car production stayed flat. The growth comes from more NXP silicon per vehicle.

Two drivers stand out. The software-defined vehicle franchise, which replaces dozens of separate controllers with fewer, more powerful processors, was over $1 billion in 2025 and is targeted to reach about $2 billion by the end of 2027, on design wins already secured. The second is a newer data center business built on control-plane chips that manage switching and power inside AI racks. That revenue is set to grow from $200 million last year to $500 million this year, inside a market Palmer sized at about $4 billion growing at a 10% CAGR.

Margins turn that revenue into earnings. Palmer’s math: every $1 billion of incremental revenue adds roughly 100 basis points of gross margin, pointing toward 60% as revenue nears $15 billion, with the VSMC fab in Singapore adding another 200 basis points once fully loaded in 2028. With gross margin at 55.6% today, the runway is real.

See historical and forward estimates for NXP Semiconductors stock (It’s free!) >>>

The valuation still treats NXP as a cyclical, not a compounder. NXPI trades at an NTM P/E of around 19x. Micron sits near 10x as a memory name, while Broadcom trades around 24x. NXP’s blend of automotive content, a scaling data center line, and a clear margin path is not obviously a 19x business, and the discount looks more like cycle-scarred memory sentiment than a verdict on the franchise.

The risk is real. NXP’s recovery leans on auto Tier 1 customers ordering to end demand. Palmer was candid that some large Tier 1s run three to four weeks of inventory, far below normal, because their margins are thin. If they stall, or a tariff shock hits production, the content story slows and the multiple compresses instead of expanding.

TIKR Advanced Model Analysis

- Current Price: $299.94

- Target Price (Mid): ~$450

- Potential Total Return: ~49%

- Annualized IRR: ~9% / year

See analysts’ growth forecasts and price targets for NXP Semiconductors stock (It’s free!) >>>

The TIKR Valuation Model uses the mid-case scenario, realized at the end of 2030, because it reflects consensus without leaning on either tail. It points to a target of around $450, a total return of around 49%, and an IRR of around 9% per year over the next four and a half years.

Two revenue drivers anchor it: the SDV processor ramp, where content per vehicle grows independent of car volumes, and the industrial, IoT, and data center portfolio, where the control-plane business adds a stream of consensus barely counted a year ago. The margin driver is operating leverage as utilization rises and VSMC reaches full load in 2028. The primary risk is automotive demand stalling if Tier 1 customers pull back.

The upside: if the ramps convert and margins climb toward 60%, the around $450 target is reachable, and the high case runs further.

The downside: if auto content stalls and the data center ramp misses its $500 million guide, returns shrink as the multiple compresses.

Conclusion

The clearest test is NXP’s Q2 2026 earnings, expected in late July. Watch two numbers. First, whether the data center business is tracking toward its $500 million full-year target, the line consensus underwrites the least, and the one that re-rates the stock if it delivers. Second, whether industrial and IoT holds low-20% year-over-year growth, which shows the recovery is broadening beyond auto. Both holdings are good; data center slipping or auto orders going quiet is bad. If the print confirms the trajectory, the gap between a 7% selloff and a $370 target closes in NXP’s favor.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in NXP Semiconductors?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NXP Semiconductors, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NXP Semiconductors alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze NXP Semiconductors on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!