Key Stats for NOV Stock

- Past-Week Performance: -8.3%

- 52-Week Range: $10.8 to $20.9

- Current Price: $18.7

What Happened?

NOV Inc., a manufacturer of drilling equipment and oilfield technology serving energy producers worldwide, generated $876 million in free cash flow over 2025 while trading at $18.72, just off a 52-week low of $10.84, as an offshore drilling recovery builds quietly beneath a soft near-term market.

Last month, NOV reported Q4 revenue of $2.28 billion, beating the $2.17 billion consensus estimate, while free cash flow of $472 million in a single quarter represented 177% conversion of adjusted EBITDA, the metric measuring operating profit before non-cash charges.

The number that makes the recovery thesis undeniable is $1.8 billion in cumulative free cash flow over 2024 and 2025 combined, generated while North America rig count fell 15% and Saudi Arabia rig count dropped over 10%, proving the portfolio’s resilience across a full downcycle.

On February 20, NOV raised its quarterly dividend 20% to $0.09 per share, a capital return signal that arrived alongside floater contract awards surging from 33 to 59 in the September 2025 through January 2026 window, confirming offshore drilling momentum is accelerating.

Jose Bayardo, Chairman, President and CEO, stated on the Q4 2025 earnings call that “the stage is set for an extended recovery as the call on production from deepwater increases,” anchoring his confidence in up to 10 FPSO project sanctions expected in 2026, up from just 5 in 2025.

With a $4.34 billion backlog, a $100 million cost-out program on track for full delivery by end of 2026, net debt-to-EBITDA at just 0.2x, and offshore rig tendering open days up over 100% for floating rigs year-over-year, NOV enters its anticipated upcycle carrying the leanest balance sheet and strongest cash generation in a decade.

Wall Street’s Take on NOV Stock

The $876 million in free cash flow NOV generated across 2025 at the cyclical trough directly sets the earnings floor from which the offshore upcycle, now confirmed by surging floater contract awards, should drive a sharp recovery.

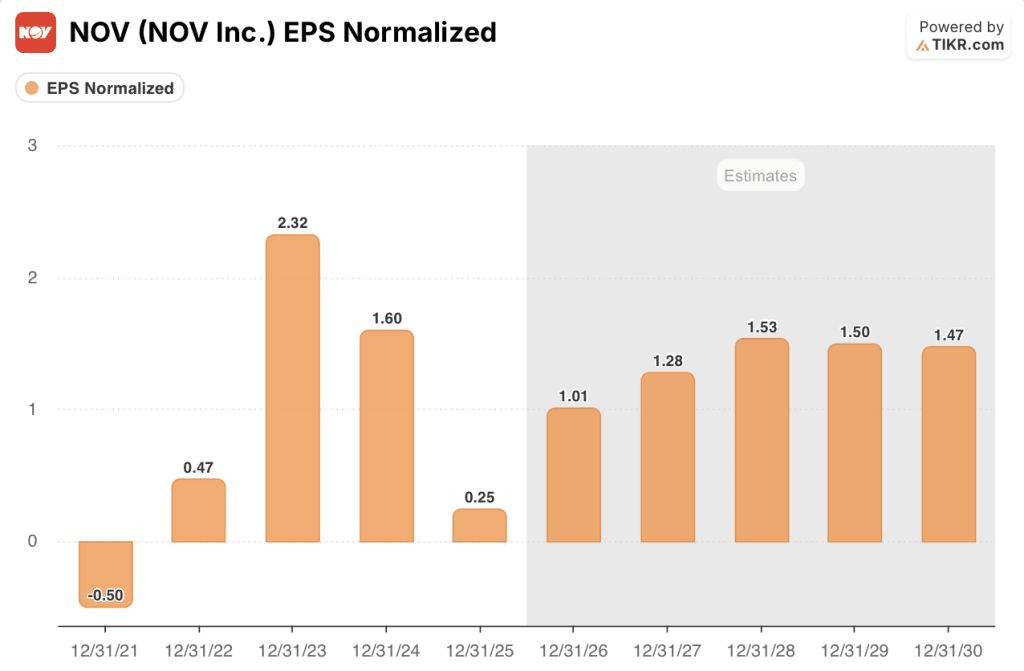

NOV’s Normalized EPS, which strips out one-time charges to show underlying earnings power, collapsed from $1.60 in 2024 to $0.25 in 2025 due to tax rate headwinds and lower activity, but TIKR forward estimates price a 307.4% recovery to $1.01 in 2026 and a further 26.5% increase to $1.28 in 2027 as offshore markets tighten.

Wall Street has quietly grown more constructive: 5 analysts rate NOV a Buy, 3 an Outperform, and 12 a Hold, with the consensus mean price target of $19.90 implying 6.3% upside from the March 12 close of $18.72.

The spread from the analyst low of $16.00 to the high of $23.00 maps directly onto the two variables already in motion: Venezuela order momentum and FPSO FID count, which management confirmed could reach 10 sanctions in 2026 alone.

What Does the Valuation Model Say?

The TIKR mid-case model prices NOV at $21.00 by December 2030, implying 12.2% total return and a 2.4% annualized IRR. The model assumes only 2.4% revenue CAGR but net income margins expanding from 1.1% in 2025 to 5.5% by 2030, driven by the $100 million cost-out program and offshore mix improvement.

The market prices NOV on trough earnings of $0.25 per share, ignoring that the company generated $876 million in free cash flow at that same trough — a cash generation rate no cyclical multiple captures.

The $4.34 billion backlog, 91% book-to-bill in 2025, and a full-year 2026 book-to-bill expected near 100% confirm the TIKR model’s modest revenue recovery assumption is already visible in booked orders.

Management raised the quarterly dividend 20% to $0.09 on February 20 with net debt-to-EBITDA at just 0.2x, signaling confidence in the cash floor precisely when the market prices maximum cycle uncertainty.

If FPSO FID count disappoints below 5 in 2026, the offshore equipment backlog growth stalls, the EPS recovery to $1.01 fails to materialize, and the TIKR mid-case target loses its primary demand driver.

NOV’s late April 2026 Q1 earnings call is the first confirmation point: watch whether Energy Equipment revenue delivers the guided 3% to 5% year-over-year growth and whether book-to-bill holds near 1x.

Should You Invest in NOV Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NOV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NOV Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NOV stock on TIKR for Free →