Key Stats for NVTS Stock

- 52-Week Range: ~$2 to ~$22

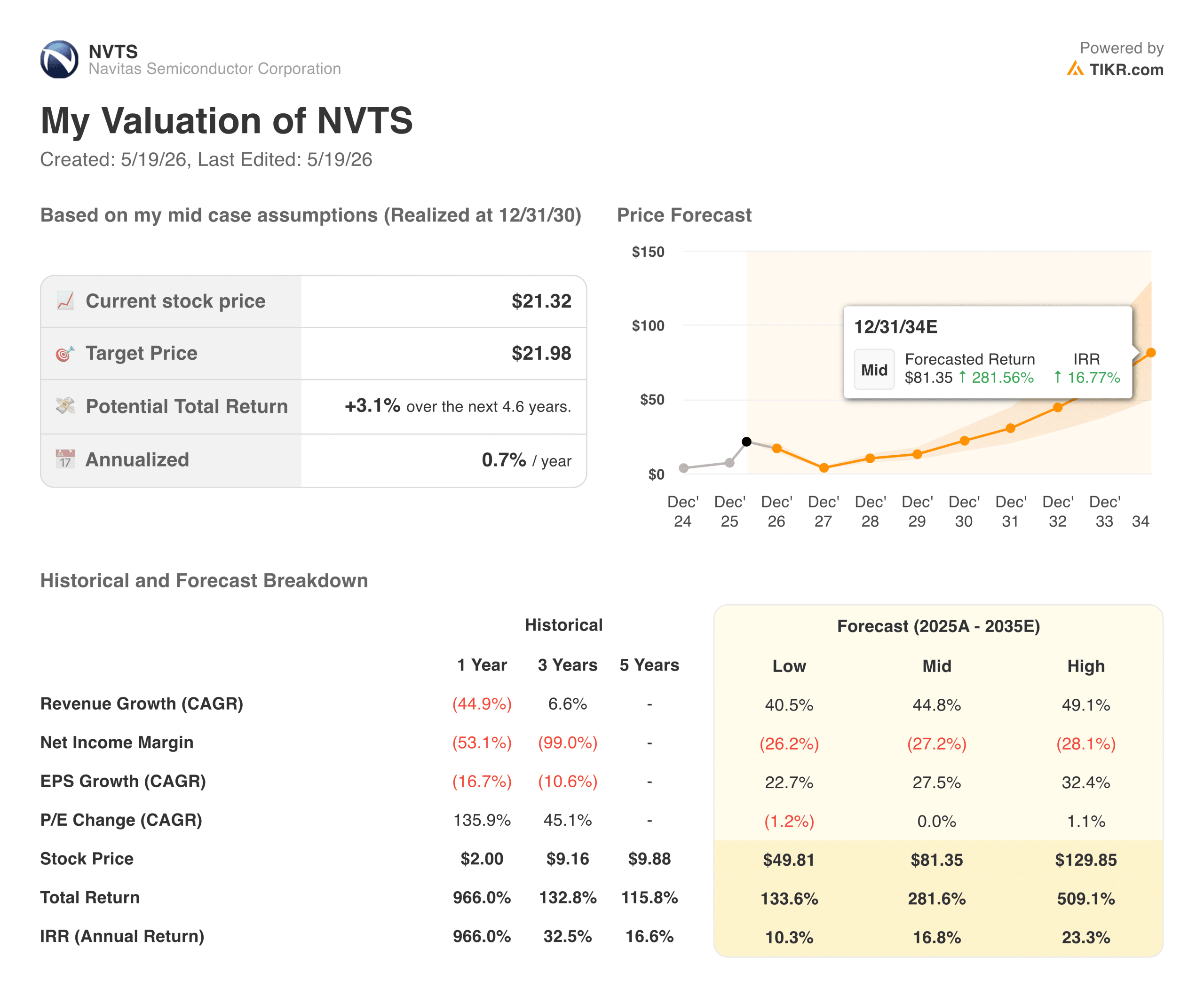

- Current Price: $21.32

- TIKR Target Price (Mid, 4.6 Years): ~$22

- TIKR Annualized IRR (Mid, 4.6 Years): ~1% per year

- TIKR IRR (Mid, 8+ Years): ~17% per year

- Most Recent Quarterly Revenue: $8.6M (down 39% YoY, up 18% sequentially)

- Non-GAAP Gross Margin: 39.0%

- Most Recent Quarterly Net Loss: $33.8M

- FY2026 Revenue Guidance: ~$41M

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

The 1,000% Rally and the 39% Revenue Decline

The easiest way to understand Navitas Semiconductor (NVTS) is to accept that both of these things are true at the same time: revenue fell nearly 40% year over year in the most recent quarter, and the stock has risen roughly 1,000% over the past twelve months. At Navitas, both are accurate, and understanding why tells you everything about what kind of investment this actually is.

Navitas makes gallium nitride and silicon carbide power semiconductors, the chips that control how electricity flows through data centers, EV chargers, solar inverters, and industrial equipment. GaN and SiC run more efficiently than traditional silicon at higher voltages and temperatures, which matters when you are trying to cool a building full of AI servers or charge an electric vehicle quickly.

The revenue decline came from deliberately exiting low-margin mobile and consumer business in China, which happened faster than the high-power replacement revenue could arrive. That is the setup the charts reflect.

See analysts’ growth forecasts and price targets for NVTS stock (It’s free!) >>>

What the Gross Margin Chart Is Telling You

Gross margins started at 45% in 2021, dropped to 31% in 2022 as mobile volumes were sold at lower prices to fill fab capacity, recovered to 39% in 2023, then drifted back toward 31% by 2025 as mobile wound down before high-power could scale up.

On a non-GAAP basis, which strips out acquisition-related amortization running through cost of goods sold, the most recent quarter came in at 39%. The trajectory management is working toward is margins improving steadily as AI data center revenue grows and mobile fades to zero.

The historical chart shows a business that has not yet demonstrated that trend consistently, which is an honest read of where things stand.

Estimate a company’s fair value instantly (Free with TIKR) >>>

What the Cash Burn Looks Like

Navitas has burned between $44 million and $66 million in free cash flow every year since going public, with no year of positive FCF. The estimates show gradual improvement from roughly -$61M in 2026 toward -$22M by 2028, with breakeven dependent on quarterly revenue scaling into the high-$30 million range. Management has been explicit about that threshold.

Getting there requires sequential growth to continue uninterrupted, gross margins to hold or improve, and operating expenses to stay roughly flat. Each assumption is individually plausible. Sustaining all three simultaneously over several years is where the execution risk lives.

What the TIKR Model Is Actually Saying

The near-term TIKR model is unusually direct. The mid-case target over 4.6 years is essentially $22, barely above the current price, implying annualized returns of less than 1%.

The 8-year mid case is a different picture entirely, targeting around $81 at roughly 17% annually if Navitas grows at roughly 45% annually, reaches profitability, and gets re-rated as the business matures.

The gap between those two time frames tells you exactly what kind of investment this is. You are not buying near-term earnings growth, but a long-duration bet on a technology platform.

What Could Drive the Returns Higher or Lower

The bull case rests on real technology, as GaN and SiC genuinely outperform silicon in high-power applications, AI data centers genuinely need more efficient power delivery, and high-power revenue grew 35% year over year in the most recent quarter with AI infrastructure specifically up 50% sequentially. If that momentum builds as mobile fades, the mix problem resolves itself.

The bear case is that Navitas is a small company with $8.6 million in quarterly revenue burning $40 to $65 million annually, competing against Texas Instruments, Infineon, and ON Semiconductor in markets that are attracting more capital as the technology matures.

The current price-to-sales multiple leaves almost no room for execution risk.

Is NVTS Worth Buying at $124?

If you believe in the decade-long GaN and SiC adoption story and are willing to hold through years of negative FCF and quarterly volatility, the 8-year case at around $81 at roughly 17% annually is worth serious consideration.

If you are evaluating the next four to five years, the model is nearly explicit: the near-term upside from the current price is minimal.

The stock has already priced in most of the near-term good news, and the journey from $41 million in annual revenue to something that justifies the current multiple is going to take longer than the past twelve months of stock performance might suggest.

Analyze Navitas Semiconductor stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!