Key Stats for Danaher Stock

- 52-Week Range: $161 to $243

- Current Price: $164

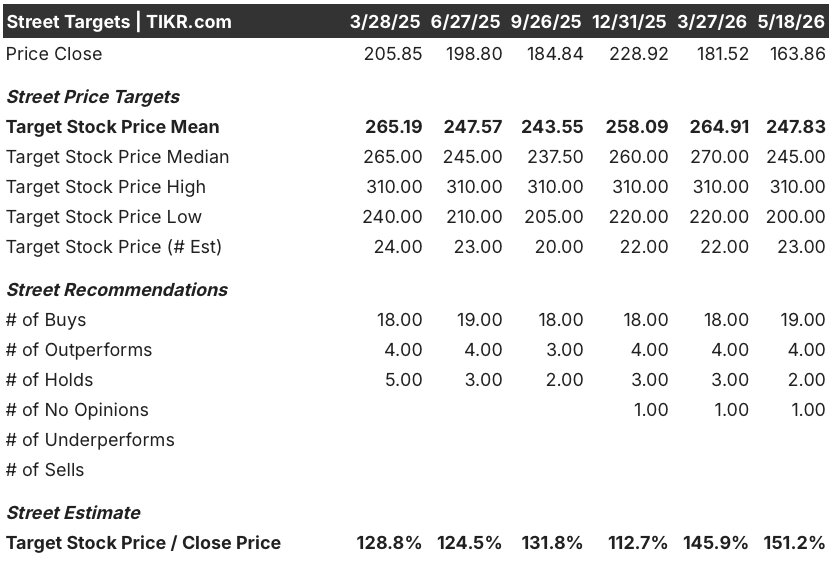

- Street Mean Target: $248

- Street High Target: $310

- Analyst Consensus: 19 Buys / 4 Outperforms / 2 Holds / 1 No Opinion

- TIKR Model Target (Dec. 2030): $

Danaher Beats Q1 EPS by 6% as Bioprocessing Equipment Orders Signal a Multiyear Upcycle

Danaher Corporation (DHR), a Washington, D.C.-based life sciences and diagnostics platform serving pharmaceutical, biotech, and clinical customers globally, delivered a Q1 2026 earnings beat that confirmed the recovery thesis while the stock sat near a 52-week low following Q1 results in April.

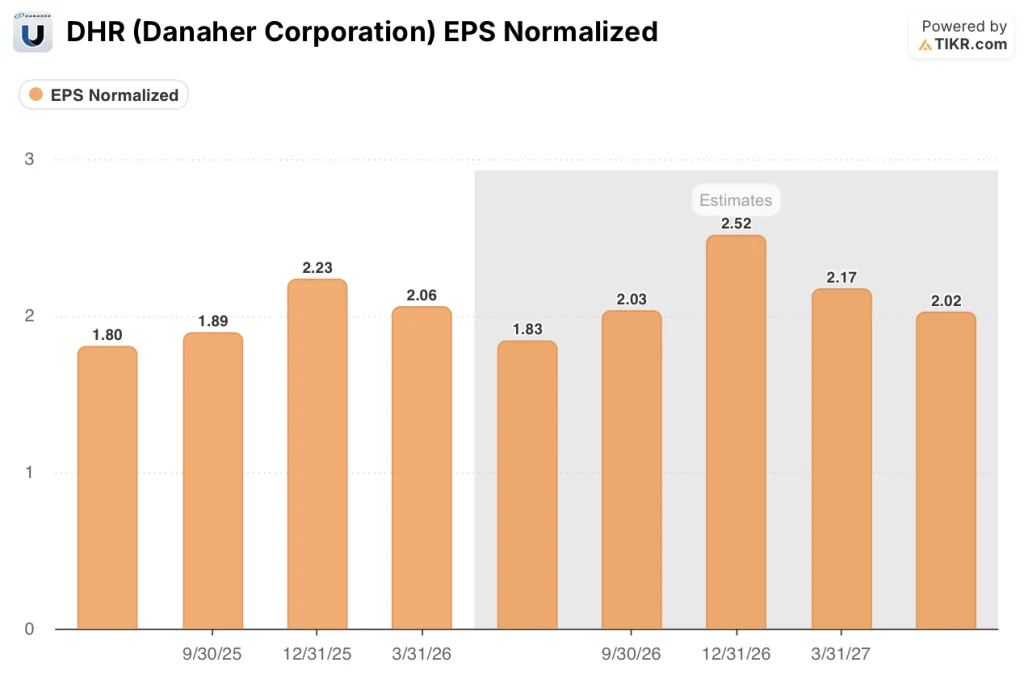

Adjusted EPS came in at $2.06 for the quarter ended March 27, beating the consensus estimate of $1.94 by around 6% and representing 9.5% year-over-year growth despite a 25% decline in respiratory revenue at Cepheid that created a roughly 250-basis-point headwind to core growth.

The bioprocessing unit, anchored by Cytiva, delivered the sharpest signal of the quarter: equipment orders grew more than 30% year-over-year, the first positive year-over-year orders growth in nearly two years, even as equipment revenue remained modestly down.

CEO Rainer Blair stated on the Q1 2026 earnings call that “we are really encouraged to see improvement in our equipment order book with over 30% year-over-year growth,” and added that the company sees itself “in the early stages of a multiyear investment cycle” driven by brownfield capacity additions and reshoring activity.

Danaher stock carries direct exposure to the next leg of that cycle: with CDMOs acquiring underutilized pharmaceutical plants and greenfield projects still in the quoting phase, equipment order conversion over 6 to 18 months creates a revenue ramp that the current share price does not reflect.

Beyond bioprocessing, two other developments add dimension to the Danaher stock thesis in 2026: the pending $9.9 billion acquisition of Masimo, a pulse oximetry and patient monitoring company in acute care settings, and a $172.5 million securities class action settlement agreed in April covering shareholder claims related to 2022-2023 bioprocessing demand guidance.

The Masimo deal, funded partly by a EUR 3 billion four-tranche senior notes offering priced in late April, is expected to close in the second half of 2026, pending regulatory approvals, and is projected to be accretive to adjusted diluted EPS in the first full year of ownership.

DHR Draws 23 Buy-Side Ratings as Equipment Orders Reframe the Recovery Narrative

The central analytical question on Danaher stock entering 2026 was whether the bioprocessing recovery was a consumables-only story or the beginning of a broader equipment cycle, and Q1 answered it clearly enough that the consensus held firm even as the stock slid.

Wall Street projects Danaher’s normalized EPS at around $1.83 for Q2 2026, growing to around $2.03 in Q3, around $2.52 in Q4, and around $2.17 in Q1 2027, implying high single-digit to low double-digit growth as the China VBP diagnostic headwinds and respiratory softness roll off in the second half.

The full-year 2026 adjusted EPS guidance range of $8.35 to $8.55, raised from $8.35 to $8.50 on Q1 strength, aligns with the consensus normalized EPS estimate of $8.44, with the Street projecting further acceleration to around $9.09 in 2027 and around $9.97 in 2028 as the equipment cycle converts.

With 19 analysts rating DHR a Buy, 4 rating it Outperform, and only 2 rating it Hold, the Street’s conviction is unusually high: 23 of 26 analysts with active ratings are constructive, with a mean price target of $247.83 and an implied upside of around 51% from the May 18 close of $163.86.

The reason that conviction persists at a stock price near a 52-week low is the bioprocessing hypothesis: high single-digit consumables growth has been the steady signal for several quarters, the 30%-plus equipment order inflection now provides a second confirming data point, and the company has managed to expand operating margins and grow EPS by nearly 10% even with a material respiratory headwind.

TD Cowen reiterated its Buy rating post-Q1 (cutting its price target modestly to $240 from $245) and flagged that excluding flu and respiratory testing, underlying demand trends were more stable, with early signs of recovery in bioprocessing equipment, biopharma research activity, and China demand all intact.

DHR’s Operating Margins Recover to 22.9% as Bioprocessing Mix Offsets Respiratory Drag

Danaher posted Q1 2026 operating income of $1.37 billion on revenue of $5.95 billion, with an operating margin of 23%, up from 20.1% in the year-ago period, as cost discipline and favorable segment mix more than offset the negative impact of lower-margin respiratory revenue.

The 22.9% Q1 2026 operating margin represents the strongest operating margin Danaher has delivered in the past eight quarters of data, reaching this level even while absorbing a roughly 250-basis-point respiratory revenue headwind that management identified as the primary source of top-line softness.

Gross margins also recovered to 60.3% in Q1 2026 from a trough of 58.2% in Q3 and Q4 2025, reflecting a mix shift back toward higher-margin bioprocessing consumables and diagnostics reagent business as the biotech funding environment stabilized.

Operating income grew 5.7% year-over-year in Q1 2026 while revenue grew 3.7%, confirming the operating leverage dynamic: Danaher is extracting more profit per dollar of revenue as the cost-reduction actions taken during the 2023 to 2025 normalization period flow through the income statement.

TIKR’s Model Values Danaher at $249 by December 2030: The Assumptions Behind the 52% Return

TIKR’s valuation model prices Danaher Corporation at $249 per share by December 2030, implying a 52% total return from the current price of $163.86, or around 10% annualized over the next 4.6 years.

The mid-case assumes a revenue CAGR of around 4% and net income margins expanding to around 27%, figures that reflect a bioprocessing consumables and equipment cycle normalizing into a high single-digit growth platform rather than the post-pandemic correction trough the stock currently prices in.

The target requires Danaher’s P/E multiple to hold near current levels through the period, which is not guaranteed given the debt added for the Masimo acquisition and the 2.5x net debt to EBITDA the balance sheet will carry at close.

The low case produces a stock price of around $248 by December 2034 at an IRR of around 4.9%, consistent with a scenario where the bioprocessing equipment cycle delivers minimal incremental revenue and Masimo integration takes longer than projected to expand margins.

The mid case reaches around $308 by December 2034 at an IRR of around 7.6%, the scenario where consumables growth holds at high single digits, equipment revenue inflects in 2027 as brownfield orders convert, and Masimo contributes the $125 million in cost synergies management identified by year five.

The high case reaches around $371 by December 2034 at an IRR of around 9.9%, produced by an acceleration in both the bioprocessing equipment cycle and Life Sciences instruments demand as academic and government funding constraints ease and the AI-driven drug discovery flywheel Blair described begins pulling forward commercial biologic production.

How did Danaher perform in Q1 2026 earnings?

Danaher delivered Q1 2026 adjusted EPS of $2.06, beating the consensus estimate of $1.94 by around 6% and growing 9.5% year-over-year.

Revenue was $5.95 billion against a $6 billion estimate, while bioprocessing equipment orders grew more than 30% year-over-year, the first positive result in nearly two years.

The company raised its full-year 2026 adjusted EPS guidance to $8.35 to $8.55 from the prior range of $8.35 to $8.50.

What is the price target for DHR stock?

The Wall Street mean price target for DHR stock is $248 as of May 18, 2026, implying around 51% upside from the current price of $164.

The high-end Street target is $310, and 23 of 26 active analysts hold Buy or Outperform ratings.

TIKR’s base case target of around $249 aligns closely with the Street mean, anchored to a mid-case revenue CAGR of around 4% and expanding net income margins toward 27%.

Should You Invest in Danaher Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Danaher Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Danaher Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DHR stock on TIKR for Free →