Key Stats for Chevron Stock

- 52-Week Range: $134 to $215

- Current Price: $196

- Street Mean Target: $215

- Street High Target: $236

- Analyst Consensus: 13 Buys / 5 Outperforms / 6 Holds / 1 Underperform / 1 Sell

- TIKR Model Target (Dec. 2030): $

Chevron Stock Delivers a Q1 Beat While Running the Playbook No Rival Can Copy

Chevron Corporation (CVX) is one of the world’s largest integrated energy companies, and its Q1 2026 earnings report delivered the clearest proof yet that its portfolio architecture was built for exactly the moment the world now finds itself in.

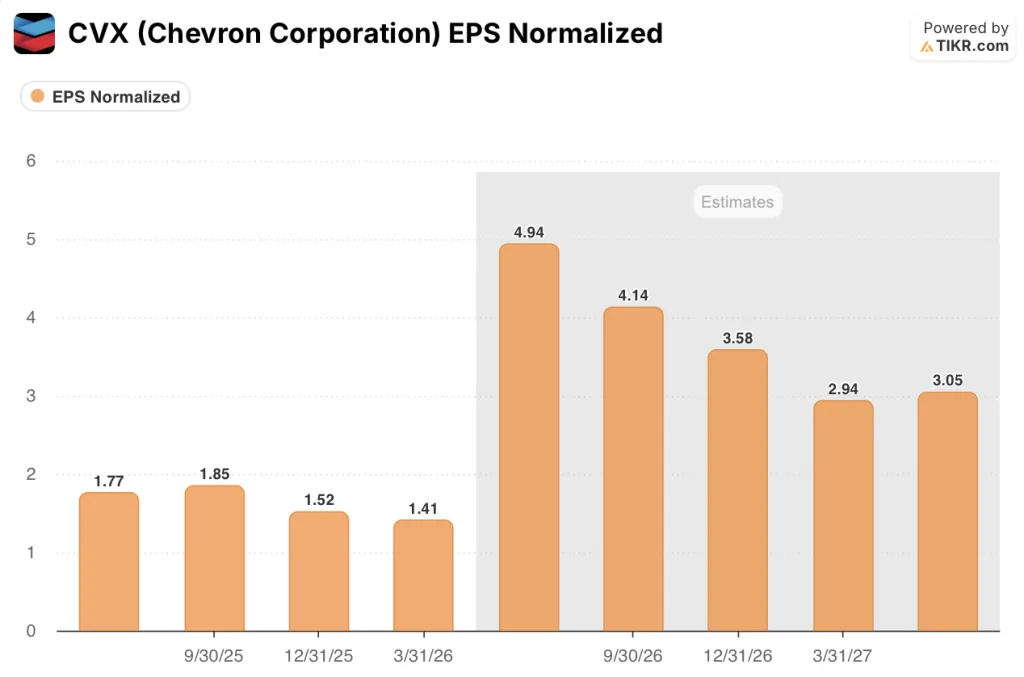

The company reported adjusted EPS of $1.41 for Q1 2026, beating the Street’s consensus estimate of $0.95 by a wide margin, even as net income of $2.2 billion fell 36.9% year-over-year under the weight of roughly $3 billion in derivative timing effects tied to the steep run-up in commodity prices during March.

That timing hit is not a fundamental story — it is an accounting artifact of surging oil prices, and CFO Eimear Bonner confirmed around $1 billion of those paper positions are expected to unwind into profit in Q2.

The real story in Chevron stock is what the upstream business is doing: segment earnings of $3.9 billion were up 4% year-over-year, production hit 3,858 MBOED for the quarter, and U.S. output exceeded 2 million barrels per day for the third consecutive quarter — now bolstered by the completed integration of the Hess acquisition.

Less than 5% of Chevron’s production sits in the Middle East, a structural advantage over rivals with heavier regional exposure, and CEO Mike Wirth leaned into that fact during Q1 2026 earnings call: “Despite heightened geopolitical volatility and related supply disruptions, Chevron delivered solid first-quarter performance, underscoring the resilience of our portfolio and the value of disciplined execution.”

The Tengizchevroil (TCO) plant in Kazakhstan, Chevron’s single largest cash-generating asset, returned to full production after a fire-related disruption in Q1 and is now running above 1 million BOEPD, with full-year free cash flow guidance of $6 billion unchanged despite the Q1 setback.

Chevron also moved in Venezuela, completing an asset swap with PDVSA that expanded its stake in the Petroindependencia joint venture to 49% and adds contiguous acreage to its Petropiar position in the Orinoco Belt, with CEO Wirth projecting the company’s outstanding Venezuelan debt to be fully recovered by 2027 at current price levels.

Analysts Hold a $215 Mean Target on CVX Stock Despite Downstream Noise

The investment debate around Chevron stock right now is not whether the business is performing well — it is whether the derivative timing effects obscuring Q1 GAAP earnings will continue to distort the market’s read on underlying cash generation.

The answer is no. The $3 billion timing hit in Q1 is a function of rising prices and mark-to-market accounting on paper derivative positions linked to physical cargoes; those effects mechanically reverse as cargoes settle, and Bonner was direct in confirming the Q2 unwind timeline.

Strip out the timing noise, and what remains is a business generating adjusted free cash flow of $4.1 billion in a single quarter, with U.S. refineries running at record crude throughput and international LNG facilities at Gorgon and Wheatstone running at full rates.

The Street has absorbed that read clearly: 13 analysts rate CVX a Buy, 5 rate it Outperform, 6 Hold, 1 Underperform, and 1 Sell, with a mean price target of around $215, implying roughly 10% upside from the current price of $196.12.

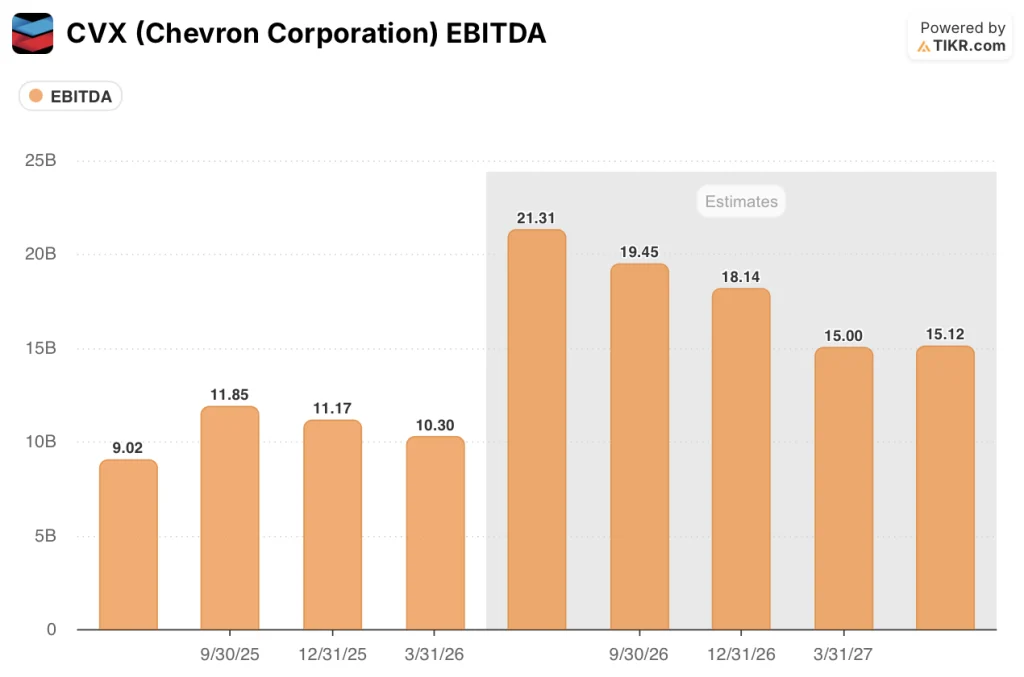

Consensus EBITDA for Q2 2026 is forecast at around $21 billion, a roughly 136% jump year-over-year, reflecting the combination of elevated oil prices from the Strait of Hormuz disruption and the full integration of Hess assets into the production base.

Meanwhile, the per-share picture tells the same story with even more precision: consensus EPS for Q2 2026 sits at around $5, up from $1.41 in Q1 and $1.85 in the year-ago period, as the derivative drag that suppressed Q1 reported earnings reverses and elevated commodity realizations flow through upstream margins without the accounting offset.

The structural case for Chevron stock rests on three pillars that are each delivering right now: the Hess integration added approximately 500,000 BOEPD of production year-over-year in Q1, the Eastern Mediterranean gas assets at Leviathan and Tamar are running at full capacity with expansion projects on track, and the TCO debottlenecking work completed in late 2025 is showing early production upside that management says it will quantify on the Q2 call.

The one genuine tension the Street is watching is the downstream segment, which swung to a loss of $817 million in Q1 from a $325 million profit a year ago, entirely on timing effects rather than deteriorating refining economics — in fact, Wirth highlighted that Chevron’s refining integration is now directing over 40% equity crude into its Asian refineries and above 50% into its U.S. system, a competitive advantage in a market where crude access is the primary constraint on throughput.

TIKR’s $210 Base Case and the Path to $280 by 2030

TIKR’s mid-case valuation model targets CVX stock at around $210 by year-end 2026, anchored to a net income margin expansion toward around 11% and EPS CAGR of roughly 9% through 2030, assumptions grounded in the Hess production ramp, the TCO debottlenecking upside, and sustained elevated commodity prices through at least mid-decade.

At roughly $196 against TIKR’s mid-case 2030 price forecast of around $281, with a total return of around 43% over the forecast period against a 10-year historical IRR of 7%, Chevron stock appears undervalued for investors with a multi-year horizon willing to own a capital-disciplined supermajor through a period of structurally elevated energy prices.

The scenario for CVX comes down to one question: how long does the current supply environment persist, and how much of that cash flow does Chevron return versus reinvest?

Is Chevron stock undervalued?

TIKR’s mid-case model targets CVX at around $210 by end-2026 and around $281 by 2030, implying roughly 10% near-term and around 43% total return over the forecast period.

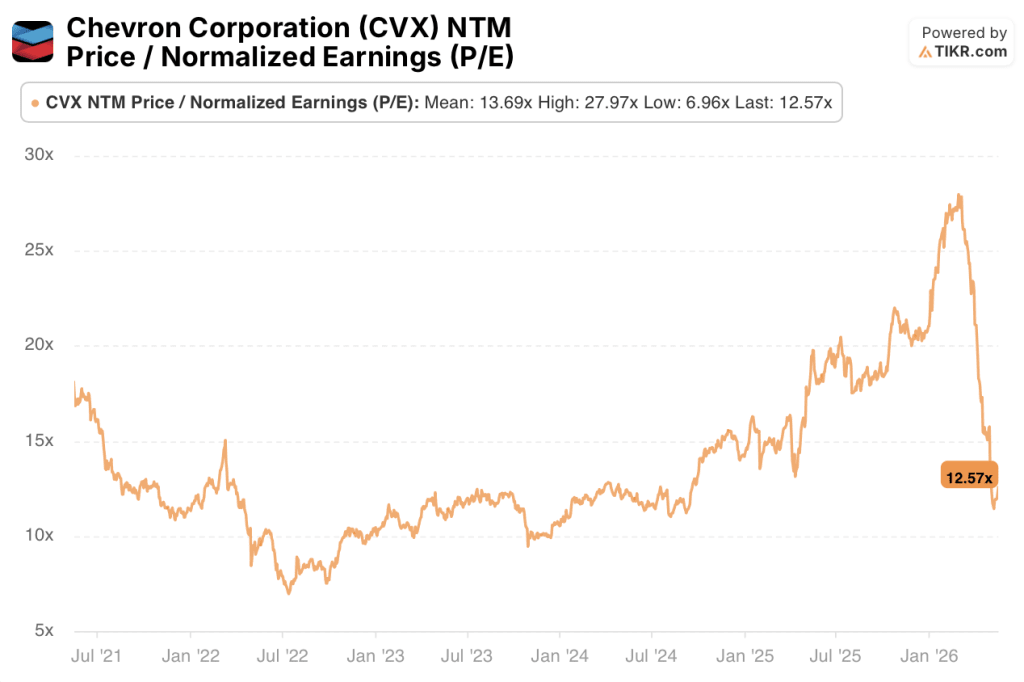

CVX currently trades at 12.57x NTM P/E, below its historical mean of 13.69x, while EPS is expected to nearly triple year-over-year in Q2 as Q1 derivative timing effects unwind.

The key variable is commodity price durability past the Hormuz disruption.

Should You Invest in Chevron Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Chevron Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Chevron Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CVX stock on TIKR for Free →