Key Fundamental Metrics for MCD Stock

- 52-Week Range: $271.98 to $341.75

- Current Stock Price: $277.97

- Street Consensus Target Price: ~$330

- LTM Gross Margin: 57.3%

- LTM EBIT Margin: 46.0%

- LTM Net Debt / EBITDA: 3.25x

- Dividend Yield: 2.7%

- Mid-Case 10-Year Forward Stock Price Target: ~$400

See analysts’ growth forecasts and price targets for McDonald’s Corporation (It’s free) >>>

Value Meals and a Warning Shot: What the Market Is Actually Pricing In

McDonald’s (MCD) reported Q1 2026 revenue of $6.52 billion, up 9% year over year and the strongest quarterly revenue growth in eight quarters. Adjusted EPS came in at $2.83, beating the consensus estimate of $2.77. Global comparable sales grew 3.8%, with positive results across all three operating segments.

The stock barely moved. What overshadowed the beat was CEO Chris Kempczinski’s candid assessment on the earnings call that the consumer environment “may be getting a little bit worse,” with management flagging an expected slowdown in Q2 comparable sales, driven by rising fuel and grocery prices that are squeezing lower-income households.

At $278, MCD is trading just above its 52-week low and roughly 19% below the Street’s consensus target of around $330. The gap between the business quality and the current price is worth examining carefully.

Value McDonald’s Corporation instantly (Free with TIKR) >>>

The Franchise Model’s Hidden Superpower: Turning $27 Billion in Revenue Into $7 Billion in Cash

The chart above illustrates one of the most underappreciated facts about McDonald’s financial model. Revenue has grown steadily from $23.2 billion in 2021 to $26.9 billion in 2025, but the more striking data point is the consistency of free cash flow. Through supply chain disruptions, an E. coli outbreak, and a challenging consumer environment, McDonald’s has generated between $6.7 billion and $7.3 billion in free cash flow every single year.

That stability is structural, not coincidental. Approximately 95% of McDonald’s 45,699 locations worldwide are owned and operated by independent franchisees, meaning the company collects rent and royalties rather than running restaurants directly.

The capital stays with franchisees, but the cash flows to McDonald’s. That model produces a 46% EBIT margin, a number most consumer businesses cannot get close to, regardless of how well they execute.

The Q1 result reinforced this picture. McDonald’s generated $2.41 billion in operating cash flow against just $682 million in capital spending, supporting a $1.86-per-share quarterly dividend and continued buybacks even as it absorbed $47 million in restructuring costs tied to its Accelerating the Organization initiative.

Analyze your favorite stocks like McDonald’s Corporation with TIKR (It’s free) >>>

Value as a Weapon: How McDonald’s Is Using the McValue Platform to Take Share

The consumer pressure flagged by management is real, but it is also where McDonald’s competitive positioning becomes most relevant. When budgets tighten, McDonald’s benefits from trade-down, as consumers who might otherwise go to Chipotle or a casual dining chain look for a cheaper meal. The relaunch of Extra Value Meals and the McValue platform in Q1 was deliberately timed to capture exactly that dynamic.

U.S. comparable sales grew 3.9% in Q1, supported by positive guest count growth and sustained market share gains versus direct competitors. The International Operated Markets segment, covering the U.K., Germany, Australia, and France, also grew comps by 3.9%, with mid-to-high single-digit growth in the U.K. and Germany specifically.

The Q2 warning is a near-term headwind, not a structural one. McDonald’s has navigated consumer downturns before and emerged with a higher market share on the other side.

A Decade of Earnings Durability With Room Left to Run

The EPS chart tells a story of steady, undramatic compounding that suits McDonald’s perfectly. Normalized EPS grew from $9.28 in 2021 to $12.20 in 2025, a period that included significant commodity inflation, labor cost increases, and the aftermath of the E. coli incident that weighed on U.S. traffic in late 2024. The consensus now projects around $13 for 2026, reaching $14 by 2027 and climbing toward $18 by 2030.

That trajectory is built on a business model in which revenue growth need not be dramatic for earnings to compound meaningfully. Because McDonald’s collects royalties and rent with relatively fixed overhead, incremental revenue flows through to the bottom line at an unusually high rate. A forward EPS CAGR of around 8% over two years, against a business with a 0.44 beta and a 2.7% dividend yield, is a compelling risk-adjusted profile.

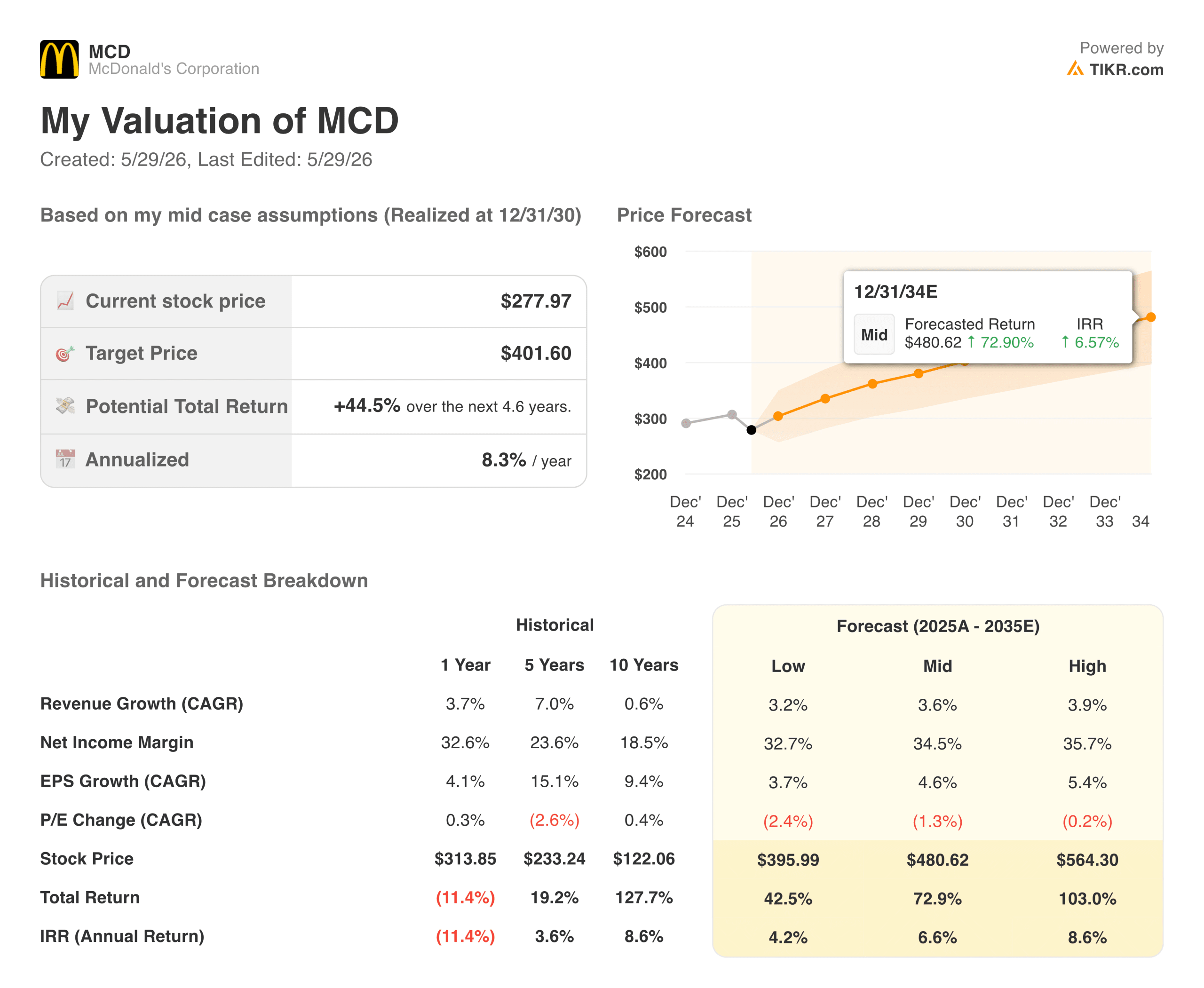

What the TIKR Valuation Model Says About MCD at $278

TIKR’s mid-case valuation model targets around $401 for MCD, implying a total return of around 44% from the current price, or roughly 8% annualized over the next 4.6 years. The model assumes around 4% annual revenue growth and net income margins holding near 35%, with EPS growing at around 5% per year on a compounded basis.

The low case is around $395, and the high case is around $565. The narrow spread between the low and mid cases reflects how predictable McDonald’s earnings profile actually is, even in a challenging environment.

The model’s revenue growth assumption of around 4% is modest and deliberately so. It does not require a consumer recovery or a reacceleration in guest counts. It simply asks whether McDonald’s can continue doing what it has done for decades, growing system-wide sales steadily while franchisee economics remain healthy enough to support reinvestment. On that basis, the numbers suggest the current price reflects a level of risk that the business itself has not historically justified.

Is MCD Worth Buying at Today’s Levels?

At $278, McDonald’s is trading near the bottom of its 52-week range and well below a Street consensus target of around $330. The 2.7% dividend yield is the highest in several years, and the company has raised its dividend for 49 consecutive years.

The near-term risk is a Q2 comp miss that confirms the consumer slowdown management flagged. That could keep the stock range-bound through the summer, particularly if broader market sentiment around consumer discretionary names stays cautious.

For investors with a long-term horizon, however, the combination of a discounted entry price, a durable free cash flow engine, a rising dividend, and a valuation model pointing to around 8% annualized returns makes the current price one of the more straightforward setups in the large-cap consumer space.

Q1 was a beat. But are U.S. margins fixable? Run McDonald’s stock through TIKR’s valuation model for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!