Key Stats for Hims & Hers Stock

- Current Price: $24.01

- Target Price (Mid): ~$35

- Street Target: ~$26

- Potential Total Return: ~45%

- Annualized IRR: ~8% / year

- Earnings Reaction: (14.10%) on May 12, 2026

- Max Drawdown: 78.06% on 2/27/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Hims & Hers Health (HIMS) has had a brutal two weeks. The telehealth platform posted a GAAP net loss, missed earnings estimates by the sharpest margin in recent quarters, then immediately returned to capital markets for $350 million in new debt. The stock has shed roughly 30% since May 11 and sits 66% below its 52-week high of $70.43.

The surface narrative writes itself: messy pivot, dilutive financing, margin compression. But the Q1 earnings transcript and TIKR data tell a more complicated story, and the market may be pricing in a worse outcome than the fundamentals support.

What Actually Happened in Q1

Q1 2026 revenue came in at $608.1 million, up 4% year over year but 1.4% below the $616.8 million consensus. The GAAP EPS miss was starker: ($0.40) against an estimate of $0.03, driven almost entirely by a deliberate restructuring charge.

In March, Hims stopped advertising compounded GLP-1 medications and pivoted to branded products including Novo Nordisk’s Wegovy pill and pen. That shift triggered approximately $33 million in restructuring charges: $28 million hit gross margins, compressing them to 65% on a GAAP basis (70% adjusted), and $5 million hit operating expenses.

CFO Yemi Okupe said on the call: “We made a deliberate strategic pivot within our weight loss specialty, one that we knew would create near-term financial noise to unlock immense potential for the platform to accelerate at scale.”

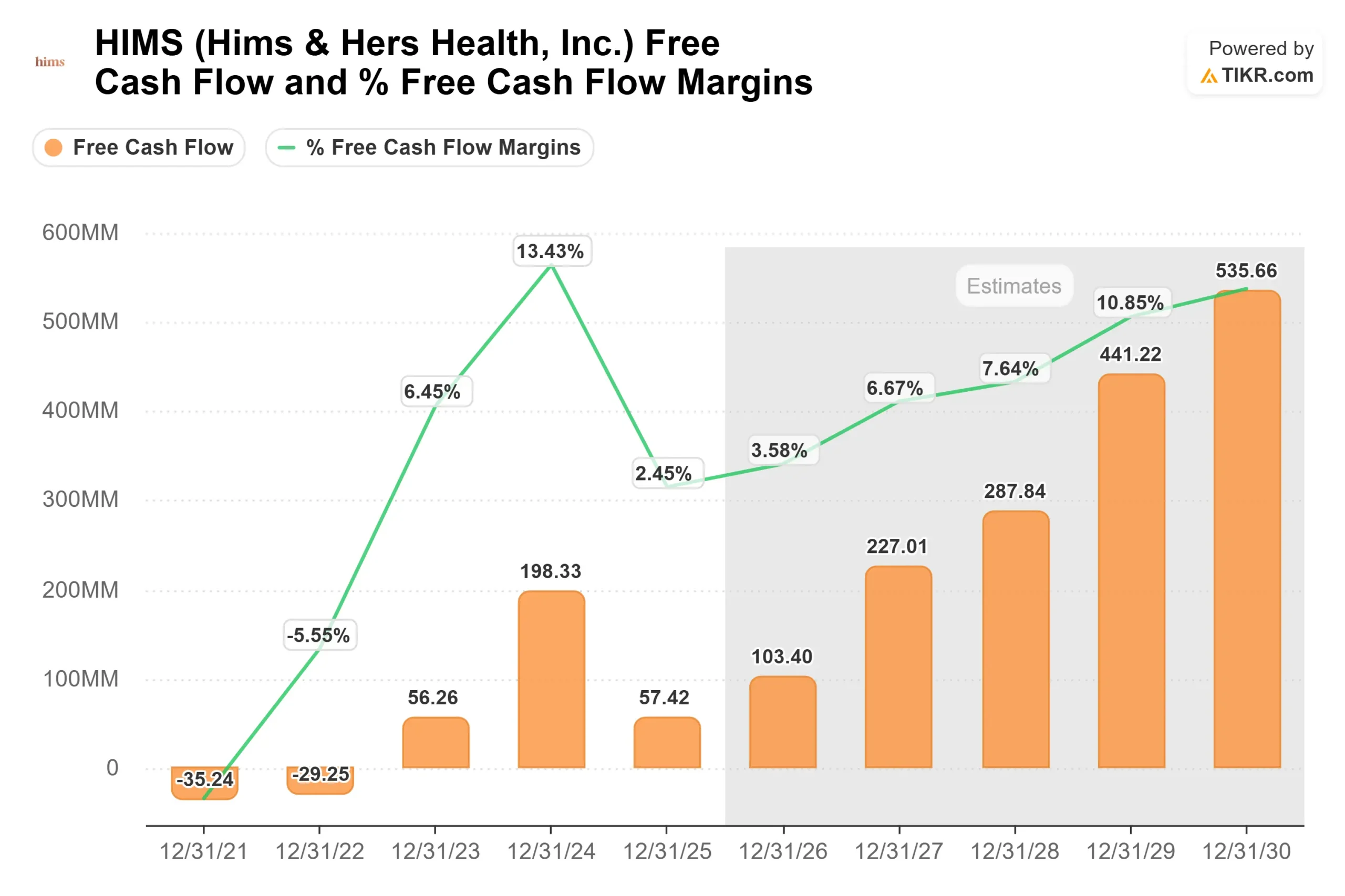

Below the GAAP loss, the cash picture was healthier. The company generated $89 million in operating cash flow and $53 million in free cash flow in Q1 despite the charges. Subscribers grew 9% year over year to nearly 2.6 million. Within six weeks of launching branded Wegovy access, Hims fulfilled more than 125,000 shipments, with new weight-loss subscribers running above 100,000 per month, per CEO Andrew Dudum. Nearly 90% of those new subscribers downloaded the app and interacted with a provider three times in their first month. The company raised its full-year 2026 revenue guidance to $2.8 billion to $3.0 billion, representing 19% to 28% growth year over year.

See historical and forward estimates for Hims & Hers stock (It’s free!) >>>

The $350M Debt Raise: What It’s Actually For

One week after the earnings selloff, HIMS returned to the capital markets. On May 18, the company priced $350 million in zero-coupon convertible senior notes due 2032, later upsized to approximately $402.5 million after the overallotment option was exercised in full. The conversion price was approximately $29.53 per share, a 32.5% premium to the day’s closing price, with capped calls layered on at approximately $50.15 per share to limit dilution. The stock fell another 8% to 10% on the announcement.

Zero-coupon structure means no cash interest until maturity in 2032, preserving near-term operating cash flow. The primary stated use is funding the Eucalyptus acquisition, announced in February, at up to $1.15 billion total. The deal adds Australia and Japan as new markets and deepens HIMS presence in the UK, Germany, and Canada. The structure requires approximately $240 million in upfront cash at closing, with $710 million in guaranteed deferred payments over 18 months and up to $200 million in earnouts through early 2029, settleable in cash or stock at Hims & Hers’ election.

With $751 million in cash on hand at Q1 end plus the fresh convertible proceeds, the company can fund the upfront Eucalyptus payment without drawing down domestic operating cash flow.

Whether the acquisition earns its cost depends on whether Eucalyptus accelerates the international platform thesis or proves an integration challenge.

The Platform Thesis That The Market Is Discounting

The most overlooked part of the Q1 call was the AI infrastructure update from CTO Mohamed ElShenawy, joining the call for the first time and now appearing quarterly.

Hims operates a closed-loop provider network where intake, diagnosis, treatment, and outcomes all live in a single stack. Every provider interaction generates clinically verified training data for its AI models, which ElShenawy called “the highest quality label in AI any company can hope for, and it can’t be acquired.” The AI team has grown to nearly 40 people, including applied scientists and PhDs from MIT and Berkeley.

Three AI products are live or near launch: a care coach copilot that drafts responses for human review, a Labs AI agent that explains biomarker results in full patient context, and an AI weight-loss companion launching soon. Each deepens the closed data loop HIMS has built over nine years. The Eucalyptus acquisition extends this flywheel internationally, into markets where branded pharmaceutical partnerships are already more mature than in the U.S.

The testosterone specialty shows how the model compounds over time. Customers track hormone levels via at-home blood tests through the YourBio acquisition, adjust treatment based on results, and stay engaged with a platform that learns from every interaction. Management reported internally that 95% of Hims testosterone subscribers saw an increase in testosterone levels within two months.

The Risks Are Real

Margin compression is structural in the near term. Weight loss, labs, and international carry lower gross margins than HIMS’s legacy specialties. Management’s 2030 target of at least $6.5 billion in revenue and $1.3 billion in adjusted EBITDA implies a margin of around 20%, a significant expansion from the 7% adjusted EBITDA margin posted in Q1. That leverage has not yet appeared in the numbers.

The convertible notes add a 2032 refinancing event at a point in the growth trajectory that isn’t fully de-risked. And TIKR data shows ROIC at 1.0% and return on equity at (2.7%), reflecting heavy reinvestment with no current return on deployed capital. Investors at current prices are underwriting future execution, not current results.

See how Hims & Hers performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $24.01

- Target Price (Mid): ~$35

- Potential Total Return: ~45%

- Annualized IRR: ~8% / year

See analysts’ growth forecasts and price targets for Hims & Hers stock (It’s free!) >>>

Using the mid case, TIKR’s model targets approximately $35 per share by December 31, 2030, a ~45% total return at around 8% annualized. The two revenue growth drivers are branded GLP-1 platform scaling through the Wegovy and Zepbound partnerships and international expansion through Eucalyptus and the existing ZAVA and Livewell operations, both compounding off $2.35 billion in 2025 revenue at a CAGR of around 10%. The margin driver is G&A and technology operating leverage as the platform scales, with net income margins expanding toward around 8%. The primary risk is regulatory: any material change in the FDA’s stance on branded telehealth distribution of GLP-1 medications would directly undercut subscriber growth and the Novo Nordisk partnership economics.

The Street is more cautious near-term. The mean analyst target across 14 price estimates sits at approximately $26, per TIKR data. JPMorgan maintained its Overweight rating but cut its target to $33 from $35 post-earnings, per reporting by The Fly via Stocktwits. Citi raised its target to $28 from $24 while keeping a Neutral rating. Neither is calling it a crisis. Both are waiting on execution.

Conclusion

The clearest near-term test is the Q2 2026 revenue print, expected in early August. Management guided $680 million to $700 million for Q2, representing 25% to 28% year-over-year growth a material reacceleration from Q1’s 4%. The mechanics are specific: monthly Wegovy subscriber cohorts stacking through Q2 should drive step-ups in both revenue and adjusted EBITDA in the back half of the year. If Q2 lands at or above $700 million with adjusted EBITDA toward the upper end of the $35 million to $55 million guidance range, the transition thesis earns its first real validation.

If revenue misses $680 million or EBITDA stalls, the full-year guidance of $2.8 billion to $3.0 billion comes under immediate pressure, and the convertible debt looks less like a strategic bet and more like leverage taken on at the wrong moment.

Watch for the Q2 print in early August. The number that matters is $700 million.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Hims & Hers?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Hims & Hers, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Hims & Hers alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Hims & Hers on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!